By Gary Tanashian

As the world awaits the Greek election, there was news today right here in Wonderland:

Treasurys rise after record-setting auction

Our great nation is selling more bonds (AKA debt) this week to keep itself afloat. Guess what? Demand was strong for 10 year notes.

Next up, 30 year debt will be peddled on Thursday. With the Fed on the bid, either in action or in implied waiting, one might expect that to be another bumper day.

"On Tuesday, the government garnered weak demand at its sale of 3-year notes. That could have been due to expectations for more Twist from the Fed, which may entail selling that maturity. That logic would also have lent support for the 10-year auction, and presumably the long bond sale in the coming session."

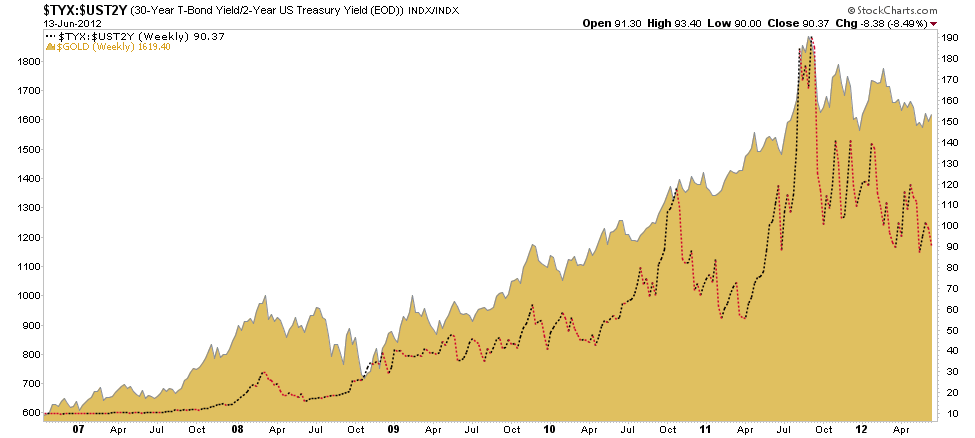

The indisputable message of this chart is that gold generally goes in alignment with the 30 year/2 year yield spread.

What a world; all a great and powerful man with a big brain has to do is cannibalize the unproductive legacy debt of the nation, eating what suits him (long term bonds) and serving what doesn't to others (short term bonds) in hopes that they eat the stuff. They are hopped up on deflation fear after all. They'll eat anything that is 'risk off' after all.

Point is, we have been following the correlation between gold and the 30-2 spread for many weeks now in NFTRH. The gold correction out of the hysterical phase of the euro crisis was very normal and indeed, expected. But the normal correction was then aided and abetted by the Fed's stated intention of Twisting (AKA 'sanitizing') its monetization of Treasury debt.

Really, how long can they keep it up? The fact is that whether they Twist again or go for the good old fashioned straight on monetization, we are off the charts and officials are just rearranging deck chairs on the Titanic as far as inflation is concerned. They have been, are and will likely continue to ram inflation into the pipeline through whatever means suits the agenda in the best way.

It will be interesting to see if gold obediently maintains the correlation. When the Twist manipulation scheme was originally cooked up and served in September, all the over bought metal needed was a shove in a southerly direction to get it to go with the program. Now, after what would qualify as a healthy intermediate correction, doing the Twist may not work as well.

Several points of analysis point toward this being a pivotal and very interesting summer; and not in a bearish way either. Real inflators may yet stand up and be counted instead of hiding behind intricate schemes and half measures. Watch the gold sector for clues coming out of what could be a volatile June. Subscribe to our free – and spam free – eLetter for a rational view of macro markets.

By Gary Tanashian

The headline read, "Treasurys rise after record-setting auction"

A slightly more accurate headline would have read, "Federal Reserve bought a record-setting amount of Treasurys". Why is the Fed buying Treasurys? Foreign purchases dried up some time ago because investing at essentially 0% interest in a business that is running annual deficits of $1.5 trillion is not considered a good investment.

Sellers of interest rate swaps create demand for Treasurys in order to sell Treasurys they don't have (fraud) which also acts to prop up the US dollar and maintain historically low interest rates. This is a ponzi scheme, but since it is backed by the Fed, which has the ability to create unlimited amounts of $$, it will continue indefinitelty . . . . or until the dollar is rejected as the global reserve currency, which will happen when OPEC starts taking something besides dollars for oil.

As I understand it, an interest rate swap is a derivative contract in which the seller of the swap agrees to pay a variable rate and the buyer agrees to pay a fixed rate on a securities portfolio that is entirely fictitious--i.e., that does not exist. If that is so, then the only way an interest rate swap could impact securities prices, hence interest rates, would be if the sellers of the swaps did not hedge their positions. In that case, because some of the buyers, if the swaps had not been available, would have shorted the government bond instead, the effect of their buying the swap would be to take some selling pressure off of the market. But if the seller of the swap prudently hedges his risk by taking an appropriate-sized short position himself, then the whole affair is a wash. No net pressure on government bond prices occurs one way or the other.

Take an example: suppose you agree to pay me a fixed rate of 4% per year on a fictive 30-year bond position with a starting value of $100,000. Since 4% of $100,000 is $4,000, that means you pay me $4,000 per year. I, in return, agree to pay you the average government bond rate, which is a variable rate. If the government bond rate starts out at 3% and stays there all year, that means I pay you $3,000. Since you are paying me $4,000, that means I make a profit of $1,000 per year. And if, say, government bond prices fall precipitously, and the government bond rate averages 5%, then you pay me $4,000, I pay you $5,000, and you make a net profit of $1,000 per year.

In short, you make money if government bond prices go down, and I make money if they stay roughly the same or go up. And if I, as the seller, short government bonds in a quantity sufficient to cover my risk if they go down, the existence of the interest rate swap is market neutral: it has no effect on the price of government bonds one way or the other.

In other words, if IR swaps did not exist, some of those who would have bought them would sell government bonds short instead; and if they do exist, the sellers of the swaps will short government bonds to hedge their positions.

Bottom line: IR swaps are market neutral unless the sellers of the swaps are unhedged--which means: they are market neutral unless the sellers of the swaps are insane.

Could insanity be the prevailing condition? Well, yes. If the seller perceives himself as "too big to fail"--meaning he expects to be bailed out at taxpayer expense if he screws up, then I suppose that he might book a lot of IR swaps without hedging his position. In a free market economy with functioning prohibitions against fiduciary irresponsibility and fraud, however, the existence of IR swaps would not pose a problem, and would not be a means by which the long-bond rate could be manipulated.

If there is a problem associated with the use of IR swaps, in short, it does not stem from the existence of the swaps, but rather from the sellers' expectations that they will be bailed out if their interest-rate bets go against them.

Also, the Fed held 62 of US bonds in 2011. Who knows what percentage they hold now? Yes, demand is strong bu for all the wong reasons. If the Fed stopped buying who would?

Demand for U.S. bonds is strong? Are you for real ?

Ever hear of Interest rate swaps ?

How long, And how much does it take of this insanity by the Government and Financial controllers. ( NO NAMES ) does it take before EVERYONE wakes up and starts to take charge of there own destiny. Is it not obvious that the monetary system is the biggest scam in human history and is in need now, More than any other time since the start of the Banking and The Federal Reserve system in 1913 to be scrapped. I would suggest that whatever the replacement, Has to be fairer and more suitable to decent hard working people than what has been forced upon us up to now. We need a CHANGE and we need it soon. It's WAKE UP TIME. Barrie Owen.