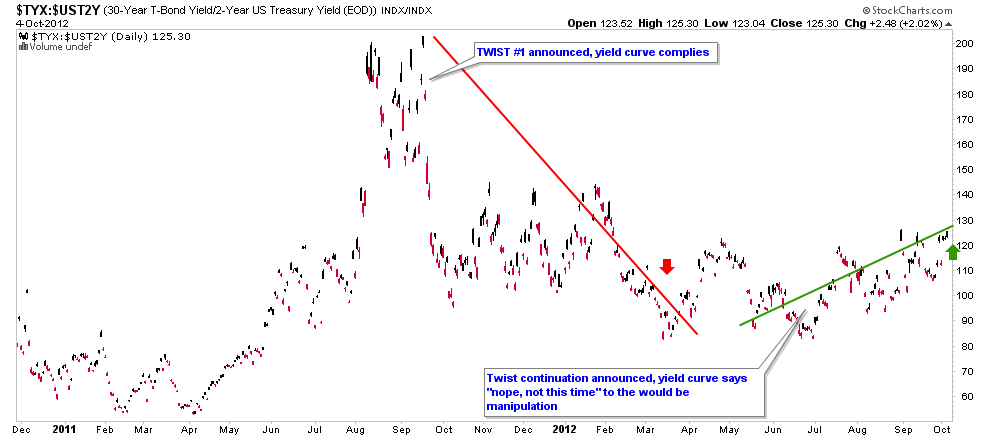

Using the spread between 30 year and 2 year US Treasury yields, we can gauge when policy makers are in control of market participants’ perceptions and when they are losing control to the free market’s will.

Operation Twist was announced in September of 2011 in the aftermath of the first phase of the Euro crisis as the yield curve had exploded higher, taking the monetary stress barometer, gold, with it. Over bought on unbridled momentum, gold entered an extended correction in line with the yield curve, which complied with policy makers’ goal of calming down the system. As shown many times in the past, gold and the 30-2 yield curve generally travel together.

By the time Op Twist’s extension was announced in June, an already mature gold correction and an in-line yield curve unsurprisingly did not respond to the manipulators’ directive. The operation whereby the Federal Reserve would buy up long-term bonds and sanitize the process by selling off short-term ones was exposed as the macro parlor trick that it is. It resulted in little more than a deflationary pretense against which inflationary policy could be promoted anew.

In hindsight, the free market knew that a bald faced and more honest inflation regimen would be engaged by policy makers desperate to keep power, as the yield curve shook off the Twist manipulation and looked ahead to full-on inflation or ‘i2k12′ (Inflationary 2012) as NFTRH coined it early in the year.

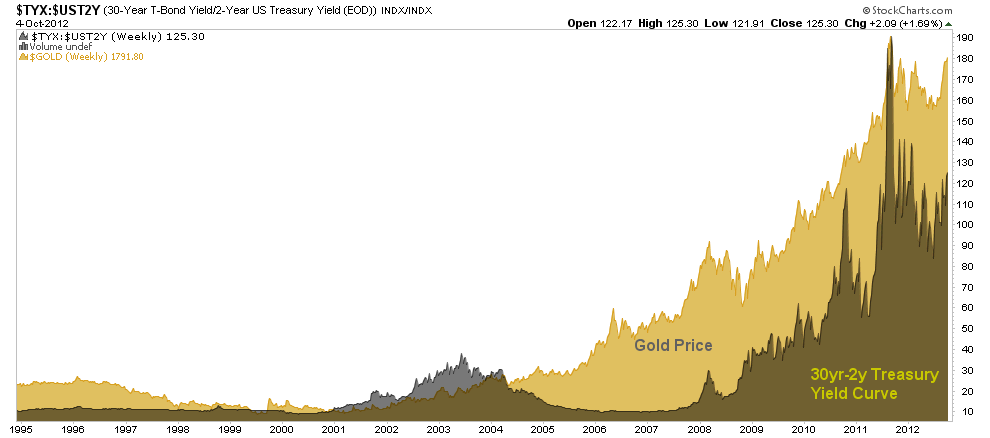

A rising yield curve is all about the promotion of inflation. The weekly view of the 30/2 yield curve and gold shows the Greenspan era inflationary regime, which was promoted against the bear market early last decade. This was the kickoff to what NFTRH terms the age of ‘Inflation onDemand’.

Greenie’s version of ZIRP resulted in a credit bubble and mal-investment far and wide. When he tried to take it back by raising short-term interest rates, the yield curve complied but a system already too far out on the leveraged limb eventually began to fall apart. The system was beyond normal austere policy making. To put it in non-technical terms, FrankenMarket needed juice and it needed it fast.

Enter the man for the job, Greenspan lackie Ben Bernanke, the new Federal Reserve chief, fresh with monetary and economic management ideas straight out of academia. Enter a whole new level of management where an epic macro game of ‘all or nothing’ came into play.

As US financial institutions began to fail, the curve began to rise as the Fed cut rates as fast as it could. Inflation was again being promoted, but the act of inflating did not stop the oncoming liquidation of Q4, 2008. The curve declined from the 2008 stress spike as it usually does during deflationary liquidations. These periods of deflationary pressure serve to build up the next stress spike in the curve.

As QE1 eventually took hold, the curve rose into the events surrounding the 2010 ‘Flash Crash’, at which point QE2 was promoted. This launched an intense phase of inflationary cost pressures that culminated in the curve topping out in late 2010, with commodities following suit in early 2011. This resulted in the deflationary pressures that held sway for the balance of 2011 before eventually giving way to a new inflationary regime that was born in the summer of 2012. Enter NFTRH’s long-awaited i2k12.

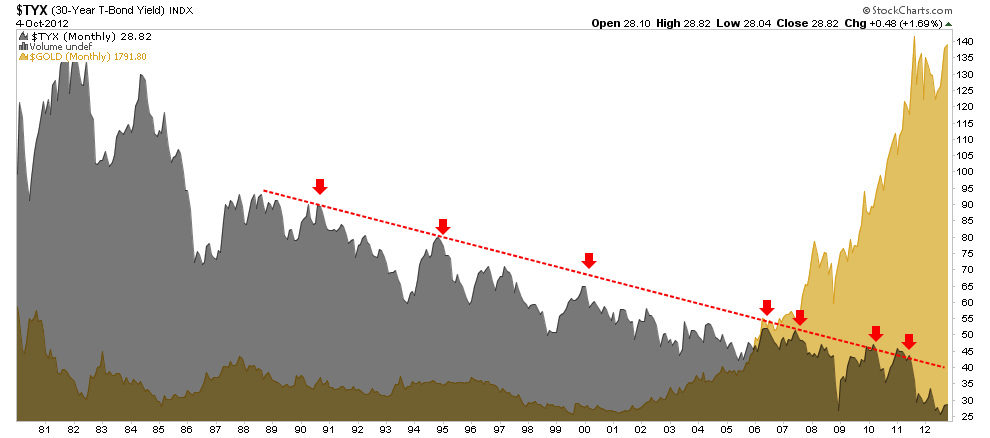

But the nominal 30 year bond yield has been declining since… forever; deflation is the play!

No sir, a wellspring of goodwill was passed on to Alan Greenspan by Paul Volcker in the mid-80′s and Sir Alan borrowed against this goodwill for all it was worth until finally, the system could not take it anymore. The great bull market of 1980 to 2000 expired and the age of Inflation onDemand began. The monetary metal was rightly contained until the current era where inflationary policy is used ever more desperately to battle the next oncoming liquidation.

There are no bond vigilantes anymore. There is just a massive market in US Treasury bonds being worked over by really smart people employing really dangerous operations. The middle chart above shows a curve that is ready to continue upward into building inflationary stress. The last chart shows that gold has not been deterred despite what is made to appear to be an ongoing deflationary continuum.

The current inflation could run until the curve reaches new highs and/or the Continuum paints another red arrow at the downtrend line. Or it could just run until the system ends; it’s a which ever comes first type of scenario. That’s our system folks; very high risk and high reward. But it is terminal. Hence the case for gold. The barbarous relic would help people bridge the gap between the dying system and the one that comes next. That is why it is not taking the bait anymore on the periodic liquidations.

Be safe first… speculate second. Safety means eliminate debt and own things of value. I fully believe that happiness can be achieved in these painful times. But you have got to take control and not take the mainstream media bromides to heart. I am not sure where this post came from or even where it went to. But there it is anyway. A great weekend to you.

**@bi****.com

Impressive article. Congrats on uncovering the ins and outs of the Feds. Maybe once bankers/hedge fund managers decided to play texas hold em with other people s money the fed had no choice but do do the same and go all in to face them

Time will tell as you say. I am not sure gold will be enough to bridge the gap of a new system...