Since we were the only ones (so far as I could see) even talking about the Semiconductor equipment industry ramp up (and positive implications on US manufacturing) back in early 2013 I think we should continue to tend the sector and finish what we started.

Last month the SOX took a massive dive down to our noted long-term support area in a giant swoosh of hype (coming from the financial media by way of one company’s outlook) and emotion by way of stampeding herds trying to get out at all costs. It was just a setup as the SOX resides at new recovery highs this weekend.

From my days in manufacturing (most of which were spent not directly participating in this sector) I remember the Semiconductor Book-to-Bill ratio (B2B) as a pretty heavily watched indicator among industry types. From Semi.org:

“The SEMI Book-to-Bill Report provides a first look at the book-to-bill ratio for North American Headquartered Semiconductor Equipment Manufacturers. The three-month average global bookings and billings are a strong indicator for trends in the worldwide semiconductor industry. SEMI follows the protocol established by the U.S. Department of Commerce in publishing our figures only on a three-month average basis. We do this in order to smooth out the natural volatility in bookings. This report is distributed monthly approximately three weeks after the close of each month. Categories covered include front-end (wafer processing/mask/reticle/wafer manufacturing/fab facilities) equipment and final manufacturing (assembly/packaging/test) equipment.”

On November 20 Semi.org published its most recent B2B data. First their summary and then a table covering the May through October 2014 period.

“SAN JOSE, Calif. — November 20, 2014 — North America-based manufacturers of semiconductor equipment posted $1.10 billion in orders worldwide in October 2014 (three-month average basis) and a book-to-bill ratio of 0.93, according to the October EMDS Book-to-Bill Report published today by SEMI. A book-to-bill of 0.93 means that $93 worth of orders were received for every $100 of product billed for the month.

The three-month average of worldwide bookings in October 2014 was $1.10 billion. The bookings figure is 7.0 percent lower than the final September 2014 level of $1.19 billion, and is 1.9 percent lower than the October 2013 order level of $1.12 billion.

The three-month average of worldwide billings in October 2014 was $1.18 billion. The billings figure is 5.8 percent lower than the final September 2014 level of $1.26 billion, and is 10.6 percent higher than the October 2013 billings level of $1.07 billion.

“While the global semiconductor equipment industry will see strong double-digit growth this year and is slated for further growth in 2015, order activity posted by North American suppliers has moderated, resulting in a book-to-bill ratio below parity for two consecutive months,” said SEMI president and CEO Denny McGuirk.

The SEMI book-to-bill is a ratio of three-month moving averages of worldwide bookings and billings for North American-based semiconductor equipment manufacturers. Billings and bookings figures are in millions of U.S. dollars.”

I created a graph of the data going back to 2010. If this were a stock chart we’d say ‘oops, looks like it’s losing support’. It is not a stock chart but it does bear watching. The green circle is the moment we noted the equipment ramp up based on input from my contact in the field. Manufacturing, the economy and ‘jobs’ were then extrapolated.

Bottom Line

Not to cause a big stir over 4 months deceleration, but it is worth keeping an eye on because in early 2013 it was worth keeping an eye on for its positive implications on manufacturing and eventually, ‘jobs’ and the economy. The Semi Equipment sector is now booking less than it is billing, and this could be a warning.

Our thesis is that a chronically strong US dollar (resulting from structural issues going on in other economies around the world) would eventually start to wear away at US manufacturing and exports. The Semi Equipment sector was the canary in the coal mine for positive events in early 2013 and its book-to-bill ratio can be watched going forward as an early indicator on an economy that the majority has confidence in these days.

Speaking of the economy, NFTRH 318 then went with a few thoughts on the global economy before discussing US and global stock markets in depth. Here is part of that economy discussion, complete with obligatory Wack-a-Mole reference…

Global Economy; Whack-a-Mole

Last week saw a cute little rodent called ‘Draghi’ pop up in the ongoing game of economic Whack-a-Mole as different countries and economic zones compete to avoid rapid deceleration, recession and/or deflation. In fact it was 2 Moles in one day as China dropped interest rates against slowing growth and a real estate market that is becoming an issue over there. These moles of course followed the BoJ a couple weeks previous.

Draghi Speaks the Truth http://biiwii.com/wordpress/2014/11/21/draghi-speaks-truth/

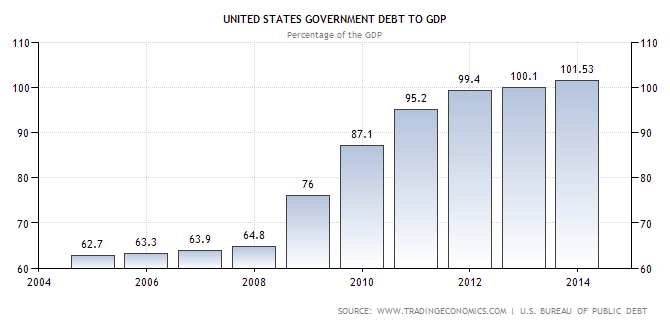

Let’s remember that it is the US that stands head and shoulders above most other economies in its economic profile. Of course, let’s also not forget that this recovery was created out of inflation and debt. Serious economists (Economy.com’s Mark Zandi, for one) continue to tout a self-sustaining economy. NFTRH will do the same… when evidence of self-sustainability comes about.

This data courtesy of TradingEconomics.com shows that debt has outpaced growth every step of the way in the now supposedly self-sustaining post-2008 economy.

Subscribe to NFTRH Premium for your 25-35 page weekly report, interim updates (including Key ETF charts) and NFTRH+ chart and trade ideas or the free eLetter for an introduction to our work. Or simply keep up to date with plenty of public content at NFTRH.com and Biiwii.com.