After fending off one blow from the SNB and another, albeit positive, surprise from the ECB, investors’ focus will, naturally, shift to next week when the Federal Reserve’s rate decision will take place. “What will Yellen say this time?” markets want to know. Can the Fed Chairman really stay hawkish while the rest of the world is plunging into a new cycle of easing? These questions have loomed over Fed meetings for a while now, especially as Oil prices plummeted and inflation expectations lowered. Yet to the surprise of many Fed watchers and investors, Janet Yellen, “the dove,” continued to press forward with a hawkish tone, giving an upbeat assessment on growth and stressing the Fed’s conviction that disinflation (low

inflation) is transitory. As the next meeting approaches, investors are now almost certain that the Fed will keep its hawkish tone in a rhetorical buildup towards an actual rate hike between June and December. But sometimes, when the consensus is optimistic, it is worth the time to pause and reflect on another possibility; could the Fed change its proverbial mind?

Is Disinflation Really Transitory?

One of the main anchors of the Fed’s belief that, indeed, the drop in inflation below 1% was and is transitory, is the US consumer. The rooted belief, as was expressed by the Fed Vice Chair Stanley Fisher, is that as growth continues to accelerate and unemployment to fall, the US consumer will feel more confident and will begin spending more, thus lifting inflation back to normal levels, even as global commodity prices are in meltdown mode.

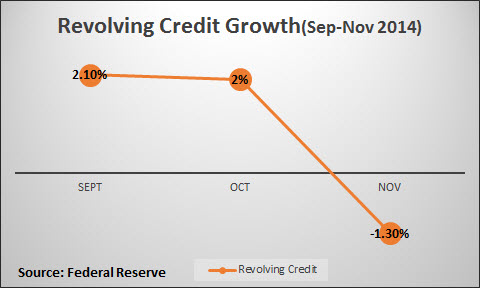

With US Consumer confidence hitting 98.2 and growth for Q3 reaching 5% at an annualized pace, and given robust retail sales, this notion of a transitory fall in inflation seems a reasonable supposition. And as long as consumers are spending more this makes perfect sense; more spending, less excess capacity in the economy, higher prices. Yet, with data on credit to consumers now having been released, any slowdown in retail sales may put a big question mark on that scenario. Recent data from the Fed shows that revolving credit, i.e. not mortgage debt but rather “quick credit” such as credit cards, took a sudden and unexpected plunge in November, falling by -1.3%. That data is not exactly in line with a confident, ready-to-spend consumer. Instead, and in utter contrast, a slowdown in consumer credit which comes with a sudden fall in retail sales and a plunge in commodity prices may point to a classic behavior in a disinflationary environment, an environment wherein consumers are postponing purchases because they believe prices will be lower in the future, thus starting another, often recurring, cycle of a fall in inflation. And if this is the case, then disinflation might not be that transitory after all, putting a big question mark on the Fed’s core scenario and an even bigger question mark on what investors believe around the world; that is, is a Fed rate hike coming soon?

Moving to Dovish in March?

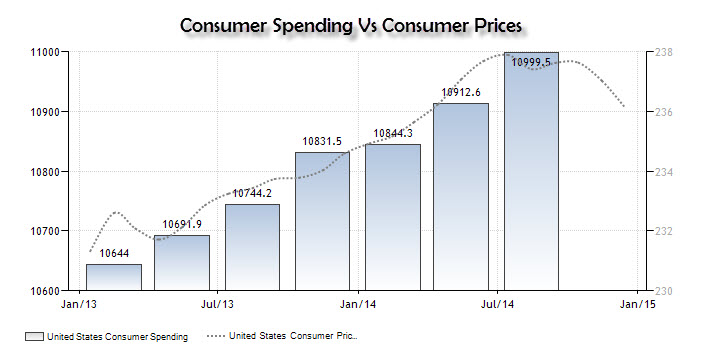

With data still robust overall, there is no reason for the Fed to change its hawkish tone that quickly; after all, this might very well be a short term bump in a long term trend upwards as the consensus expects and as hawkish members, and Yellen herself, believe. Yet, the next release of consumer spending data and credit due out next month could change that belief. As seen in the chart below, consumer spending rises in tandem with consumer prices. The Fed believes that consumer spending will continue to rise and thus will push inflation back up. But as one can see below, the final column for 2014 is missing in the consumer spending vs CPI chart, and if this column falls lower it could eventually prove that the Fed was wrong and that consumers, instead of spending more on the back of cheaper prices, are spending less as they would in a deflationary cycle and just as is happening around the world. Although the Fed tends to move gradually and therefore will not explicitly ditch its plans to raise rates, a clear warning on the risk of falling inflation would be enough to send investors a stark warning that rate hikes could be pushed back, further into the future, once again, much as Dollar bulls dreaded. So, before taking a US rate hike as a certainty, beware; a change from a hawkish Fed to a dovish Fed may be closer than it appears. Although data may eventually come in line with the Fed’s hawkishness, it might be a mistake to take a hawkish Fed for granted. Rather, it is wise to put a big question mark behind every hawkish statement until the data reaffirms that inflation is coming back again.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

When were they ever hawkish? The whole crux of the problem is they overdid asset inflation and even a normal bear market of 20-30 percent crushes the financial companies. It's all about propping up asset prices.

When are we going to pay attention to the jerry-rigging of the CPI under Clinton as he balanced the budget (by appointing Prof Jeremy Rifkin to give more weight to quality changes) thereby

lowering the impact inflation on soc security payments? If, for example, the average hard drive goes from a capacity of 10 gb to 1 terrabyte & if the new 1TB drives sell at 10 times the price as the older 1GB drives then the price of storing (say) 10gb fell 100-fold in the new Rifkin computation of the CPI.

really???? such dribble and speculation.

drivel?

what does dovish and what does hawkish mean?

Nothing, really. It used to be an old war term for those who wanted to wage war vs. those who wanted peace, but what that has to with economics or interest rates is anybody's guess.

Hi Bill ,

When Referring to monetary policy , the term dovish refers to the intention of a central bank to keep policy easy by cutting rates , adding stimulus or just leaving rates very. A hawkish central bank is when the central bank begins or is in the midst of raising rates and/or tightening policy amid a recovering economy. Hope this clarifies.

My guess is consumers are spending about the same, it's just going to different sectors than oil and in future groceries and utilities. Wages haven't risen, so not more money to spend there, but more discretionary money to spend after filling the gas tank. That won't produce a retail spending spike immediately, but should further along.

The Fed is unlikely to move beyond a "tiny" amount, never going back to traditional levels. This is an economy where we are focused on a "Greece" type work force (shifting from high skilled, high wage jobs to low paying jobs in restaurants and hotels) following the Greek example. We can't afford to raise interest rates. We can't afford to spend as the number of credit worthy people is tapped out today. There only so many categories of new sub-prime borrowers we can add.

Think of us like Japan. Remember 1999? Remember 2014? Over time debt and the related interest eats up consumerism. We do the rest to ourselves by not limiting immigration to people who add to the Federal tax base.

Agree on tiny, the old days of 4% being a neutral rate are long gone. I expect in '16, ceteris paribus. maybe four 25bp hikes over the year. More window dressing than substantive.

As for Japan, main difference is we aren't an export based economy.

As for spending, I think we'll see it pick up in auto, housing, and others while consumer debt will get paid down a little and maybe 401k's will be more fully funded. Some sectors get hurt, some get helped.