For many investors, this will feel too much like déjà vu by a half; the Greek woes are here yet again. And again, the Greek government is attempting to negotiate a new bailout deal with the Troika, even as European leaders debate whether or not to accede to that request. And, yet again, the question of a possible collapse of the European Currency Union emerges. However, unlike the last time, markets are reacting relatively calmly to the news of the breakdown of the current Greek bailout agreement. In part, that can be attributed to the lingering impact of the ECB’s Quantitative Easing program which was recently announced but it is also in part due to the broad belief that Greece would not likely exit the Eurozone. It seems investors’ two burning questions, i.e. will Greece leave the Eurozone and if it does, can the Eurozone survive, may be hard to disassemble. Nonetheless, it is a fact that, quite often, events in history can teach us as much about the past as about the future and it is those lessons which can help us disassemble those important questions.

Not the First Time for Greece

While the notion of Greece being the E.U.’s Achilles heel might sound like a story of only a few years past, the truth is it goes much farther back. This is the not the first time in relatively modern history that Greece has played a “spoiler” role, and since the Latin Monetary Union no longer exists, it’s not difficult to guess how the first saga ended. In 1865, the Latin Monetary Union became a framework of agreed currency exchanges set by its member states, e.g. Switzerland, Italy, France and Belgium; Greece and Spain joined a few years later. The monetary exchange system, which relied on the value of Gold, basically counted on each country to produce a coin at a specific gold weight that would be matched by all members, thus insuring a de facto single or one monetary currency.

Yet it wasn’t too long before it was revealed that Greece, with a highly indebted economy, was minting union coins with less Gold than it was obligated to. Back then, as now, Greece was a country that had constant economic and debt crises, a country with a low productivity rate. Eventually, after escalating tensions with other members, in the year 1908 Greece was forced out of the union. Through Greece was eventually permitted to return, nothing had changed from the point of Greece’s initial expulsion and it wasn’t long before other countries were over-spending, as well. Soon after that, most members were inflating their currencies as well as printing worthless bills to the point that, eventually, trust in the union went far beyond the point of no return; the union effectively stopped working when World War I broke out. In truth, while Greece could not take sole blame for the union’s collapse, it was Greece’s inflated currency that had been a major destabilizing factor.

Theoretical Lessons

In retrospect, the first and perhaps the more intuitive lesson might have been not to include Greece in the union in the first place, but of course it’s a bit too late for that discussion. But the second lesson to be learned is critical; that fiscal integration is a key pillar for every union, a key that preserves the trust in the system.

Lessons in Practice

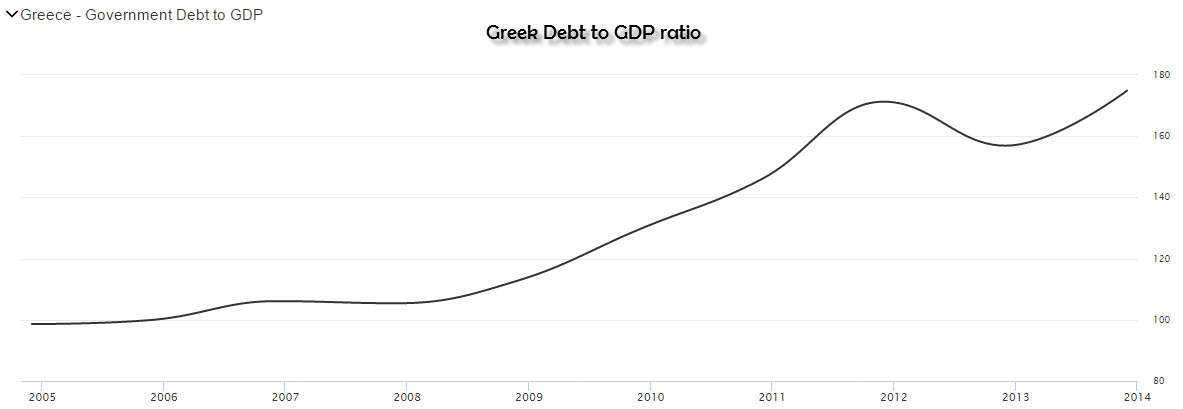

Cynics might say that theory is one thing while practice is another entirely. How can this history lesson guide us in gauging the path of the current tangled situation between Greece and the rest of the European Union, between the German finance minister Wolfgang Schäuble and the Greek finance minister Yanis Varoufakis? Unless Greek debt is viewed as the equal of German debt, unless Germany and other stronger members can guarantee that Greece will not leave debt holders with a haircut, Greece will always “cheat in minting its coin” and, as a result, Euros will be worth less and, eventually, the decoupling of Greek bonds and German bonds will leave no path except to a breakup. Given that, any haircut – in theory or in practice – will raise the risk of holding Greek debt vs German debt, which will only allow Greece to drift further away and endanger the European Union. Since the only chance for Greek bonds to near the yields of a Germany bond is through another bailout that may be the only option to fix the fractured trust. If Greek debt continues to grow, as seen in the path below, and if Greek bonds continue to trade as junk bonds (as surely will happen without a reliable bailout), the Euro as we now know it – perhaps not tomorrow or the day after or even within the next two years – will eventually end up just like the Latin Monetary Union, in the pages of history.

Chart courtesy of TradingEconomics.com.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

the Greeks will never change. they are a lazy welfare country that want their government jobs but avoid paying their taxes. they deny the fact the country can not continue to support a country on government wefare. Lets go to the beach.

Sounds like the rest of the world nowdays 🙂