The FOMC meeting ended yesterday as many had expected. Besides some marginal tweaks in the language, the message remained the same; data will determine our rate policy. Now, hours after the latest US GDP figures hit the newswires, it seems that Dollar Bulls are gearing up towards a September rate hike. Part of their rationale is because the data is good enough to sustain a rate hike. And that’s essentially true. With wages growing annually at 2%, Core Inflation at 1.7%, unemployment at 1.8% and now GDP bouncing back, indeed, a rate hike is warranted. At the same time, there are essentially no signs that the US economy is overheating. Rather, we’re seeing notable signs of stabilization. This, then, begs the question: How many rate hikes can the US handle in the upcoming year?

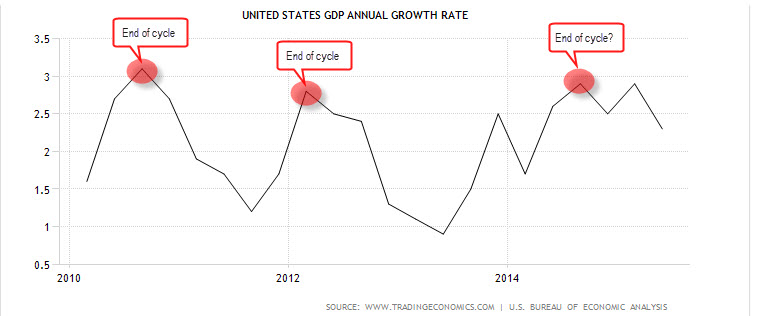

No Escape Velocity in GDP

When we examine the dynamics of GDP growth, it’s evident that the US GDP growth rate is not breaking the range. Instead, it has the same cycles that tend to end around the 3% growth rate. After that, the US economy tends to decelerate, only to regain momentum later. But this range of growth has not been broken. This means that there’s no evidence that US GDP is at escape velocity, a pace which would require several rate hikes a year.

Chart courtesy of Tradingeconomics.com

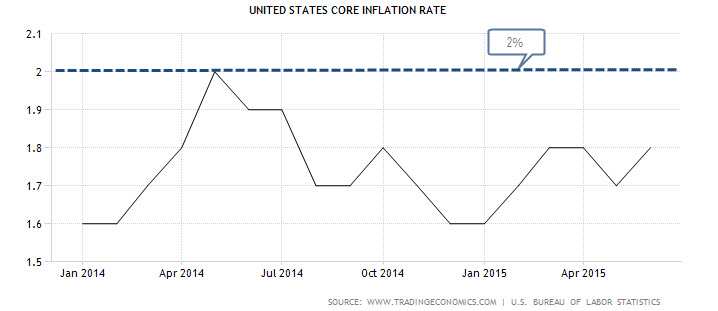

No Escape Velocity in Inflation

When we examine US Core Inflation, a similar picture emerges. US inflation is within the Fed’s 2% range and is showing no signs of overheating, i.e. escaping the Fed’s target. Rather, every time it reaches the 2% range, it tends to cool and then slide slightly lower.

Chart courtesy of Tradingeconomics.com

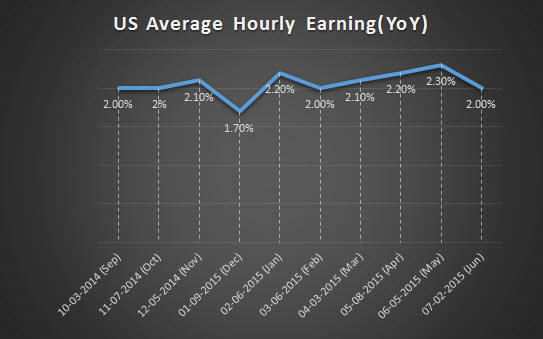

Growth in Wages

When we examine wage growth (YoY), wages are growing at around 2% annually, which is fine. But that is the kind of wage growth that produces a 2% inflation rate, more or less where we are now. There are no signs that wages are accelerating above 2%, and with a low participation rate, that

might take significantly more time.

Chart courtesy of FXStreet.com

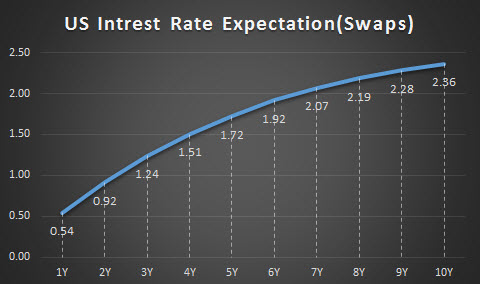

What this Means for Interest Rates

Don’t be mistaken; the numbers are pretty much okay. The US probably does need a rate hike and maybe another one next year. But growth doesn’t seem to be overheating, inflation is and continues to look steady at or below 2% with wages are moving in tandem. That means that everything is in check and there’s no need to slam on the brakes. In other words, there’s no need for the Fed to cool down the economy.

With that in mind, and still no other evidence, it’s hard to see more than a single rate hike this year and perhaps one other in 2016. With that said, that’s pretty far from some speculation, i.e. a 25 bp rate hike every other month in 2016. But as you can see from interest rate swaps below, the money market holds the former view. That is, no more than two rate hikes in the coming year. And that is simply because more than that is not needed.

Chart courtesy of Thomson Reuters

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

With inflation at 1.7%, it's clear that there is no need for a rate hike any time soon. Wages and employment growth is far from robust, and this recovery is tenuous at best. The lunatics in Washington continue to pour money only into a massively bloated war machine and let everything else, including the country's infrastructure "wither on the vine." There is no current economic justification for rate hikes, period, and unless inflation hits 4% or more, there is no need for one either.

We also need to find out the inflationary effect of the real estate price increase which could

lead to spiral effect of rent increase and then expected compensating wages increase required by businesses to keep up with its manpower sustainability. Examples include Macdonald n Walmart that

will have cross-over effect on wages in other industries.

Yellen is expected to have the foresight in dealing with the interest rate to avoid even a slightest chance of the overheated economy before it becomes uncontrollable. But the measures must be mild enough not to

rock the boat.

Real estate prices will go down if interest rates are increased. The interest rate decreases are one of the essential factors in the recovery of real estate prices over the past several years.

Accommodation will stay the rule, I expect the occasional 25bp slowly up to 1% or so but no return to the old neutral rate of 4%. Our current broken business model won't survive much of a hike, there is no stomach for killing the current irrational exuberance, and no interest in popping the current housing bubble. Mild strengthening of the dollar to keep commodity prices low but no more than needed to keep oil below $60 as the euro strengthens.

With total U.S. debt to GDP at around 360% , it's not wise to incsease rates until our economy has a chance to delevelage. (which could take a long time). With the long bond rate now just under 3%, over time my experts

at hoisingtonmgt.com indicate we may see the long rate decline to 1.6% - 1.8% from here. Before you laugh

outloud, check their long term record.

Since the banks that own the Fed (ditto for the other CB's) have been dining on virtually interest-free money for as long as the taxpayer is willing to allow the national debt to increase, they could easily have a number of piddly 1/4% increases and it wouldn't amount to a f*rt in a gale.