The coming weeks could be pivotal ones for the Euro. This time, it isn’t because of a threat to its existence or a member state’s bankruptcy. No, this time, it will be because of the actions of Mario Draghi and the European Central Bank. The ECB chief has the power to ignite the momentum desperately needed to awaken the Eurozone from its economic stupor. Simply put, Mario Draghi must push the Euro below 1 Dollar.

The Eurozone Lately

When we examine the latest trends in the Eurozone, we do see some positive signs. Exports have recovered, and industrial production has increased, as well. On the consumer front, retail sales have also been accelerating nicely. On top of that, the Eurozone’s GDP growth rate has been inching up, albeit at a very moderate pace.

Chart courtesy of tradingeconomics.com

Of course, this is largely attributed to the massive depreciation of the Euro. The common currency has fallen more than 20% against the dollar in less than a year. But, and this is a very big but, those tenuous improvements are not enough to underpin a Eurozone recovery.

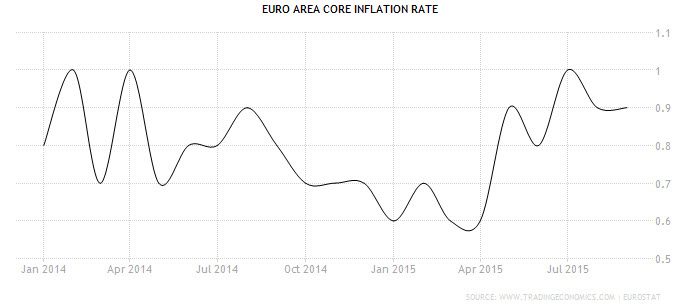

For example, the Eurozone’s Core Inflation is still remarkably low at an annual pace of 0.9%, half the pace of US inflation. Then factor in the latest woes from the Germany, where exports recently plunged. That suggests some mild weakness for the EU’s growth engine. Of course, the Volkswagen “controversy” and the nose dive in Deutsche Bank’s earnings aren’t helping either.

Chart courtesy of tradingeconomics.com

The Risk of Inaction

One of the Eurozone’s key weaknesses has always been with the ECB. With the institution’s conservative approach, quite often, the stimulus was too little, too late. Other times, the ECB ignored inherent weakness, and back in 2011, it hiked rates prematurely only to have to cut them later.

Simply put, ECB policy was, at best, merely unhelpful, but at its worst, it was harmful. The ECB can’t seem to get the Eurozone economy past stability and into recovery. Because whenever that last little push is needed, it’s nowhere to be found. What ECB policy is missing is the wherewithal for that last little push. That’s the one that will that get the economy over the hump.

Unlike his predecessor, Jean-Claude Trichet, Mario Draghi is willing to unleash Federal Reserve-like measures. However, Super Mario needs to prove that he is capable of putting some positive momentum into the Eurozone economy. And he needs to do that now.

Perhaps that’s the biggest difference between the conservative camp in monetary policy and the more progressive. That is the emphasis on momentum. It’s not enough to have the economy just move in the right direction. The momentum must be strong enough to keep it moving.

The ECB has been purchasing €60 Bln of Bonds monthly to stimulate the economy and weaken the Euro. The hope is that that would boost exports, which are the Eurozone’s main growth engine. Indeed, this has been working, and exports are starting to recover. But that recovery is still very moderate, and as Germany’s exports reveal, also very fragile.

That leads to the singular conclusion that what is missing is momentum. If the ECB is willing to give one final push, to get the Euro below parity with the US Dollar, that could do it. That could allow Eurozone exports to become really and truly competitive. Growth and inflation could actually approach ECB targets and not be illusively so.

Despite the paradox, Draghi needs to push the Euro off a cliff. In the absence of that, the fragile recovery will die out, and the Euro will be weaker. That weakness could endure for far longer than the ECB would like. Just look at what is happening to the Japanese Yen. The BOJ, trapped in its own conservative approach, failed to give that extra push of stimulus. As a result, growth and inflation were left for dead, and the Yen became a target for short sellers. The reality is that it’s time for Super Mario to live up to his name.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

do you have some info in french .

Hi Eric,

I'm sorry to say that we do not offer information in French.

Best,

Jeremy

(1) The present force of deflation is the strongest one globally and shows no sign of abatement, and (2) the USA could easily initiate a new type of QE, which would shoot down anything super Mario could do...after all, who wants to lose the currency war? and (3) I will continue to add real money (silver and gold) to my holdings while the prices are ridiculously cheap.

Time to buy Gold and Silver.

Major Currencies are becoming worth less-and-less.

Rising dollar contributes to fall in commodities. It's misguided or disingenuous to call for more aggressive action to reduce their exchange rate.

(Doing a comparison with yen)

The actions they take are of limited aid because (at least in this country) the middlemen are sucking up the differences between the currencies into higher profits and not passing them on to consumers. Despite the tear upwards in the US dollar, on e might go to a Honda or Toyota dealer only to find the prices rising significantly despite the strength in the dollar (many more examples). So frankly I think that if they drop the euro to half what it is now, we will see the standard price hikes next year which translates into no significant ROI for EU.

How can the euro have fallen 20% against the dollar and both the US and Europe reporting inflation of less than 1%. Did prices not change as a result?