At long last, the market finally got their long awaited Federal Reserve rate increase. Yesterday, the Fed hiked the Fed Funds rate by 25 basis points, from 0.25% to 0.5%. The Fed's famously watched "dot plot" revealed that most members expect at least four rate hikes in 2016. And investors? If interest rate swaps are any indication, then investors expect no more than two rate hikes next year.

So who is right then? The Fed? Or the market?

It's all about Oil Prices

The crux of the discrepancy between what the market expects and what the Fed expects is the inflation outlook. Even more specifically, it is the outlook for energy. The market is downbeat on energy prices for the foreseeable future. It views energy prices as a considerable hurdle to higher rates.

From Janet Yellen's speech yesterday, we can read between the lines. The Fed sees the negative impact of low energy prices as transitory, with no long-term risk to inflation. In other words, the Fed sees the pressure on Oil prices fading.

Who is Right?

We all know that, sometimes, the Fed can be overly dovish or overly hawkish and miss the mark. But then again, so do investors. Many times, investors tend to ignore, or at least underestimate, long-term risks to their scenario. Who is right this time? Of course, we'll only know with certainty at the end of 2016. But this writer believes that, this time around, the Fed is the better forecaster.

Here is Why:

First of all, we have to realize that Oil prices are at historical lows. It's true the market is oversupplied but how much longer can Oil producers keep producing. Right now, the pace of production is roughly ** barrels a day. When you consider that many producers are losing, we might not have too long to wait.

When that does eventually happen, Oil prices will be coming back from a very low base. Along the way, the risk of Oil prices spiking, which could send inflation higher, becomes a real possibility. Certainly, that risk is more tangible than the market believes.

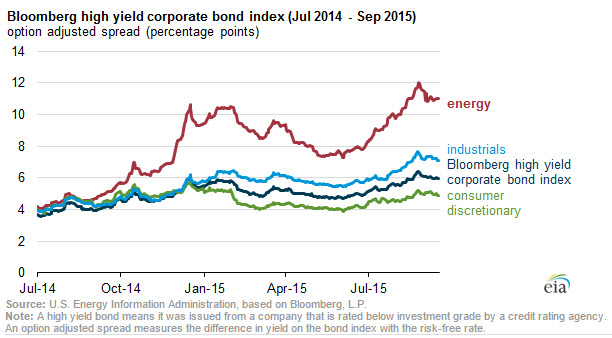

Just as an illustration of how much pressure is on Oil producers, take a look at the chart below. From the chart of EIA (based data from Bloomberg LP), we can see high yield bonds from various sectors. What emerges, when comparing the Oil sector to peers, is clearly a troubling image. The energy sector and its energy-associated yields are surging above 10%, far above unrelated peers.

Not only that, but according to the EIA data, debt payments now pose more than 80% of operational cash flow in US onshore Oil producers. Obviously, that leaves very little free cash flow.

Smaller producers, which are only partially responsible for the US Oil production surge, are barely treading water. Thus, it is, of course, only a matter of time before pressure becomes too much to handle. Then, smaller Oil producers will begin to default and trigger a mini domino effect. Once they do, the Oil supply could suddenly shrink and Oil prices suddenly spike.

Chart courtesy of The US Energy Information Adminisration

What does it mean for the Dollar?

Of course, this brings us right back to the US Dollar. The argument for higher Oil leaves us to conclude that inflation and interest rates might play out closer to the Fed's scenario. That's in contrast to investors' consensus which expects much more moderate Fed tightening. And this leads us to conclude, once again, that the consensus is overly dovish on the Dollar. And if that is, indeed, the case that leaves plenty of room for more Dollar gains to come.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Lior, first of all the real world inflation is more than what the fed declares it is. Using 1999 CPI calculations for example, it's running near 5%. Also know that the current formula assigns a less than 1% weighting towards total CPI for health care. That tells you right there how phony the "no inflation" slogan is. Anyone living in the real world knows it's more, and anyone on a fixed income is being fleeced. Secondly, if economies tank and go into recession, oil prices won't recover like you said. No one knows if that will happen. A "V" shaped recovery that was predicted last year did not happen, and won't for 2016 either if global economies are in the tank and demand is not there. Regards