Almost two months into 2016 and the stock market isn't sending investors much news to cheer about. The S&P 500 is down roughly 6% year-to-date and global economic concerns regarding a lack of growth and record low oil prices means that volatility is high and investors are skittish.

While high growth sectors like energy and industrials are suffering, defensive sectors finally have their moment to shine. But not all defensive sectors are performing as well as expected in the current environment. Consumer staples, generally a sector that does well when the broader averages are doing poorly, doesn't have much to offer investors. The Consumer Staples Select Sector SPDR ETF (PACF:XLP) is up marginally at only 1%. However, there's another defensive sector is enjoying the performance spotlight.

The Utilities Select Sector SPDR ETF (PACF:XLU) is up 8% year-to-date. A sector traditionally associated with defensive utility stocks and high dividends makes for an ideal bunker for investors seeking shelter from a slowing economic fallout from China and other factors.

While utilities are a rising tide lifting all ships in the industry, one company stands out as a strong performer, a high dividend payer, and consistently beats earnings.

A Stable Energy Provider That's Making Waves On Wall Street

DTE Energy Company (NYSE:DTE) is a $15 billion electric and gas utility company that operates on a national scale with its largest consumer base located in Michigan. The company recently beat earnings and received an analyst upgrade making it one of the few outperforming stocks in the market.

The company reported 4th quarter earnings of $1.01 per share versus the analysts consensus of $0.99 per share marking the second straight quarter of earnings beats. Since December, the stock has had two analyst upgrades to a "buy" or "overweight" recommendation while one initiated coverage with a "buy" recommendation as well.

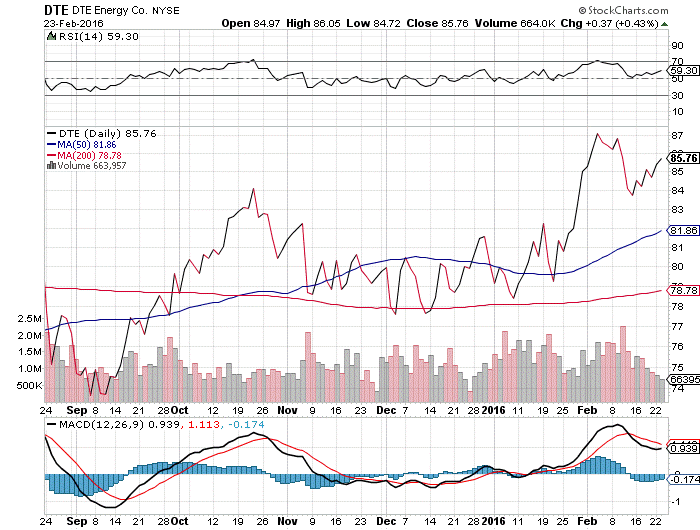

Looking at DTE's chart shows us considerable positive momentum building up in the stock.

Chart courtesy of StockCharts.com

The first thing to note is that the 50-day moving average is moving steadily away from the 200-day moving average – a strong momentum signal that's matched by its positive MACD. Despite the growth, the stock isn't overbought yet either with an RSI of 59.30.

The stock trades at 17.7 times earnings – slightly less than the industry average of 19.1 and well beneath the S&P 500 average of 24.3. It also has a relatively high EPS growth estimate for utility stocks of 5.5%. Like most utility stocks, DTE comes with a hefty dividend yield of 3.40% giving it additional downside protection aside from simply being in a defensive industry.

Despite the mild weather this winter, the company made up for any utility weakness through its non-utility segment which posted year-over-year growth of 14%. Commercial growth in its utility segment has helped bolster company earnings as well with continued growth expected throughout the year.

Full year earnings guidance for DTE ranges from $4.80 to $5.05 per share. Given its P/E and expected earnings, the stock is fairly valued at around $90 per share. That gives investors a 5% upside with just growth and more than 8% considering its dividend yield. In a bear market, its a high-flying stock with a stable business and low risk.

Check back to see my next post!

Best,

Daniel Cross

INO.com Contributor - Equities

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.