I recently wrote two articles highlighting Disney as an inexpensive growth opportunity for long-term investors. In my opinion, Disney presents a compelling case for long-term investors. My positive sentiment is rooted in many lucrative franchises such as Star Wars, Pixar, Marvel, ESPN and the legacy Disney brand turning out original content such as Frozen and more recently Zootopia. Disney offers a deep and well-diversified product portfolio that is set to provide growth, income and safety well into the future. This portfolio gives rise to a basket of entertainment income streams via movies, licensing deals, theme parks, TV programing, resorts and distribution rights. Disney stock has been under pressure as of late due to increasingly worrisome revenue declines from its ESPN franchise. I feel this decline in the stock is unwarranted, and analysts underestimate the ability of Disney to evolve to the consumer and monetize ESPN via other means. My views were recently echoed by analysts at Pivotal Research which upgraded the stock from a hold to a buy and raised its target price from $104 to $122. JPMorgan Chase also reiterated its buy rating and assigned a $118 target price. Disney has witnessed fantastic growth over the last decade and considering future catalysts in the pipeline; Disney appears undervalued. Disney currently sits at a P/E of ~18 along with a PEG of ~1.5 and has seen its stock fall from $122 to a current price of ~$98 or alternatively a 20% decline. Taking a look at its P/E ratio (currently 18 – in-line with the broader market average) indicates that it’s an average stock and I believe Disney is much more than the average stock. This presents a great buying opportunity in an inexpensive, high-quality growth stock.

Disney’s Q2 Fiscal 2016 Results

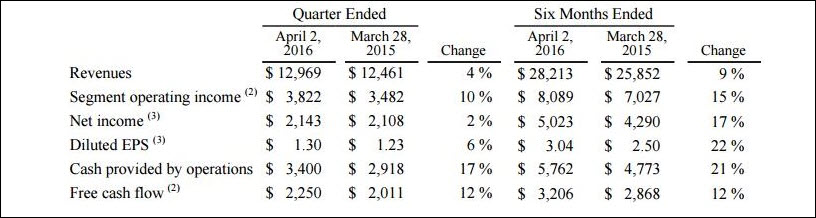

Disney released robust fiscal Q2 2016 results across the board albeit continued stagnation within its Media Segments division was reported. Overall, all major financial metrics (i.e. revenues, income and free cash flow) increased from the prior quarter and prior six month period (Figures 1 and 2). Comparing the two six-month comparable earnings periods, all metrics increased by double-digits with revenue coming in at a 9% increase.

Figure 1 – High-level earnings overview from fiscal Q2 2016

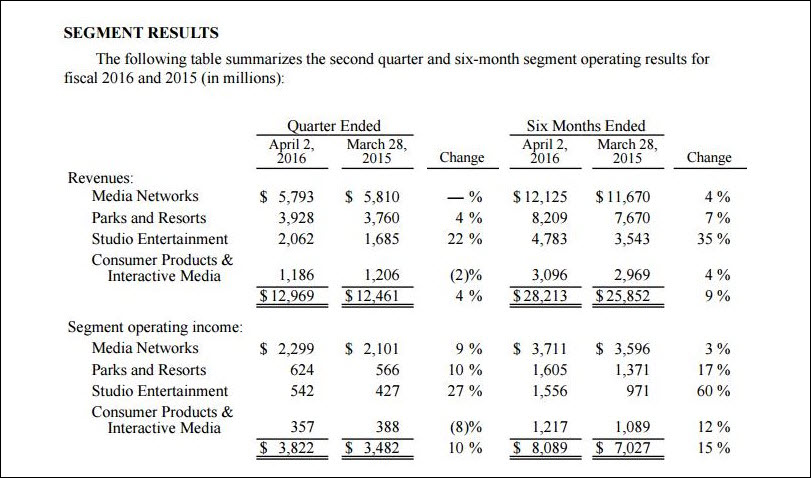

Figure 2 – Detailed segment results for fiscal Q2

Taking a closer look into the earnings report, continued weakness persists in the media networks segment as revenue was flat quarter over quarter albeit operating income increased. Disney is taking a $147 million charge to shutter its video game unit within the Consumer Products and Interactive Media division as revenue decrease 2% and 8% quarter over quarter and comparable six month periods, respectively. Disney appears to be taking proactive measures and divesting non-core assets that clearly aren’t performing well nor adding value to its overall business. Outside of the Consumer Products and Interactive Media division, the decrease in revenue from its Media Networks appears to have been arrested with a slight bump over the comparable six-month period.

“We’re very pleased with our overall results in Q2, which marks our 11th consecutive quarter of double-digit growth in adjusted EPS.” “Our Studio’s unprecedented winning streak at the box office underscores the incredible appeal of our branded content, which we continue to leverage across the entire company to drive significant value. Looking forward, we are thrilled with the Studio’s slate and tremendously excited about the June 16th grand opening of the spectacular Shanghai Disney Resort.”

- Robert A. Iger

Hasbro Results May Be A Long-Term Tailwind For Disney Earnings?

Disney and Hasbro have established a mutually beneficial partnership as Hasbro’s recent quarterly sales increased by 16%. This double-digit increase in sales was largely attributable to the sales of Disney’s Star Wars and Princess franchises. Overall, Hasbro’s revenue grew to $831.2 million from $713.5 million during a time that is typically slower for toy makers. Hasbro’s strong numbers benefited from the late 2015 release of the new Star Wars film. CEO Brian Goldner stated “Retail and consumer demand for Star Wars remained very high” and that Hasbro’s line of Disney Princess characters was “very positive.” The Disney and Hasbro relationship is being leveraged for future movies such as the recently released Captain America Civil War film. Goldner stated that Hasbro can facilitate excitement about Star Wars property as the film is released on home video later this year. These strong numbers may serve as a long-term tailwind for future Disney earnings. As strong consumer demand indicates albeit, via toy sales, this may bode well for licensing deals, home video sales, merchandise sales, and future spin-offs of these popular movies and franchises.

Future Growth and Pipeline

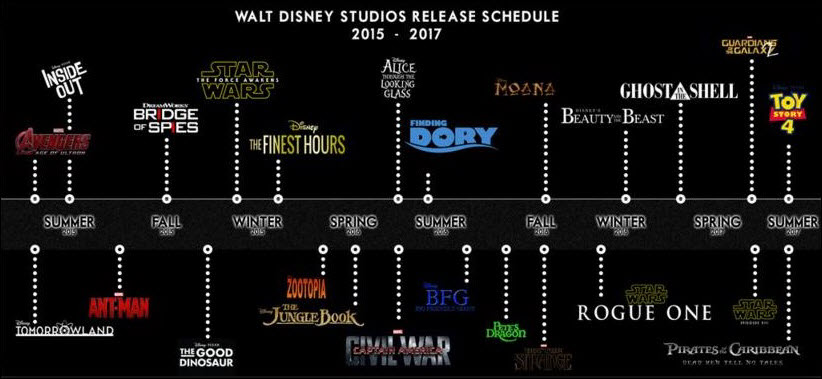

Disney has a rich pipeline with Star Wars themed parks, Star Wars movies, the opening of Disney Shanghai later this month, Marvel movies, Pixar movies and future Disney movies such as Finding Dory to highlight a few. The deep movie portfolio and distribution schedule is highlighted below (Figure 3).

Figure 3 – 2015-2017 Disney movie line-up

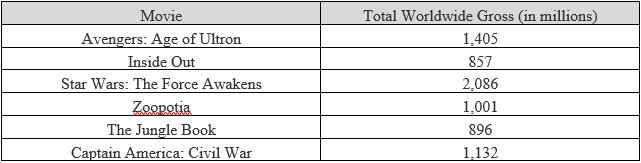

The strength of this movie line-up is easily in the billions of dollars just in theatrical release not to mention the licensing deals for product related sales and spinoffs for future releases. Taking a look at a few of the hits from this movie schedule highlights the Disney movie moat (Table 1).

Table 1 – Highlighting a handful of Disney blockbusters

The early success of this pipeline of movies is a strong indication of Disney’s movie moat; considering sequels are slated from very successful originals can only bode well for Disney. Table 1 highlights six movies that grossed beyond or near the billion dollar mark over the most recent nine month period. Finding Dory is an upcoming attraction that will likely add significant revenue streams for Disney throughout the summer. Additional catalysts for Disney reside in Disney Shanghai that is set to open later this month, and estimates are $3.7 billion – $6.2 billion in annual revenue with up to 50 million visitors per year. Considering its rich pipeline of movies, future theme park opening and legacy revenue from other segments, Disney appears well positioned for future growth.

Financial Strength and ESPN Worries

Disney has delivered impressive earnings over the past decade which was highlighted by the most recent quarterly report. Analysts have been fixated on the ESPN woes and the drop in its cable network and broadcasting segments. Per the previous earnings release, Bob Iger stated;

“The decrease at ESPN was due to higher programming costs, partially offset by an increase in advertising and affiliate revenues. Results for the quarter were negatively impacted by the timing of our fiscal quarter end relative to when College Football Playoff (CFP) bowl games were played, which resulted in an increase in programming costs and advertising revenues. Six CFP games were aired in the current quarter that were aired in the second quarter of the prior year. Increased programming costs due to the CFP games as well as contractual rate increases for NFL and college football programming were partially offset by the absence of rights costs for NASCAR. Higher advertising revenue was due to an increase in units sold and higher rates, both of which benefited from the CFP. Affiliate revenue growth was due to contractual rate increases, partially offset by a decline in subscribers and unfavorable foreign currency translation impacts.”

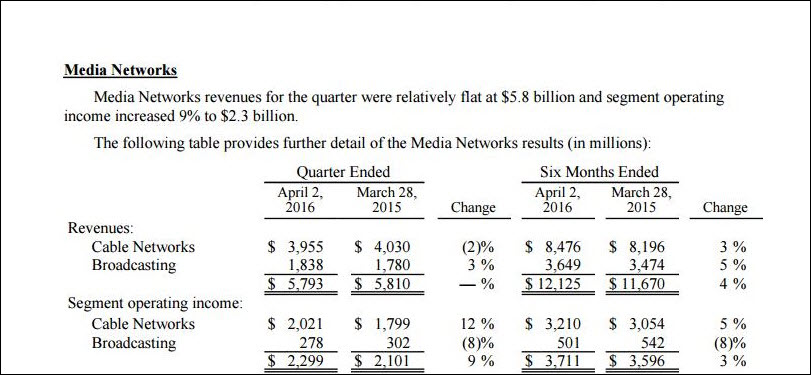

As Disney prepared to announce the most recent results and considering the above timing of ESPN broadcasting and Disney looking to monetize ESPN via alternative means, I’ll was looking for a capitulation in the ESPN decline and further acceleration in other segments. This appears to be the case as Media Networks posted a flat revenue number on a quarterly basis while over the same six-month period last year, revenue in this segment increased by 4% and operating income increased 3%.

Figure 4 – Media Networks detailed results

Conclusion

Disney represents great value with a rich pipeline of products and sustainable revenue stream from a variety of global franchises. Hasbro earnings may serve as a strong indicator for future Disney earnings over the long-term. Using this proxy, recent analyst upgrades, blockbuster movies, ESPN capitulation and Disney appears to have the wind at its back. Disney stock has been wrongly punished for revenue and income declines stemming from the ESPN franchise. I feel that Disney will continue to circumvent this ESPN specific issue and look to ways at evolving the offering (streaming via Sling TV) to the consumer and monetize ESPN via other means. The wildly successful franchises of Star Wars, Marvel, Pixar and the legacy Disney line are unappreciated. Disney has witnessed fantastic growth over the last decade and considering future catalysts in the pipeline; Disney appears undervalued at current levels. This presents a great buying opportunity in an inexpensive, high-quality growth stock that may not last much longer, currently sitting near the high $90s.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author holds shares of DIS and is long DIS. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.