The Mexican economy has been remarkably resilient to weakness in the US. Mexico’s exports to the US amounted to $295 Billion in 2015, a staggering 77% of total Mexican exports. Under such circumstances, one would expect the slowdown in US growth in the first quarter to tank the Mexican economy. Instead, robust growth in consumer spending allowed Mexico to grow at a fair pace of 2.6%, year-on-year. But now, as the tide in the US economy turns, the Mexican manufacturing sector, which suffered during the first quarter, could recover. Mexican GDP growth will move higher, and monetary policy will turn tighter. And the main benefiter? It’s the Mexican peso, which has been undervalued for quite a while.

How US Manufacturing Impacts Mexico

Mexico’s exports to the US are varied, ranging from beef to oil, yet the bulk of its US-destined exports are manufactured goods. Vehicles, vehicle parts, tractors, trucks and computer screens are among the manufactured items, and the list goes on. Transports and Machines are the top two categories and amounted to $186 Billion in 2015.

But here comes the tricky part—manufactured goods are also Mexico’s main import from the US. That is because Mexico is part of the supply chain for US manufactured goods which are shipped to Mexico for assembly and then exported back to the US. In effect, Mexico’s manufacturing sector is a satellite of the much bigger US manufacturing sector.

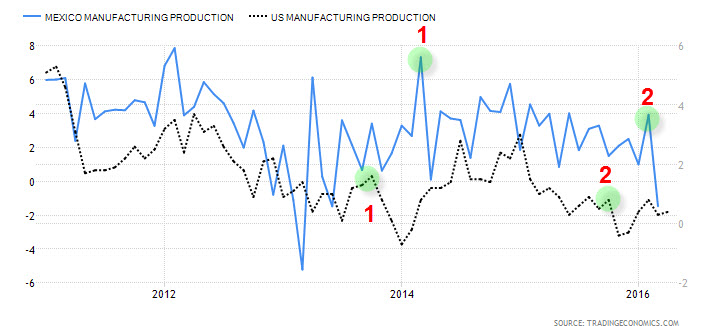

Once US manufacturing returns to growth so will Mexico’s manufacturing sector and, consequently, its contribution to Mexican GDP growth. The chart below illustrates the correlation between the two manufacturing sectors. US manufacturing moves first, and Mexican manufacturing follows slightly thereafter, both in descent and ascent. Although US manufacturing is still soft, it has returned to growth and the Mexican manufacturing sector will soon follow suit. As the US recovery gathers more and more momentum, the recovery in manufacturing will accelerate and the improvement in Mexican manufacturing will be even greater.

Chart courtesy of Tradingeconomics.com

Banco de Mexico Will Turn More Hawkish

The Mexican Central Bank, Banco de Mexico, is another key strength for Mexico and the Peso. Banco de Mexico at the helm of Agustín Carstens has been remarkably vigilant. Inflation, which had been rather volatile in years past, has stabilized. When the Mexican Peso was softer amid turbulence in the LATAM space, Governor Carstens reacted and hiked rates by 0.5% to 3.75%, in order to keep inflation from spinning out of control.

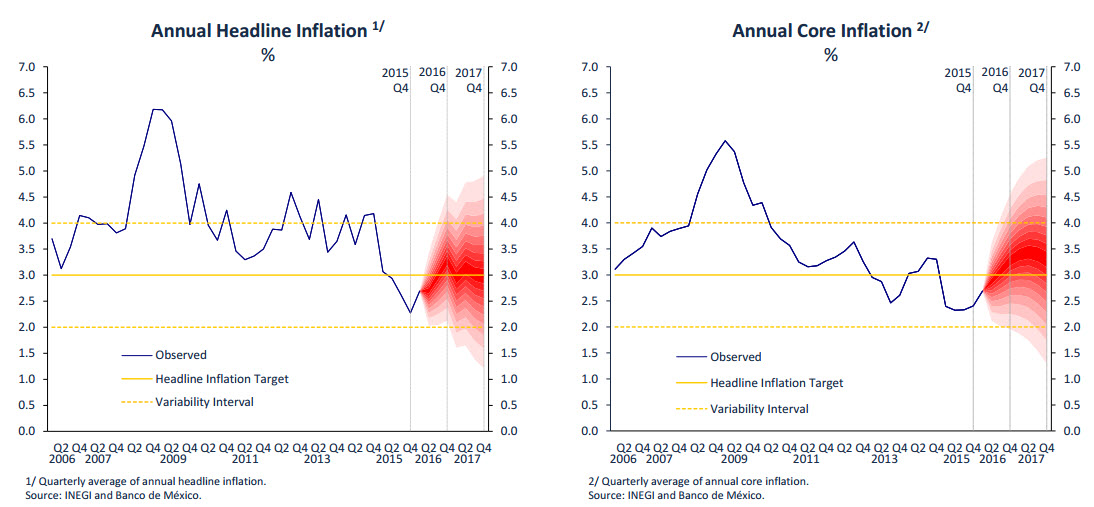

And yet, despite the rate hike in February, economic recovery is likely to pull inflation numbers even closer to the 3% target. As the chart from Banco de Mexico shows, inflation is already pretty close at 2.54%. This means there is a reasonable chance more rate hikes are in the cards. Which in turn will incentivise demand for the Mexican Peso even more.

Chart courtesy of Banco De Mexico

MXN vs. EUR and JPY

On the one hand, with the Fed rate hike coming closer and with the US and Mexican economy so interwoven, it will be risky to buy the MXN vs. the Dollar. On the other hand, buying the MXN against the EUR and JPY is a very different story. Both the European Central Bank and the Bank of Japan are light years away from tightening. 10-year bond yields in Japan are -0.1% and in Europe, yields on German 10-year bunds are at 0.14%. That’s a far cry from the Mexican 6.15% 10-year yield. Such a yield differential tends to stimulate strong carry trade flows into the MXN and out of the EUR and JPY. The vigilance of the Banco De Mexico and the improved growth outlook only reinforces the likelihood of that trend.

The MXN/JPY already shows signs of an impending rally while the EUR/MXN seems to be topping out, with the immediate targets for the MXN/JPY and EUR/MXN at 6.3 and 19.7, respectively. Of course, any unexpected turmoil in the markets or a sudden softness in the US economy could derail such a trend. Moreover, a Fed rate hike in June might spook investors If US economic growth is deemed too soft. And yet, despite all the risks and perils, the case for a higher MXN seems strong.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.