Risks of Saudi Arabia requiring a regime change are increasing, despite the OPEC production and non-OPEC production agreements. Fitch Ratings reduced Saudi Arabia’s rating to A+, the fifth-highest investment grade, and changed the outlook to stable from negative. The downgrade “reflects the continued deterioration of public and external balance sheets, the significantly wider than expected fiscal deficit in 2016 and continued doubts about the extent to which the government’s ambitious reform program can be implemented," Fitch said.

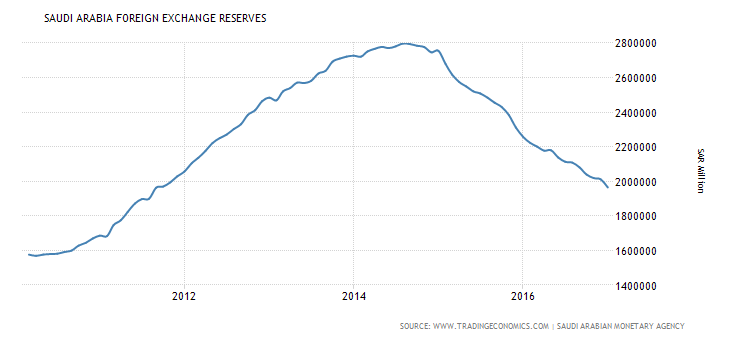

Saudi foreign currency reserves peaked at about $745 billion in 2014. They have dropped to about $525 billion, down $222 billion, or 30%. And despite higher oil prices in January, the reserves fell by $12.5 billion. The IMF has projected that the reserves may be entirely expended by 2020 if world oil prices do not recover sufficiently.

Note: The chart above provides reserves in SAR million

The government had budgeted crude prices in 2017 to average around $53 per barrel. I deduced that from the 2017 Budget of the Kingdom of Saudi Arabia (Page 21):

“Total revenues are expected to reach SAR 692 billion in 2017, a 31% increase compared to initial projections this year. Oil revenues are 20 estimated at SAR 480 billion, 46% higher than the 2016 projections… The increase in projected revenues and expenditure is primarily due to the energy pricing reform program, although this will be partially offset by the allowances for those citizens who need government support." (emphasis added).

But the problem is that KSA needs oil prices in the $60s to balance its budget, and that appears to be unlikely during 2017 due to the persistence of the global oil glut. The Energy Department reported that U.S. crude oil inventories reached a new record high of 533 million barrels, which is 32 million higher than a year ago. Crude stocks have risen by 54 million thus far in 2017.

American shale production is picking back up. Goldman Sachs predicts that output in the Permian basin will rise by about 300,000 b/d during the second quarter.

Libyan oil production has recovered to 700,000 b/d due to the end of fighting at a port. They are targeting 800,000 b/d by the end of April and 1.1 million barrel per day by August. Libya is not subject to OPEC’s production cuts.

Iraq has not cut its production as promised. It has predicted it will rise to 5 million barrels per day end of 2017, up 400,000 to 500,000 b/d.

Goldman Sachs recently wrote, "2017-19 is likely to see the largest increase in mega projects production in history. Led by U.S. shale, (this) could create a material oversupply in 2018-19.”

Vision 2030

Deputy Crown Prince Mohammed Bin Salman (“MbS”) unveiled a transformation plan last spring to diversify KSA’s revenues over time. The centerpiece of the plan is to list Saudi Aramco in an IPO during 2018. MbS said he thought the company has a valuation of $2 trillion, and so the sale of 5% would bring in $100 billion.

But a closer look at the company reveals that it does not own the oil reserves, which was the basis of his valuation. It has a monopoly on producing them, for which it pays the government a royalty of 20% and taxes of 85%.

I performed net present value calculations with the following assumptions (per barrel):

Price = $70

Royalty = 20% = $14

Production Cost = $10

Gross Margin = $46

Tax = 85% = $39.1

Net = $6.9

Volume = 10 million b/d

Period = 70 years

Discount Rate = 10%

NPV = $ 251 billion

This valuation is only 12.5% of the $2 trillion valuation desired. An IPO of 5% would yield $12.5 billion in proceeds, not the $100 billion being floated. Furthermore, investors would have to accept the sovereign risk, which would probably require a higher discount rate, further reducing the valuation. Khalid Al-Falih, the Saudi energy minister has said that the government will continue to make "sovereign decisions" regarding the company's production and investments: "(Investors) are going to have to accept it. It is part of the package."

Mr. Al-Falih recently said the government is studying the tax issue. But when I reduce the tax to 50%, the valuation rises to $419 billion, about 20% of the $2 trillion valuation. Wood Mackenzie Ltd has reportedly made a valuation of $400 billion. And so the Aramco IPO does not appear to be the “Hail Mary” pass that KSA needs.

According to a source who visits Saudi Arabia every week in business, there is private talk of regime change. Some royals have moved permanently to Europe. KSA cannot survive with prices in the $50s for many years.

In desperation, King Salman has traveled to Asia seeking investment. He was looking for partners who could list Aramco’s IPO.

Conclusions

Unless oil prices recover over the next few years, which seems increasingly unlikely, the royal family may transition away from supporting the kingdom. This could lead to civil unrest. The U.S. might need to get involved to keep the oil flowing.

U.S. Strategic Petroleum Reserves are over 690 million barrels and could be tapped if there is a disruption of supplies. Ironically, the are being drawn down about 200 million barrels over an eight-year period for budgetary reasons.

The risk of a regime change in KSA does create an oil price risk. It is a medium-term risk to keep in mind.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

20% royalties and 85% tax?

The royal family pays the taxes to themselves, do they not?

But who gets the royalties off the top? Is it paid to the US royal family for keeping the royal family in power?

Aramco pays royalties and taxes to the government (i.e., royal family). Not paid to U.S.

That is the problem Trump talked about during the campaign. KSA gets US protection without paying for its actual cost.