Leveraging Options

I’ve written numerous articles on options trading and how one can leverage options over the long-term to mitigate risk, generate income and accentuate returns. Leveraging options to supplement portfolio returns can make a meaningful impact on overall returns, especially over the long-term. Here, I’ll focus on covered calls and covered puts with corresponding lessons learned over the course of the past year with empirical data.

Covered calls are intended to leverage a stock position while extracting value on a consistent basis via selling option contracts against that position and collecting premium income in the process. I liken this to a landlord renting a room for monthly income, however, in this case, one is renting the stock. The option contract is structured with the option seller (stock owner) collecting a premium in exchange for the right for the option buyer to purchase the shares of interest at an agreed upon price by an agreed upon date for a premium (income that the option seller will receive). In this scenario, the stock owner doesn't believe that the shares will appreciate beyond the agreed upon price and thus be able to collect income while retaining the shares and dividend rights. The option buyer believes that the shares will appreciate beyond the agreed upon price and be able to buy the shares at a lower price than the market currently trades.

Covered puts involve leveraging a cash position that one currently has on hand and collecting a premium in exchange for the obligation to purchase one’s shares at an agreed-upon price prior to an agreed upon date. If the stock falls below the agreed-upon price prior to the agreed upon date, then the individual that bought the contract from you will force the obligation (that you agreed to) for you to purchase the shares. In this case (when the stock falls throughout the contract lifespan), the shares can be sold to you (the put option seller) at a higher price than the market. However, if the shares rise in value then the shares will remain with the owner and the put option seller will keep the premium income and the cash earmarked for the potential purchase of the shares will be freed. Why exercise the contract and sell the shares to you (option seller) at a lower price when one can sell the shares on the open market at a higher price?

Covered Call Objectives

- Collecting premium income: "Renting" out your stock for monthly income can be a great income generator over the long term. Assuming disciplined options are sold, the risk of relinquishing the stock in question decreases and retention of the shares and premium income increases.

- Mitigating risk: As the stock in question trades sideways and/or decreases in value, the premiums over time will mitigate the lack of appreciation and/or the decrease in value.

- Accentuating returns: As the stock trades higher over time, extracting additional value over the long run will accentuate these returns in a meaningful manner.

Covered Put Objectives

- Initiate a position: Initiate a position in a stock at a lower price in the future than the stock currently trades today via receiving a premium which will reduce the effective purchase price to below the current market value.

- Income: Identify stocks that have corrected and sell a covered put to receive a premium with the anticipation of the stock appreciating near the agreed upon contract price to capture the premium income and exit the contact. Thus no shares purchased and gains via premium income are realized. The earmarked cash plus the premium income can now be repurposed for subsequent trades.

- Lower Cost Basis: Adding to an existing position via a covered put contract – when a long position corrects, one can add to his position to lower the cost basis with the intent of being assigned shares at a lower effective price than they currently trade when factoring in the premium income. Essentially locking in this downward movement and being assigned shares to lower one’s cost basis when combined with a preexisting position.

Covered Calls – Successes (Facebook and Nike)

I've had many successful covered call contracts however it's very difficult to continuously generate income without the shares moving against you eventually. Here are two examples of long-term options income being generated on two of my long-term holdings, Facebook (FB) and Nike (NKE). My strategy is to sell options into strength to decrease the possibility of relinquishing my shares while extracting income and retaining the shares. For FB, I've been able to generate an additional $5.78 per share in income or $578 in cash leveraging this long-term position. For NKE, I've been able to generate an additional $1.94 per share in income or $194 in cash leveraging this long-term position while collecting the dividend and reinvesting over time. This translates into $772 in cash generation leveraging these two positions.

Covered Calls – Lessons Learned (Apple and AbbVie)

Apple (AAPL) and AbbVie (ABBV) were very difficult pills to swallow with unrealized gains far beyond the relinquished prices. As Apple started to trend higher after recovering from the low $90 range, I decided to engage in covered calls and had some wins however the upward trend was too strong, and I relinquished shares at $127 only to watch the shares rise to $160! I missed out on $33 per share or $3,300 in appreciation based on this 100-share block! ABBV had moved from higher from the low $60 range to the mid $70 range and had some wins however the upward trend was too strong once again, and I relinquished shares at $73 only to watch the shares rise to $96 with no news really at all! I missed out on $23 per share or $2,300 in appreciation based on this 100-share block! This translates into $5,400 in total lost unrealized gains on these two long-term positions. Hindsight is 20/20, and as a result, I prefer to engage in covered puts as theoretically stocks and move infinitely higher.

Covered Puts - Successes

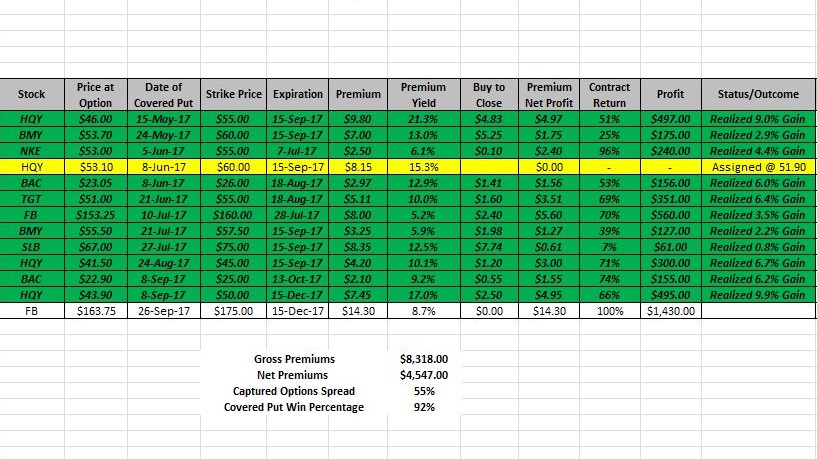

I typically select high quality, large-cap household names when engaging in selling covered puts. Typically, I identify companies that have sold-off in a meaningful way due to extraneous circumstances or a marginal miss in an earnings report. These companies are ones that typically pay dividends, engage in share buybacks, acquisitive mindset and still growing revenues. Examples of these opportunities include but are not limited to Starbucks (SBUX), Disney (DIS), CVS Health (CVS), Apple (AAPL), Bristol-Myers Squibb (BMY), Nike (NKE) and Target (TGT) to name a few companies that have witnessed huge sell-offs while the underlying business model remains fundamentally intact. Inevitably, these stocks appreciate to pre-selloff levels usually within a short period of time. Below is a laundry list of examples over the past year where the assignment is very rare and in the event of being assigned, I was able to still sell at a profit (Figure 1). Figure 1 shows a subset of my 2017 covered put contacts with results and out of the most recent 13 contracts, 12 of them have been wins (92% win rate) with a premium capture of 55% and a net income gain of $4,547 (including the FB pending contract as this is already in-the-money).

Figure 1 – Subset of 2017 covered put contracts and results

Summary

Covered calls and covered put options can be very valuable regardless of objective since these instruments provide optionality with regard to generating income, mitigating risk, accentuating returns, initiating a position, generating income and lowering cost basis of an existing long-term position. I’ve shown empirical examples of each option strategy behind the trades. Covered calls are inherently more risky in the sense that stocks can infinitely increase through the agreed upon price and the shares will be relinquished as in the case with AAPL and ABBV. With regard to covered puts, limiting one’s option trading to large-cap, dividend-paying household names can mitigate risk as these companies have history of resiliency, dividends, share buybacks and major acquisitions to drive growth. Based on my empirical data over the past year of engaging in options trading, I tend to favor covered puts.

Thanks for reading,

The INO.com Team

Disclosure: The author is long Disney, Facebook, Nike, Target and Starbucks. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.

RE; Complaint about being assigned a stock on a covered call and missing the big upside... why not just buy back the stock on the open market. You may wait for a pull back as nothing goes straight up, or just buy in, possibly miss a point or two but still capture the large gain you are complaining about missing?

About 3 comments on that question.

1: First and foremost, because whatever ramps the daylights out of the stock you sold calls against happens while you're in the dark. It gaps up $5 over your sold strike. By the time your neurons see and comprehend it, it's done. Depending of course upon which strike you sold.......because some people START a position selling ITM calls to protect their downside and then add more stock on a pullback......some people sell ATM calls looking to get max vol in the call value because ATM options have the greatest sensitivity to vega, or, they sell OTMs, looking for "rent" hoping not to be called. The selection of call strike you sell is dependent upon your market outlook, which can be wrong or right. Nobody can predict the future. Many people cannot handle the present! (just kidding but not really)

2: Because when you do that, the thing that compels you to do that is you see the stock "running away" from you. Otherwise you'd leave it alone, right? Think, here, about psychology, not just price. One of the definitions of "volatility" that I really like is "market price action that makes people act". So, you sold the call for $2 and now you are thinking about buying it back for let's say $5. Or $8. Or if you sold BIO calls today....$38.

3: WHILE THIS IS GOING ON your brain has been twisted into a pretzel because you wanted the stock but you didn't want to sell it but now you want it more because it has gone higher but you would have never bot the stock $8 higher so you think "I'll just let it go" but you really wish you hadn't sold the calls and now you start thinking about chasing the stock but it has to pull back and I'll buy it then but what if it doesn't?

When you do this. And you do it a lot. And it becomes a habit. You will be and feel left behind and that damned number in the lower right hand corner of your statement will go nowhere, probably bleed off over time and then take that big hit THAT YOU CAN'T RECOVER FROM because you are addicted to selling those stupid CCs and you ABSOLUTELY CANNOT hit a home run. Selling CCs is a virtually guaranteed recipe for mediocre performance, because in the end, it is a formula for NOT LOSING. It is a formula born of fear of the market. And I will say to you or anyone else: Go do 100 covered call plays and get back to me. IF YOU ARE SMART enough to "only do those few and infrequent CC plays where it makes sense" then you are smart enough to do much sharper plays.

People who like covered calls should visit radioactivetrading.com and learn about collars. They are superb and have enough free training to make the site completely worth it. Learn about collars.

Gained lot of knowledge by reading the blogs above. Very insightful.:

Al Pecherer

Could you provide the name of the service you mention " I subscribe to a service that does maybe 40 plays in a month, long calls only. "

S.V. Murthy

"Trading Addicts" Jeff Kohler. I think it's tradingaddicts.com

Now I am going to disagree with you. You say CCs "mitigate losses". ENORMOUSLY imperfectly. So imperfectly that I have to object to the thought. This is a thing that CC sellers do not fully understand. Selling CCs amounts to selling a dime for 9 cents; and in this record low vol market, more like about 8.2 cents. There is no call any CC seller would sell with a delta of 1.00. By definition. Sure, you could buy a $50 stock and sell a $20 call. Purposeless. Once the calls are sold there is one and only one outcome that makes the play a good play. And that is the passage of time while the underlying does not decline too far. Most CC sellers will buy a $50 stock and sell a $50 call. With a delta of .50, such a call will fall in value by 50 cents for every dollar the underlying falls. Suppose the u'lying falls by $5. OK, the short call loses 2.50. OK, to that extent, your loss is mitigated. Now suppose the u'lying falls another $5. Now, the short call at 50 against a stock (now) at 45 has a delta about .28. So *as the underlying falls, the ability of the sold call loses its ability to mitigate losses falls, and that protection stunk in the first place, being only 50% effective. Every CC seller has had this experience: you bought the stock at 50, the stock fell to 40, that call you sold at 50, you should not have to pay ANYTHING to buy it back. But you do! Or if don't wish to buy it back, you are stuck in your crappy stock! Because while your underlying is falling, the overwhelming majority of CC sellers do NOT have permission to sell calls naked, therefore they can NOT place a stop loss order under their stock without first closing out (buying back) the short call!

So you say, "well, don't do this on stocks that you do not really want to own". Errr, if you really want to own the stock (regardless of price performance) then DON'T SELL PART OF IT by selling a covered call!

Habitual sellers of covered calls will find that the inability to control losses in the above circumstance will impose a loss amounting to the proceeds of 3-4-5 covered call sales. Just talking about that number in the lower right corner, the only one that matters.

What is the service you subscribe to please???? Thank You!!!

Noah, Jim was replying to me.

I agree with you, generally. The BIGGER consideration is whether you want to employ an "infrequent big win" or "frequent small win" strategy across your portfolio. In the short term, CCs look great. And though I use them all the time....they.....SUCK. CCs are a formula that produces sub-average portfolio results long term and I say that as one who has probably done well over 2500 CC trades. The fact of the matter is, they completely eliminate the possibility of home runs. In a low volatility market, selling options simply does not generate the premia required to compensate for the risk. Anyone who is a wild proponent of CCs, I always say the same thing. "Do 100 CC plays and get back to me with whether you still like them".

I subscribe to a service that does maybe 40 plays in a month, long calls only. Fully 1/4 of them go to zero. 4 of them are 5-8 baggers. 10 of them double. About 15 are breakeven. This strategy produces 25+% gains per month and sometimes 40%. You just have to have the stomach to see a lot of failures and the discipline to allocate exactly the same amount to each trade.

Even though I sell CCs a lot and do debit spreads a lot, it is my opinion that excess use of CCs produces mediocre results simply because you can NEVER EVER hit a home run but you CAN suffer ghastly losses. You can overthink it 5000 times beyond that simple statement but the math is inescapable.