Options can provide an alternative approach to the traditional buy and hold for the long-term strategy. Options can add value to one’s portfolio in a variety of ways, specifically, maintaining liquidity via maintaining cash to engage in covered put options, initiating positions via being assigned shares strategically prior to or upon expiration of the option contract and capturing premium income via closing out the contract prior to expiration as the shares move in your favor to realize income. Here, I’ll discuss these three different scenarios and strategies behind each one with real life examples.

Maintaining Liquidity and Capturing Premium Income

Maintaining liquidity is integral to any portfolio as cash can be deployed in opportunistic scenarios to capitalize on sell-offs or adding to a long position that has corrected to lower cost basis. Covered puts can be implemented as a means to leverage cash on hand to sell contracts that are covered by cash. This cash would be deployed in an effort to maintain this cash balance yet be put to work via an option contract. This cash reserve can be utilized for selling covered puts thus not purchasing the underlying security with the end goal of never being assigned shares and netting premium income in the process. Once the contract expires, the covered cash allocated to the contract will be freed in addition to the cash that was realized from the option premium at expiration. This scenario will allow cash reserves to be maintained while adding cash via covered put contracts.

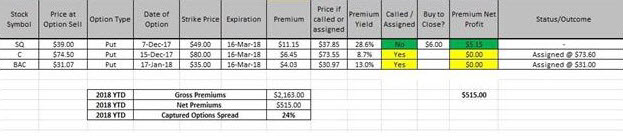

It’s important to bear in mind that covered puts shouldn’t be sold unless one wouldn’t mind being assigned shares in the underlying equity. Additionally, restricting covered put contacts to high quality, large-cap, dividend-paying companies will help to mitigate risk and decrease the likelihood of assignment in order to maintain liquidity and add to the cash on hand. Recently, I decided to target Square (SQ), a high growth stock with large option premiums that had sold off from $49 to $39 prior to its recent run-up to $55. Considering its growth and a 20% sell-off from its highs, I elected to sell a put option contract with a strike of $49 (hoping to retrace its highs at the time of selling the contract) for a premium of $11.15 per share of $1,115 for the contact income (Figure 1). As the shares approached the strike price of $49, I elected to buy-to-close the contract for $6.00 to net a realized income of $515 in cash and free up the previously allocated $4,900 for the contract. This realized $515, yielded a 10.5% return on the trade, however, had I waited until expiration I would’ve netted the entire premium as Square broke through the $49 strike price before expiration. The end goal is to capture premium income and maintain liquidity which was accomplished before the expiration of the contract, so I decided to accelerate the closure of the contract and walk away with a double-digit gain.

Strategically Initiating Positions

Covered puts can also be employed to initiate a position in a company that shows a compelling long-term buy. Why purchase shares at current prices when one can purchase shares marginally cheaper in the future? In this way, if the shares maintain current levels, then assignment will be no harm, no foul since shares were desired anyway. If the shares move in your favor (in this case the shares appreciate in value) the put seller has optionality where he can be assigned at an immediate unrealized gain on the shares or sell the contract to close out the option at a profit without being assigned. Either way, the option seller nets an unrealized gain or realized gain via assignment of shares at a lower price than when the option was sold/current market value or premium income via the closure of the contract, respectively.

Like analysis from Noah Kiedrowski?

Get Our Free Political Plays Newsletter

This free, bi-weekly newsletter from Noah Kiedrowski will give you actionable stock plays based on political action. Spot and profit from the political plays that matter.

Banks are in the sweet spot with the confluence of reduced corporate tax rates, repatriation, deregulation and long-term tailwinds of rising interest rates. Given the above strategy and rationale for engaging in covered puts for strategically initiating positions in banks, I elected to sell put options on Back of America (BAC) and Citigroup (C). My objective was two-layered. Ideally, assignment of shares would occur at an unrealized gain, or I’d elect to buy-to-close the option contract to capture the premium income if the shares appreciated beyond the strike price.

I decided to sell put options on BAC and C when the shares were trading at $31.00 and $74.50, respectively (Figure 1). BAC and C were trading at $32.17 and $73.47, respectively upon assignment. Shares of BAC and C were assigned at effective purchase prices of $31.00 and $73.60, respectively. As demonstrated below and consistent with the objectives put forth, both assignments led to an immediate unrealized gain with BAC and a no harm, no foul assignment of C.

Figure 1 – Details surrounding the three put options that were sold highlighting the above strategies

Conclusion

Options can be leveraged in a variety of ways to maintain liquidity, strategically initiating a position and capturing premium income. Regarding maintaining liquidity and capturing premium income, I decided to choose Square, a high growth stock with large option premiums that had sold off 20% from its highs. I elected to buy-to-close the contact to net a 10.5% return. The end goal of capturing premium income and maintaining liquidity was accomplished. Since banks overall are uniquely positioned to greatly benefit from the combined legislative initiatives in taxation, repatriation, and deregulation with an additional tailwind of a rising interest rate environment, I strategically entered two positions via assignment of Back of America and Citigroup. Collectively, depending on one’s strategy, he can leverage put options to augment his portfolio in the discussed scenarios.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares of BAC and C and is long both holdings. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.