Occasionally, businesses undergo corporate restructuring for various reasons. Often this involves spinning off a separate, independent entity to potentially unlock value for shareholders over the long term. Some notable spin-offs include Dow from DowDuPont, Alcon from Novartis, Otis Elevators from United Technologies, and VMWare from Dell. When company spin-offs occur during an options expiration cycle, this can complicate the normal lifecycle of a pending options contract. When this happens, these options are denoted as "adjusted" with the corresponding ADJ within the options chain. One of the most recent notable spin-offs was Kyndryl (KD) from International Business Machines (IBM), as these two broke apart and traded as separate entities during an actively pending option contact. The share split ratio changes the deliverable of the option contract and thus requires normalizing the two entities relative to the original contract value when adjusting for the new strike price. This normalizing is necessary as shares may ostensibly be in the money; however, as a function of the share split ratio, the option contract is out-of-the-money and not assignable.

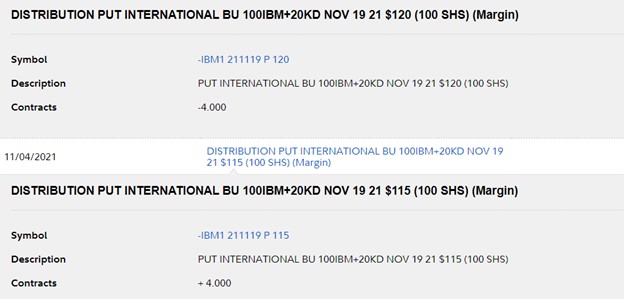

Figure 1 – IBM spin-off of Kyndryl and its impact on pending options as seen via a Trade notification service - Trade Notification Service

Breaking Down An Adjusted Option

IBM completed a business spin-off of (KD) that publicly traded as a separate company. The share spin-off was a 1:5 share split translating into every 100 shares of IBM; the shareholder also receives 20 shares of KD. As such, any options that were active during the spin-off experienced a deliverable change that was equivalent to 100 shares of IBM plus 20 shares of KD.

Let's walk through a put spread that was sold on IBM prior to the announced spin-off. The $120 strike was sold, and the $115 strike was bought for protection to take in a net credit. During the option lifecycle, IBM announced the Kyndryl spin-off, which changed the complexion of the option trade.

The original trade was sold with agreeing to buy IBM shares at $120, and the option buyer would be obligated to deliver shares at $120 per share. Factoring in the KD spin-off, the option buyer would now be obligated to deliver 100 shares of IBM and 20 shares of KD due to the 1:5 share split.

As long as the combined value remains above $120 per share, then the contract remains out-of-the-money and cannot be assigned even if shares of IBM trade below the original $120 strike. Put another way, if IBM trades below $120, but the added 20 shares per contact bring the value of the contract above $120, then shares will not be assigned as the collective value of the contract exceeds $120 per share.

Different Scenarios

Scenario A: IBM trades at $120, and KD trades at $20 per share; the deliverable translates into IBM being worth $124 a share if you normalize to IBM shares only after factoring in the KD worth. The KD portion can be calculated out by taking the 20 shares and multiplying by $20 per share, and then dividing by 100 shares since it was a 1:5 split. This simple math works out to $4 per share of intrinsic value for the option contract. In this case, since the combined deliverable remains above $120 per share and the contract is out of the money and cannot be assigned even though IBM is exactly at the $120 strike because the combined value is actually $124.

Scenario B: IBM trades at $117, and KD trades at $20 per share; the deliverable translates into IBM being worth $121 a share if you normalize to IBM shares only after factoring in the KD worth. In this case, since the combined deliverable remains above $120 per share and the contract is out of the money and cannot be assigned even though IBM is below the $120 strike because the combined value is actually $121.

Scenario C: IBM trades at $115, and KD trades at $20 per share; the deliverable translates into IBM being worth $119 a share if you normalize to IBM shares only after factoring in the KD worth. In this case, since the combined deliverable is now below the $120 per share and the contract is in the money and can now be assigned because the combined value is actually $119.

Actual Outcome

A put spread was sold with a $120 strike and a $115 protection strike for a risk-defined put credit spread. The combined value of the IBM/KD deliverable remained out of the money, and the option was closed out to realize a profit just as any normal option contact would be closed out.

Figure 1 – The “adjusted” option of IBM’s spin-off of Kyndryl and its impact on pending options as seen via a Trade notification service - Trade Notification Service

Conclusion

When company spin-offs occur during an options cycle, this can complicate the normal lifecycle of a pending options contract. When this happens, these options are denoted as "adjusted" with the corresponding ADJ within the options chain. One of the most recent notable spin-offs was Kyndryl (KD) from International Business Machines (IBM), as these two broke apart and traded as separate entities during an actively pending option contact. The share split ratio changes the deliverable of the option contract and thus requires normalizing the two entities relative to the original contract value when adjusting for the new strike price. This normalizing is necessary as shares may ostensibly be in the money; however, as a function of the share split ratio and the combined value, the option contract is out-of-the-money and not assignable.

Disclosure: Stock Options Dad LLC is a Registered Investment Advising (RIA) firm specializing in options-based services and education. There are no business relationships with any companies mentioned in this article. This article reflects the opinions of the RIA. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. The author encourages all investors to conduct their own research and due diligence prior to investing or taking any actions in options trading. Please feel free to comment and provide feedback; the author values all responses. The author is the founder and Managing Member of Stock Options Dad LLC – A Registered Investment Advising (RIA) firm www.stockoptionsdad.com defining risk, leveraging a minimal amount of capital and maximizing return on investment. For more engaging, short-duration options-based content, visit Stock Options Dad LLC’s YouTube channel. Please direct all inquires to [email protected]. The author holds shares of AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY, and USO.