The financial sector is poised for a very strong rally into the end of 2021 and early 2022 as revenues and earnings for Q4:2021 should continue to drive an upward price trend. The US Federal Reserve is keeping interest rates low. At the same time, the US consumer continues to drive home purchases and holiday shopping. Strong economic data should drive Q4 results for the financial sector close to levels we saw in Q3:2021. If that happens, we may see a robust rally in the US Financial sector over the next 45 to 60+ days.

The strength of the recent rally in the US major indexes shows just how powerful the bullish trend bias is right now. Some traders focus on the downside risks associated with the US Federal Reserve actions and/or the concerns related to inflation and global markets. I, however, continue to focus on the strength in the US major indexes and various sector trends that show real opportunities for profits.

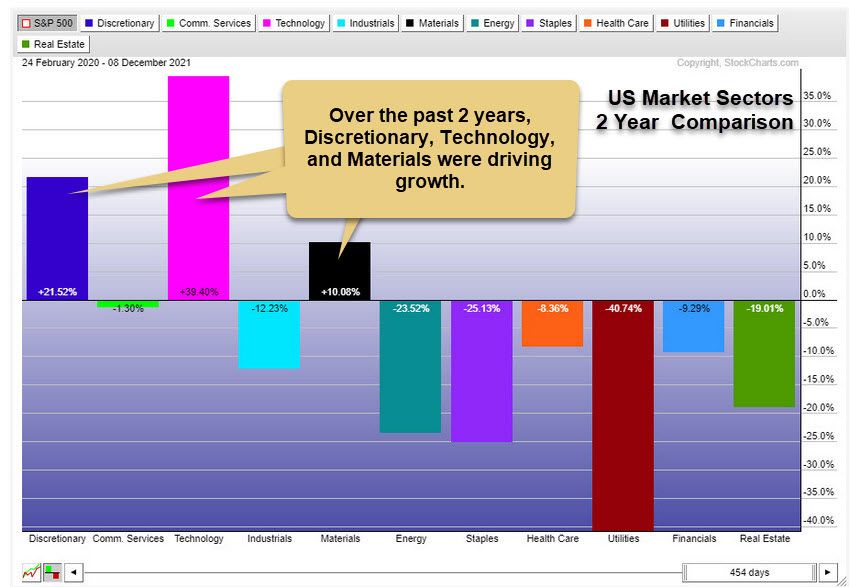

Comparing Sector Strength

The following two US market sector charts highlight the performance over the last 12 vs. 24 months. I want readers to pay attention to how flat the Financial Sector has stayed since just before the 2020 COVID event and how the Financial Sector has started to trend higher over the past 12 months. This is because the shock of COVID briefly disrupted consumer activity. Yet, consumers are coming back strong, driving retail sales, home sales, and the continued strong US economic data. Therefore, it makes sense that the Financial sector should continue to show firm revenue and earnings growth while the US consumer is active and spending.

Over the past two years, Discretionary, Technology, and Materials drove market growth compared to other sectors. Remember, the initial COVID virus event disrupted market sector trends over the last 24+ months.

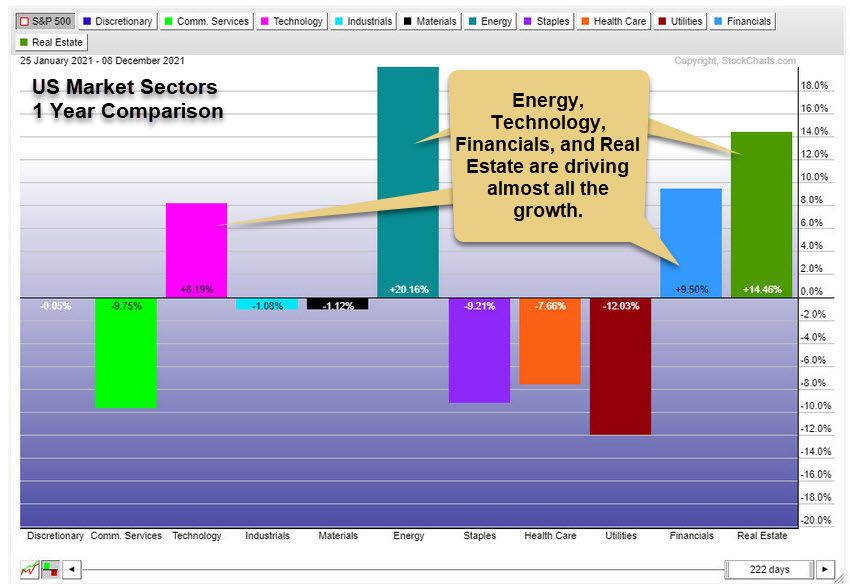

Taking a look at this 1 Year US Market Sector chart shows how various sectors have rebounded and how the Discretionary and Materials sectors have flattened/weakened.

Pay attention to how the Energy and Real Estate sectors have been over the past 12 months. Also, pay attention to how the Financial sector is strengthening.

I believe that the continued deflation/deleveraging that is taking place throughout most of the world will continue to drive global central banks to stay relatively neutral regarding rising interest rates. This will likely prompt an easy money policy throughout most of 2022 and drive continued revenues/earnings for sectors associated with consumers’ engagement with the economy.

If inflation weakens into 2022 while wage and jobs data stays strong, we may see more moderate strength in the Financial, Healthcare, Discretionary, and Technology sectors over the next 6 to 12+ months.

Read more about Global Deleveraging Here: Delivering Covid Bubble Possible Volatility Risks In Foreign Markets

Fiancials May Pop 11% Oo More Over The Next 6+ Months

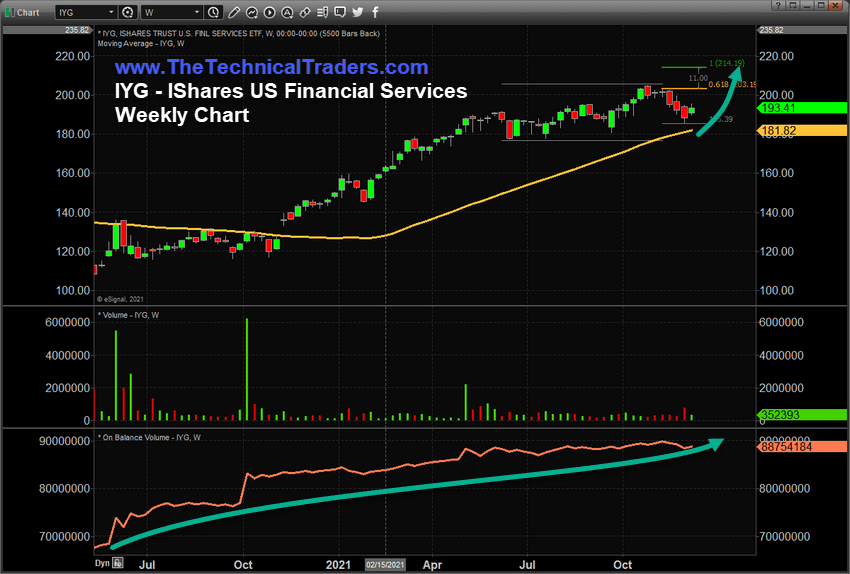

This Weekly IYG, IShares US Financial Service ETF, highlights the recent sideways price trend in the Financial sector and the potential for a 9% to 13% rally that may take place as the markets shift into focus for the Q4:2021 earnings. Yes, inflation is still a concern, but as long as the US consumer continues spending and engaging in the economy, the Financial Services and US Banks should show strong returns.

If the US markets rally into the end of 2021, possibly reaching new all-time highs again, this trend may carry well into 2022 and drive Q4:2021 and Q1:2022 revenues and earnings for the Financial sector even higher.

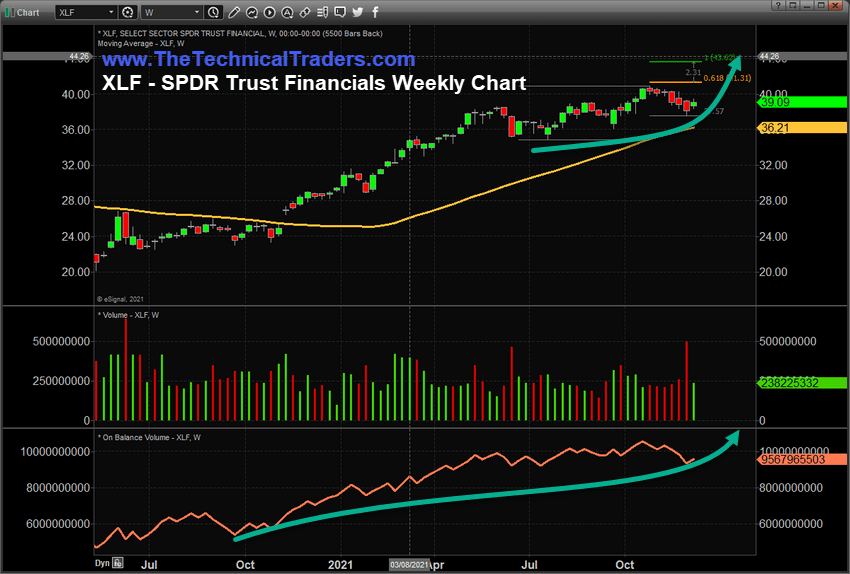

This Weekly XLF chart shows a very similar setup to IYG. I firmly believe the recent fear in the markets related to the US Federal Reserve, the new COVID variants, and the global markets deleveraging process is missing one critical component – the strength of the US markets and the strength of the US Dollar.

As the rest of the world struggles to find support and economic strength, the US markets continue to rebound on the strength of the US consumer, the recovering economy, and the growth of these sectors. As long as the US Federal Reserve does not disrupt this trend, I believe Q1:2022 could be much more robust than many people consider. I also think the deflation/deleveraging process will work to take the pressures away from recent inflation trends.

What Could This Mean For 2022?

Early 2022 may well work as a “rebalancing” process for the global markets – possibly taking the pressures away from the strength in energy, commodities, and staple products/materials. This means pricing pressures will decrease while consumers are still earning and spending. The Financial sector should benefit from these trends over the next 6+ months.

Watch for the Financials to start to increase throughout the end of 2021 and into early 2022. There are many ways to consider trading this move, but ideally, I think the rally will take place before the end of February 2022.

Q1 is usually relatively strong, so that this trend may last well into April/May 2022. It all depends on what happens that could disrupt the current market sector trends. If nothing happens to disrupt the strength of the US Dollar and the strength of the US markets, then I believe the Financial Sector has a very strong opportunity for at least 10% to 11% growth.

You don’t have to be smart to make money in the stock market; you just need to think differently. That means: we do not equate an “up” market with a “good” market and vi versa – all markets present opportunities to make money!

We believe you can always take what the market gives you and make CONSISTENT money.

Learn more by visiting The Technical Traders!

Chris Vermeulen

Technical Traders Ltd.

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation for their opinion.