Yep, it's the same old story; once again, Japan is just muddling through. Private consumption is weak and inflation is practically non-existent. And inflation could get worse with the latest plunge in oil prices. And with Japan barely slogging through, investors' call for the BoJ to amp its efforts are on the rise.

So what's the problem? In the eyes of the BoJ, the situation isn't really bad enough to require further intervention.

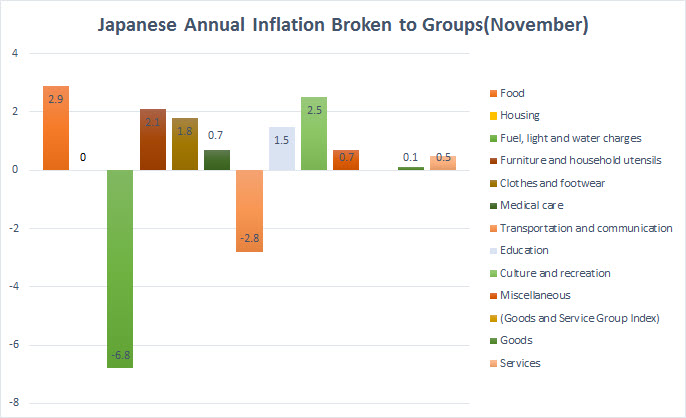

What The BoJ Sees

So why wouldn't the BoJ want to add any more gunpowder to an already aggressive stimulus plan? The answer comes in two parts.

The first part was covered extensively in my last article and thus needs little elaboration. That is the BoJ wants the Abe government to shoulder some of the burden. It needs to fulfill its own side of the bargain and push forward much needed financial reforms.

And the second part? The BoJ wants to hold some gunpowder in its arsenal... just in case things get worse. With the Chinese stock market meltdown radiating across the world, the BoJ wants to make sure it has enough "weapons" to unleash. But so far, in the eyes of the BoJ, it's not yet bad enough to risk the economy.

Chart courtesy of The Statistic Bureau of Japan

Let's take a quick look at the latest key data. November's inflation figure (annualized), albeit rather low, still wasn't the textbook definition of deflationary pressures. From a total of 10 various segments, from food to energy to housing, only transportation and energy fell on an annual basis while Housing prices were unchanged at 0%. Despite the dismal numbers, for deflation to be a risk, prices of most items need to fall. And as the chart below shows, that has yet to happen.

Moreover, when the BoJ examines GDP growth it has bounced back to 1.6% YoY. Now while that's not exactly mind-blowing, it's not "dangerous" either. Especially when GDP is measured on a Per Capita basis which takes into account Japan's shrinking population.

For those reasons, the BoJ prefers to push the 2% inflation target further before escalating already "aggressive efforts" to stimulate the economy.

What Investors See

While the BoJ is busy maintaining its creditability and gunpowder, investors, including this writer, see things a bit differently.

For example, Japan's consumer confidence index is stubbornly below 50 which signals subdued consumer spending. As can be seen in the chart below, things are not looking well. The figures point to a clear deflationary bias in Japan. That is especially true when we consider that savings, as a percent of GDP, is higher.

Chart courtesy of Tradingeconomics.com

And because Japan's sovereign debt is so overwhelmingly large, most of those savings are sucked up to fund the government. Japan's corporate sector is itself a big net saver and that is also being used to fund Japan's massive debt of 230% of GDP.

Of course, in practical terms, it means the Japanese public and private sector are holding too much Japanese government bonds. The only way to reduce that amount would be to make fewer bonds available. That way, Japanese corporates and individuals would be forced to buy riskier securities. In turn, that would push the wheels of inflation and start it moving back up.

How could that be accomplished? Simply put, the BoJ needs to buy government bonds to reduce the amount available for purchase. So far, the amount that has been bought by the BoJ has been staggering, at roughly $600 billion worth each year. But with Japan's government producing a deficit of roughly $300 billion annually, much of the QE effect is being negated.

It's a classic Catch-22 scenario: A higher government deficit means more government bonds. And that pretty much defeats the whole purpose.

Clearly, that means that the BoJ needs to act even more aggressively. It prefers to wait for things to worsen before tilting towards more QE and satisfying investors.

Thursday's Data Will Be Handy

Because there is some dissonance between what investors and the BoJ are thinking you might presume JPY trade is stuck. But there's no need for despair. If there's any indication that things are getting worse, that will increase the chance of BoJ action which should be enough for more easing.

This brings us to Thursday when Japan's CPI data for December is due out. As previously mentioned, the BoJ wants to see most of the items measured in CPI fall in price. Only then will it turn on the deflation alarm and unleash more stimulus.

Now, don't expect that to happen in Thursday's release. However, it should be enough to see that more items fell in price compared to November. That's an indication that we are going there, i.e. a deflationary trend. And as you know, that is just what investors need to make the first move and push the JPY onto another bearish wave.

So hold on to your guns; while Yen trade has been dull lately, the change might be nearer than you think.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.