Commodity prices are facing a shift. As inflation heats up and growth stabilizes, the commodity arena is gradually tilting in favor of growth-oriented commodities such as Oil and Copper Meanwhile, commodities associated with inflation protection, e.g., Gold and Silver, are not only losing their allure but face growing sell pressure.

The thought of selling precious metals just as inflation is showing signs of coming back may sound counter-intuitive. After all, precious metals are one of the more well-known methods of hedging against inflation. So, why are precious metals tanking just as inflation is coming back?

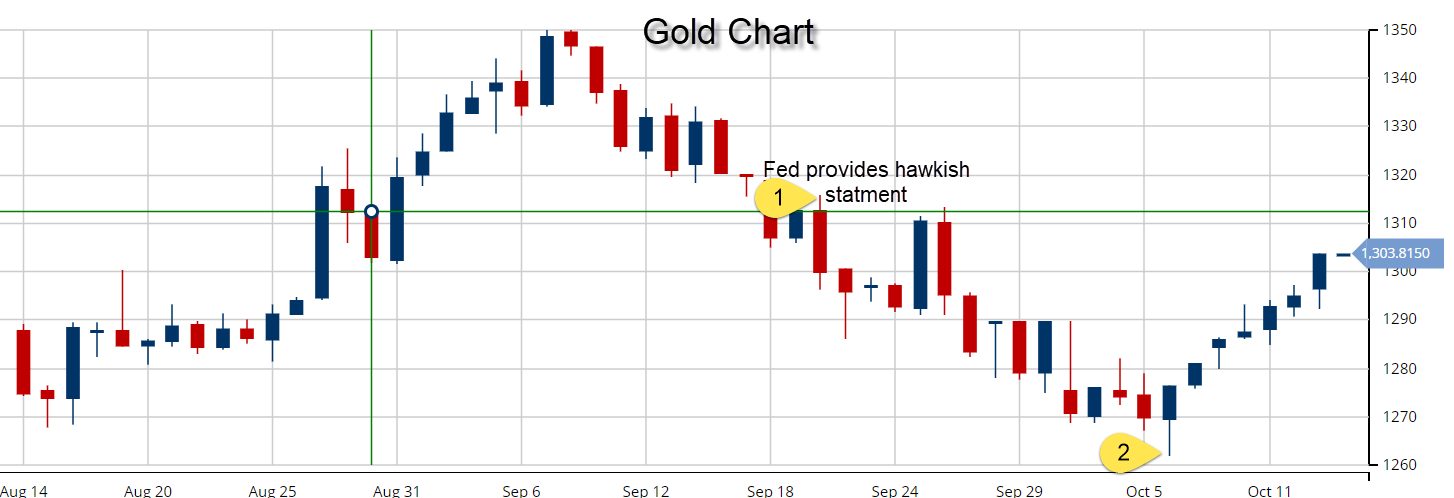

Because the capacity of precious metals as an inflation protection method emerges when investors believe that inflation is understated in the official numbers. When inflation becomes fact, we begin to see the classic, "buy on rumor, sell on fact" response; i.e., investors start selling precious metals. Since Gold and Silver do not pay interest, their investment appeal decreases when rates rise. But, when inflation is under-reported, effective rates are lower and the value of the currency, in our case the Dollar, is eroded. And, in this case, precious metals gain appeal for preserving value and as an alternative investment. That would explain Gold’s price surge from July $1,210 an ounce in July to $1,350 in September, when US headline inflation numbers caught the market off guard with a fall to from 2.7% in February to 1.6% in June, meaning inflation was understated.

This dynamic also explains the fire sale that hit precious metals in the aftermath of the Fed's September rate decision. The Fed signaled a rate hike as soon as December and another three in 2018. Gold responded by shedding 3.6% in two weeks.

Chart courtesy of MarketClub.com

All the while, the rest of the commodities space was holding rather well in the face of higher rates. In fact, in aggregate, excluding precious metals, commodities prices were gaining. One good example is the iShares S&P GSCI Commodity-Indexed Trust ETF (GSG), which embodies exposure to the broad commodities market from energy and agriculture to precious metals and gained 0.54% during Gold's selloff.

What's Next?

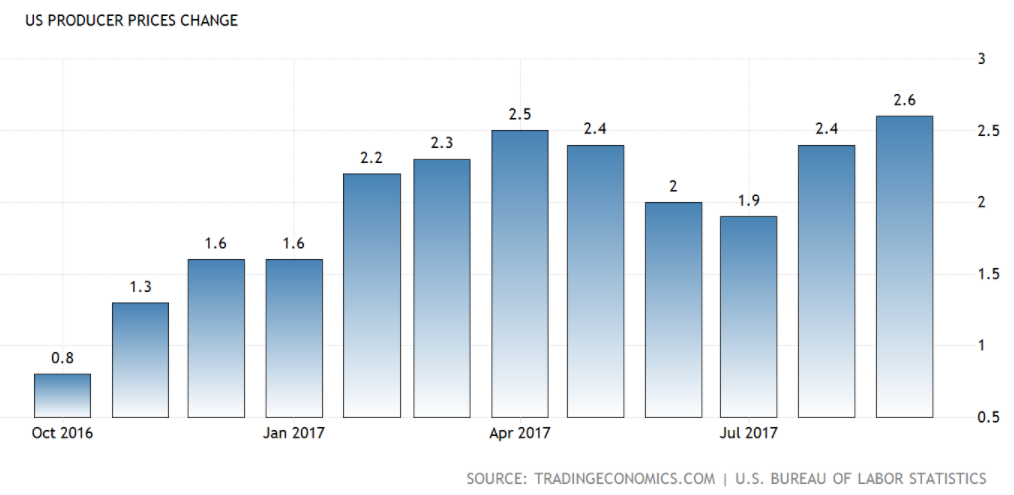

Earlier this week, the minutes of the Fed's September meeting were released. What they revealed was the Fed members' collective concerns over inflation potentially falling, thus countering the hawkish statement that came on the 20th of September, the day of the actual rate decision. The overall picture hasn't changed; the Fed still foresees the possibility of a rate hike in December and another three over the next year. Meanwhile, headline inflation bounced back to 2.2% in September, while September producer prices jumped by 2.6% year-over-year, after a 2.4% year-over-year gain in August. Together, that paints a hawkish inflationary outlook and, therefore, a bearish outlook for precious metals.

Chart courtesy of Tradingeconomics

Buy The Stocks Not The Futures

Although upon the surface it may seem that an investor would do better to just buy exposure to the rest of the commodities segments, e.g., energy and agriculture, the reality is not quite so simple. That is because an ETF which holds commodity futures (or any ETF that holds futures), with all its hefty rollover fees, is simply not a very good long-term strategy.

On the other hand, with ETFs that hold stocks of commodity miners, traders and/or producers, a different story emerges, especially if their valuation is historically low. In that case, the ETF can provide an upside on an earnings yield basis. ETFs, such as the SPDR S&P Global Natural Resources ETF (GNR), that provides exposure to the broad area of commodity producer stocks, and it trades at a 16.6 P/E with a 2% dividend yield, or the SPDR S&P Metals & Mining ETF (XME) that holds a diversified exposure to metal producers and trades at a 10.62 P/E. When we stack up to those two ETFs again the 25.46 P/E of the S&P500, we can at least conclude that we are getting exposure to commodities at a cheap valuation. True, at times, commodities do outperform the companies that mine and producer them. But, with the P/E multiples so low for miners compared to the rest of the stock market, this time around, miners are cheap and may, in fact, provide better value than the commodities they extract.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Commodity prices are facing a shift. As inflation heats up and growth stabilizes, the commodity arena is gradually tilting in favor of growth-oriented commodities such as Oil and Copper. Meanwhile, commodities associated with inflation protection, e.g., Gold and Silver, are not only losing their allure but facing growing sell pressure as well.