With the recent decline in the price of oil, many investors are wondering, where the opportunity is to make money from the decline? As I have stated before, my investing motto is always to keep it simple; which in this case would mean "simply buy oil stocks."

Over the past few months, the price of oil has unexpectedly fallen from over $100 a barrel to the $50 range. Neither economist, market analysts, or oil industry experts saw this decline coming. So I believe it is safe to say that no one, certainly including myself, knows were the price of oil is going in the near future. But with that being said, I think most would agree the use of oil is not going away in the near future. Oil is and will be the most widely used form of energy in the coming years, despite the rise of natural gas, solar or any other form of energy which currently exists.

The fall in the price of oil has caused oil stocks to decline. For example, Exxon Mobile (XOM) is down more than 8% over the past six months while Chevron (CVX) is off by nearly 14%. Smaller players like Anadarko Petroleum (APC) is off by nearly 22% and Pioneer Natural Resources (PXD) is off by 32% as the price of oil has fallen during the second half of the year. These types of declines have been felt throughout the industry.

One of the first and most common antidotes we are taught as investors is "buy low, sell high." When stocks fall, their price is low or at least lower than it was, which means if you believe in the company, or in this case the industry, then now is the time to buy. Continue reading "Falling Oil Prices Presents Opportunity"→

In theory, the price of any stock represents the present value of future cash flows. When those cash flows (i.e. earnings per share) are undergoing a contraction, the share price should theoretically decline. Occasionally, a share price will fail to reflect a future rebound in earnings growth that's expected to occur. In such a scenario, the intelligent investor takes notice. He knows that if projections are indicating a future rebound in earnings, then he can expect a future rebound in the stock price as well. He's aware that, in this instance, the further the share price declines today, the larger the percentage gain investors will see tomorrow. Thus, the stock is an obvious buying opportunity.

Let us turn our attention to Manitex International, Inc. (NASDAQ: MNTX), a provider of engineered lifting solutions. The company is currently valued at a market cap just north of $150M. Like many fast-growing small cap stocks, MNTX has seen plenty of volatility in both its earnings and share price.

With full-year EPS expected to contract by 17.5% YOY (from $0.80/sh to $0.66/sh), the stock is trading roughly 38% below its 52-week high. Furthermore, its P/E ratio of 15.6 is in the lower echelon of its long-term range, which would seem to imply a further earnings contraction to occur beyond 2014. Continue reading "Manitex (NASDAQ:MNTX) Looks Primed For Excess Returns"→

This week was undoubtedly a busy week for FX traders, with the utter meltdown of the Russian Ruble followed by Putin’s speech, the across-the-board selloff in emerging markets and the surprise negative rate announced by the Swiss National Bank. What this week won’t be remembered for is a Pound Sterling turnaround, yet I intend to illustrate in this article that that might just be in the cards.

Across the Channel

The fact that the Pound Sterling has shed value against the almighty Dollar might not come as a surprise; after all, the Dollar has rallied across the board as the Fed turned hawkish and the economy accelerated. But what is a surprise is why the Pound Sterling, the currency of an economy which has grown at an annual pace of 3%, has been essentially flat versus its European peer, the Euro? In short, after a robust performance from the UK economy, investors are beginning to get the sense that rather than continue accelerating the UK is been dragged down by the woes across the Channel with Europe pulling UK growth potential down. Below, the two major charts that made investors ponder and Sterling stagger.

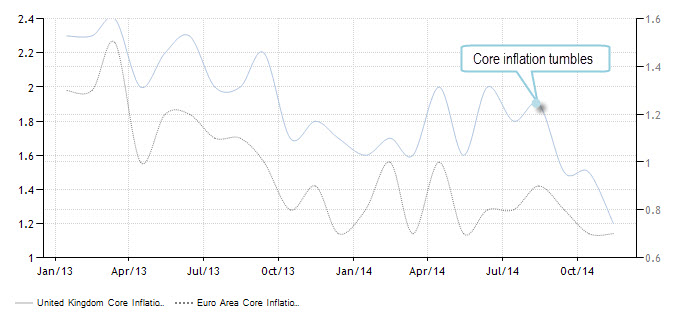

Core Inflation Tumbles

The first and foremost piece of data is inflation, but not just headline inflation which is also affected by external factors such as Oil prices (which, as we all know, happen to be collapsing) but core inflation that isolates external volatile factors including energy and food. As you can see in blue, UK Core Inflation just took a nose dive, hitting 1.2%, just 0.5% above the Eurozone’s 0.7% core inflation rate. With such a collapse in inflation expectations investors are beginning to question the UK recovery, wondering instead if growth is about to slow rather than accelerate, or perhaps that wage growth is not just around the corner as the pundits have said, and that maybe the Eurozone’s own stagnant growth is dragging the UK down along with it.

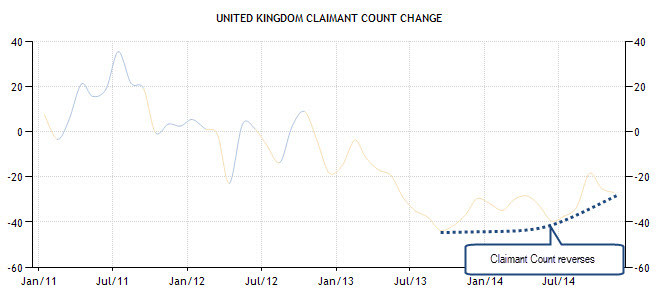

Thereafter, comes job market data; although unemployment has fallen to 6% it’s stubbornly fixed at this level and the claimant count rate, which measures the fall in unemployed (as seen in our second chart) has slowed down in pace. That had led investors to ponder that perhaps the job market is about to reverse some of its earlier job gains and that unemployment could nudge a bit higher.

Claimant Court Reverses

This has all led to one very basic question; are rate hikes in the UK really on the table next year? What with inflation in a nose dive, wages failing to rise and unemployment perhaps on the verge of a hike? Certainly, the possibility of a rate hike being pushed back into 2016 seems, especially after those readings, more probable. And that pretty much explains the flat performance of Sterling even against a battered Euro.

Retail Sales Changes the Game?

So what is the game changer? We have established the reason(s) why Sterling has been stagnant thus far but what makes investors think the game has changed? In two words: retail sales. The robust retail sales figure coming out of the UK on Thursday, a 6.4% (YOY) gain, surprised even the most optimistic investors. That unexpectedly positive figure has resulted in yet another possible scenario for Sterling watchers; say, the one in which the recent mild UK data was just a temporary bump or a minor glitch, and that the UK is actually gearing up towards another fall in unemployment, a rise in wages and maybe even a rate rise in 2015.

Matching Technicals and Fundamentals

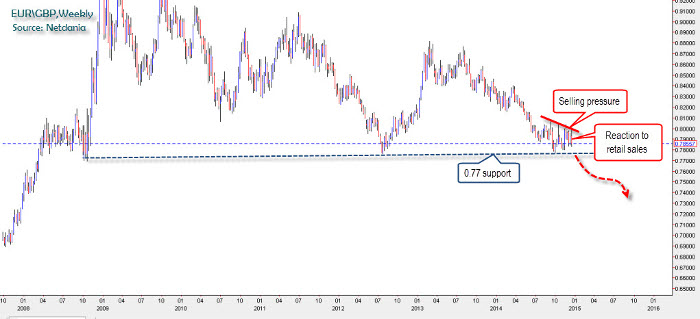

As seen in the chart below the reaction in the market was not too late to arrive and the EUR/GBP quickly took a nose dive amid renewed Sterling bets. This could very well be the start of another push south for the pair, especially considering the formidable resistance the pair has generated and how this resistance pattern was reinforced today. But, and although this could be the signal for the start of another bearish push in the pair, more needs to happen. Next week’s final Q3 GDP reading may very well provide that fuel, that impetus, which can push the pair below the 0.777 level. However, most investors are eying December’s CPI data and 4th quarter GDP which is due out next month. Because if those two readings follow suit after the robust retail sales numbers, the 0.777 support could be broken, and as the chart illustrates below, the next support for the pair may be quite distant, creating a potentially long bearish cycle for the pair and taking the Sterling bullish bet back into the game. So, if you are in it for the long haul, be patient; Sterling just may surprise you for the better.

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

For good and bad, Wall Street is constantly finding new ways for investors to attempt to grow their money. But, with all these products available for investors to choose from and a massive amount of information being presented to the average investor, it is easy to understand why so many investors still ignore ETFs and stick with mutual funds.

In most cases the average investor does not have a choice between a mutual fund and ETFs when it comes to their 401(K) plans through their employer. But for those investors who decide they want to put more money to work than just their 401(K) contributions, plowing more money into mutual funds is a bad idea for three reasons: truly knowing what your buying, performance, and cost.

Knowing What You Actually Own

Walk into any retail store in the US and pick up a any product; find the tag if it's a piece of clothing, the label if it's a drug or grocery item, or even the new Christmas toy you purchased, and you can find out exactly what was used to make that product. Depending on what the product is, there are different laws that have been put in place to protect the consumer which require the manufacturer to inform the customer of exactly what they are getting at all times.

Flip to the world of finance, unfortunately knowing what you are buying at all times is not always the case. While mutual funds are required to disclose their holdings to the public, these disclosures don't typically happen more than on a quarterly or semiannual basis. So what that means is that although you think you have purchased a large-cap growth mutual fund and that the manager must have at least 90% of the fund's assets in large-cap growth stocks, you essentially have no way of finding out if that's really were your money is invested. All the mutual fund manager needs to do is sell whatever doesn't meet the large-cap growth requirement the day before the fund's disclosure statement is put together and to investors it looks like the manager is doing exactly what he is supposed to be doing.

Remember that classic episode from the very first season of Seinfeld, when Jerry wants to "break up" with his obnoxious friend, Joel Horneck, but just can't bring himself to do it? Jerry can't stand the guy, but the thought of actually telling Joel he doesn't want to see him anymore is just so painful that even after he gets up enough nerve and delivers the blow over lunch at the diner – after which Joel, not unexpectedly, starts to blubber and carry on in public – Jerry immediately backs off and apologizes, further prolonging his agony.

I thought of that episode (I usually think in terms of old sitcom episodes, much to my wife's annoyance) after I read the Federal Reserve's policy statement on Wednesday. It once again chose to kick the can down the road (I really hate that metaphor, but it does apply here) and put off raising interest rates until sometime into the unknown future. Apparently the Fed just can't bear the thought of having the financial markets pull a Joel Horneck on it.

Not only did the Fed not remove the "considerable time" language from its statement, as many market participants were expecting. Instead, it added a brand new noncommittal phrase, saying that "it can be patient" before it begins to "normalize the stance of monetary policy," i.e., raise interest rates from its current zero to 0.25% target range.

Of course, both being "patient" and "considerable time" can mean anything, or nothing, at all. What they absolutely don't mean is "right now" or "very soon." At her news conference following the statement, Fed Chair Janet Yellen said a rate increase won't take place for "at least the next couple of meetings," meaning well into next year, and maybe not even then. Who knows?

Perhaps Mrs. Yellen and the six of her colleagues on the Federal Open Market Committee who voted for the statement (there were an unusually high three members who didn't go along) thought they were being cute in adding another set of evasive, ambiguous words that show that it still can't make up its collective mind.

Is the Fed simply indecisive? Incompetent? Or simply afraid of what the market reaction might be if it stops prolonging a policy that is no longer necessary? Continue reading "Joel Horneck And Fed Policy"→

You are now leaving a Magnifi Communities’ website and are going to a website

that is not operated by Magnifi Communities. This website is operated by Magnifi

LLC, an SEC registered investment adviser affiliated with Magnifi Communities.

Magnifi Communities does not endorse this website, its sponsor, or any of the

policies, activities, products, or services offered on the site. We are not

responsible for the content or availability of linked site.