Overview

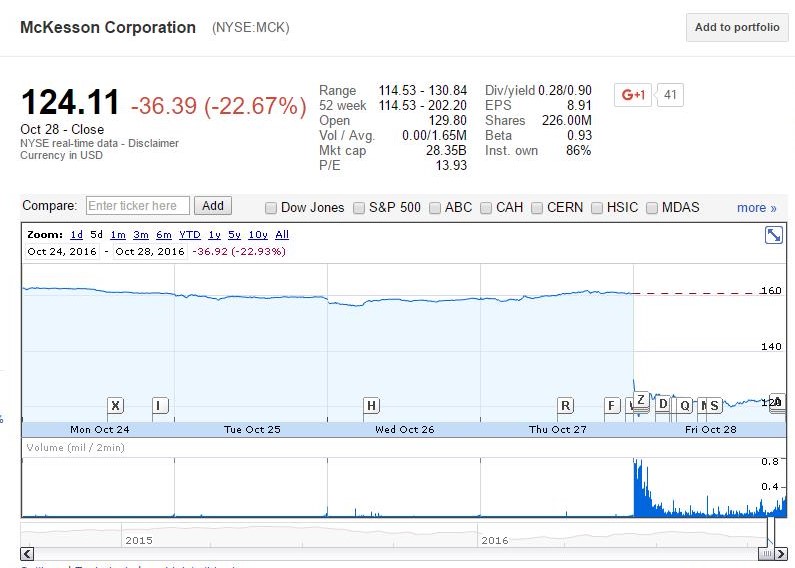

McKesson Corporation (NYSE:MCK) recently reported Q2 2017 numbers that missed analysts’ expectations on both EPS and revenue, missing by $0.11 per share and $1.25 billion, respectively. This was the fourth consecutive quarter in which McKesson has missed revenue targets. As a result of the most recent miss, shares of McKesson sank by ~$40 per share or 23% beginning in after-hours trading and through the next trading day (Figure 1). In February I wrote a piece on McKesson stating that I felt McKesson presented a buying opportunity when the stock sank to a 52-week low of $148 per share. As that call began to come to fruition, I wrote a series of follow-up articles voicing caution as the share price appreciated. On March 21st I framed my thesis as being well intact as the shares appreciated to the mid $150s. On May 29th I stated that concerns remained despite the solid Q4 2016 quarterly earnings as shares appreciated to the low $180s. On July 20th I stated that shares had appreciated 34% by reaching the ~$200 level and at that point, I was hesitant due to pressures regarding the pharmaceutical supply chain and earnings from other pharmaceutical wholesalers such as Cardinal Health. At the writing of the July 20th article, I had relinquished my position in McKesson due to the run-up in share price and the growing concerns of the business model in combination with social and political pressures.

Figure 1 – McKesson’s free fall after missing Q2 2017 earnings and lowering guidance

Continue reading "McKesson Craters - Misses Q2 2017 Estimates and Lowers Guidance"