Last week, the jobs report was released. Economists were expecting an additional 258,000 new jobs added last month. The Labor Department’s report revealed that the U.S. economy has had robust job growth last month adding over 500,000 jobs in July.

The exceedingly strong numbers of the report diminished concerns about the United States entering a recession. While this optimistic report bodes well for economic growth, it certainly does not address inflation.

However, it does change market sentiment which had been intensely focused on the last two GDP reports. On July 28 the government released the advance estimate of the second quarter GDP. The report revealed that the GDP had decreased at an annual rate of 0.9% during the second quarter of 2022.

Although trading last week was limited to four trading days due to a holiday weekend gold had a deep and severe price decline.

Gold lost approximately $74 in trading this week opening at approximately $1814 on Tuesday and settling at $1741 Wednesday. Last week’s price decline resulted in gold devaluing by 4%.

The Friday before last, gold opened above and closed below a support trendline that was created from two higher lows. The first low occurs at $1679 the intraday low of the flash crash that occurred in mid-August 2021. The second low used for this trendline occurred in the middle of May when gold bottomed at $1787.

Gold closed just below that trendline one week ago, however it was Tuesday's exceedingly strong price decline of $50 that accounted for two-thirds of last week’s price decline and resulted in major technical chart damage.

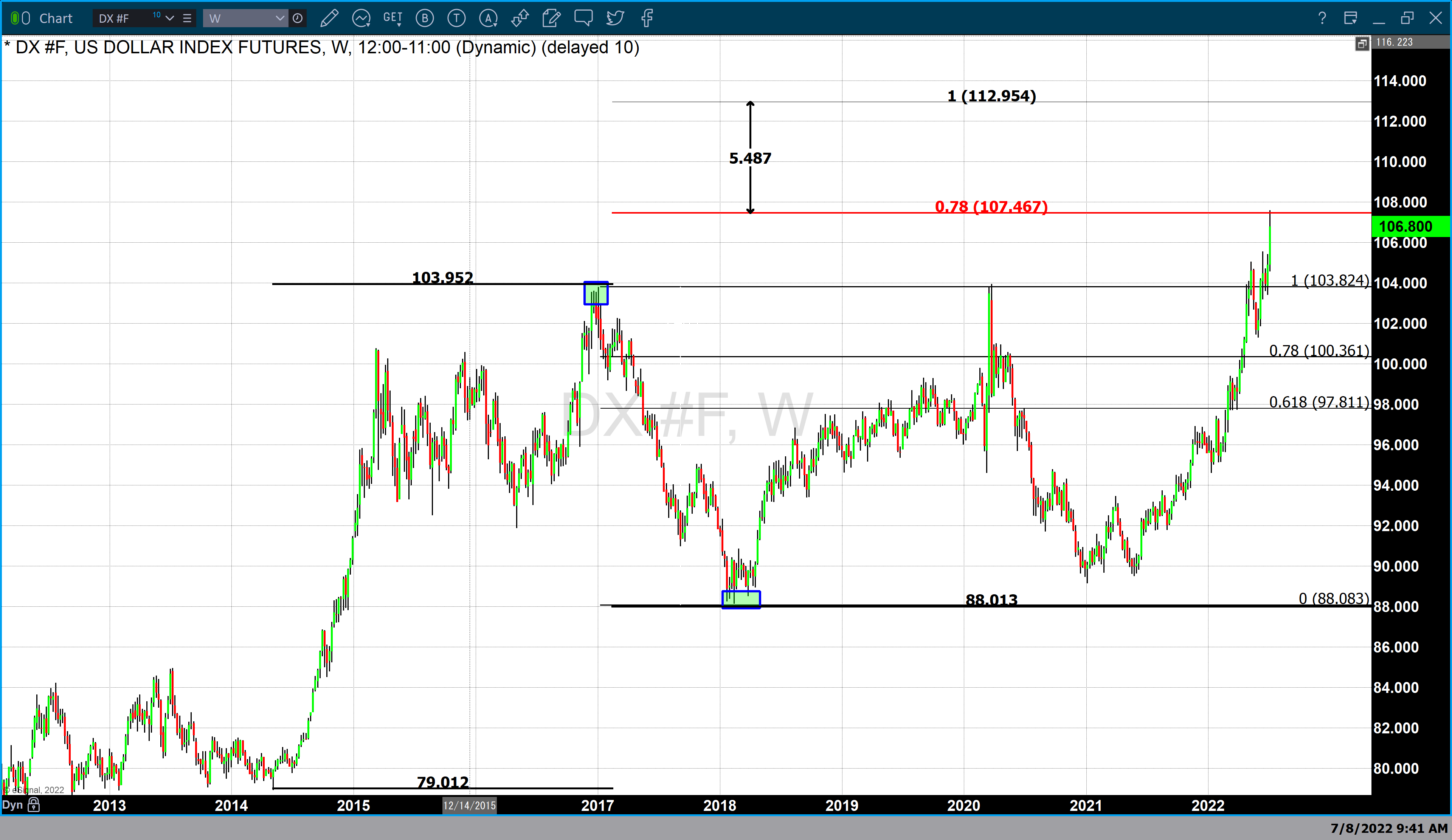

The primary force that moved gold substantially lower last week was dollar strength. The dollar index gained well over 2% last week accounting for over half of the price decline in gold.

Dollar strength was a result of traders and investors focusing on recent and future interest rate hikes by the Federal Reserve. Since March the Federal Reserve has raised rates on three occasions with each rate hike having a higher percentage increase than the last. The Fed raised rates by 25 basis points in March, 50 basis points in May, and 75 basis points in June.

Friday’s jobs report was forecasted to show that 250,000 jobs were added to payrolls last month. The actual numbers came in well above expectations with 327,000 jobs added last month. The unemployment level remained at 3.6%.

The fact that the actual jobs report came in above expectations strengthened the hand of the Federal Reserve to continue to raise interest rates substantially this month.

It is highly anticipated that the Federal Reserve will enact another 75-point rate hike at the July FOMC meeting. Before the Federal Reserve raised interest rates in March the fed funds rate was just ¼% or 25 basis points.

Currently, the interest rate set by the Federal Reserve is at 1 ½ % to 1 ¾. This would take the interest level set by the Federal Reserve to 2 ¼% to 2 ½%.

According to the CME’s FedWatch tool, there is a 93% probability that the Federal Reserve will raise rates once again by 75 basis points this month.

However, there are three more times that members of the Federal Reserve will convene for an open market committee meeting which leaves the door open for additional rate hikes. Because the Federal Reserve is data-dependent the number and size of the rate hikes will be based upon whether or not there is a substantial decrease in inflationary pressures.

That being said, it is most likely that this week’s CPI report will not have a dramatic impact on the Federal Reserve’s decision to raise rates as Chairman Powell and other Fed members have stated that the Federal Reserve will aggressively raise rates at the July FOMC meeting.

For those who would like more information simply use this link.

Wishing you, as always good trading,

Gary S. Wagner The Gold Forecast

Chairman Powell’s testimony before Congress this week painted a dire economic outlook which will include the continued contraction of the national GDP coupled with continued interest rate hikes.

During his testimony, it was evident that there was a subtle difference in his word track that was uncharacteristic and a dramatic change from his usual refined method.

The chairman made it clear that the Federal Reserve has one goal in mind above all others and that is to reduce the level of inflation. They emphatically stated that the actions of the Federal Reserve will most likely lead to a recession rather than a soft landing.

Yahoo finance captured his overall demeanor in a most articulate manner saying, “He said a recession caused by the Fed’s own monetary tightening remains a “possibility.”

A soft landing, with higher rates but a still-healthy economy, would be “very challenging” to achieve. And Powell said the Fed’s fight against inflation was “unconditional,” meaning nothing will stand in its way.”

The revisions by the Federal Reserve to their monetary policy most certainly would contract the economy and bring on a recession.

A recession is defined as “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.”

The last GDP report revealed that the United States had an economic expansion leading to a 6.9% growth in the GDP for Q4 of 2021. If advanced estimates for the GDP Q1 are correct it will indicate a decrease in the real gross domestic product (GDP) for the first quarter of this year.

The last occurrence of a contracting GDP quarter to quarter occurred during Q2 of 2020. However, the following quarter (Q3 2020) revealed a robust increase in national GDP.

This is why next week’s report is so critical. On Wednesday, June 29 the BEA (Bureau of Economic Analysis) will release the U.S. GDP first-quarter report.

According to the advanced estimate released on April 28, “Real gross domestic product (GDP) decreased at an annual rate of 1.5 percent in the first quarter of 2022, according to the "second" estimate released by the Bureau of Economic Analysis. In the fourth quarter, real GDP increased 6.9 percent.”

Currently, there is a high probability that the actions of the Federal Reserve will lead to a recession. The question is not whether or not the United States will enter recession but rather when the recession will begin and how long the recession will last.

While a recession can stabilize gold pricing, and higher inflation certainly creates a bullish undertone for the precious yellow metal, rising interest rates have become a primary focus on the future price of gold and has pressured pricing lower since March of this year.

Gold has declined just over 12% from the highs of $2070 in March to gold’s current pricing of $1828. While it seems as though there is strong support for gold at $1800 depending on how aggressive the Federal Reserve becomes in regard to further rate hikes.

Besides the GDP report due out on Wednesday, on Thursday the government will release its latest core inflationary numbers when the U.S. PCE price index report is published.

For those who would like more information simply use this link.

Wishing you, as always good trading,

Gary S. Wagner The Gold Forecast

You are now leaving a Magnifi Communities’ website and are going to a website

that is not operated by Magnifi Communities. This website is operated by Magnifi

LLC, an SEC registered investment adviser affiliated with Magnifi Communities.

Magnifi Communities does not endorse this website, its sponsor, or any of the

policies, activities, products, or services offered on the site. We are not

responsible for the content or availability of linked site.