For the investors who are watching the Euro, its latest behavior might appear bewildering. After all, the ECB, slightly undershooting expectations, still increased its target asset purchases to roughly €1.5tn. At the same time, the ECB cut the deposit rate to -0.3%. And let's not forget the goings on over on the other side of the Atlantic. There, the Federal Reserve is gearing towards its first rate hike in almost a decade. What, then, could possibly incentivize investors to buy Euros? And can it last?

Draghi's Words Hit a Nerve

When investors expect more central bank easing, they also expect the obligatory rhetoric. But what they hate is when the rhetoric is of a very specific sort. In this case, it is when a central banker stresses the limitations of monetary stimulus. Yet, in practically the same breath, they drive home the need for more government input. And essentially, that is exactly what Mario Draghi said.

Now, when the Fed unleashed similar rhetoric, it was seen as a signal that its ammunition might be running out. Earlier this year, the BoJ had made a similar statement in an attempt to lower expectations of more stimulus.

Given that, if Draghi is using that kind of "excuse," what can we presume? Perhaps that Super Mario is actually preparing us for less stimulus? Certainly that makes one think. And the fact that Mario Draghi was rather moderate in adding more stimulus tends to fuel speculation.

Now, what do investors do when they are "underwhelmed" by the stimulus? They liquidate positions first and ask question later. And so the EUR/USD bounces back to 1.09 from its lows.

What Drove Draghi to Undershoot?

So what drove Draghi to backpedal on the buildup he created coming into the December meeting? Though he didn't say it outright, it might just be the same reason the other central banks chose. That is to sit back, wait, and see how it all plays out.

Because that is exactly what Draghi wants—to wait and see. Draghi might presume that a Fed rate hike is coming this week and that that might weaken the Euro. If so, that could stimulate the Eurozone economy a bit. If that's the case then why not save his weapons for later?

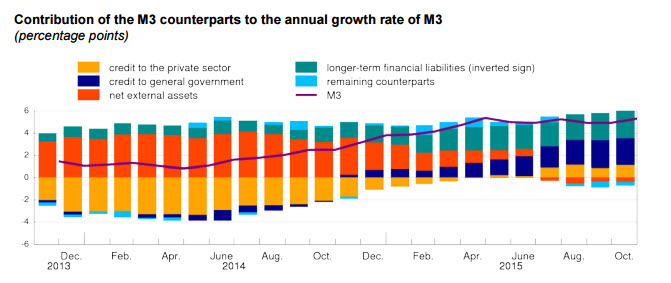

The second reason, perhaps, is rooted in the chart below as prepared by the ECB. The chart illustrates the growth in money flows in the Eurozone (M3). As can be seen, the drag to M3 Money Supply from a shrinking credit market has eased. In other words, the Eurozone credit market is no longer contracting. And that means deflationary pressures might ease as well. Which, of course, just might validate Draghi’s wait-and-see approach.

Chart courtesy of The ECB

Draghi will have to deliver

In the end, however, Draghi will still need to unleash another QE bazooka. Because, despite all else, there's a big difference between loans that stop shrinking and loans that grow robustly. And, of course, under such a case, Eurozone inflation is likely to stay muted. And since inflation will be well below the ECB's 2% target Draghi will be compelled to act.

Euro Strength Transitory

It is quite the paradox but the longer Draghi waits with additional stimulus, the longer the Euro will be lower. The Eurozone needs a Euro that is lower than $1 to recover and boost its exports and inflation Otherwise the economy will just barely muddle through.

Don't be fooled by appearances, the Euro, despite its plunge of 25% since May last year, is still overvalued and weighs on regional growth. And since that is the case, the latest Euro strength then is nothing more than a pause before the fall. In other words, the Euro's appreciation is transitory in nature. Short sellers of the EUR/USD might soon come down from the fence and pile on for another short. But, this time, it could be all the way to parity.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

I wonder how someone can call the Euro overvalued. A friend of mine just came from Berlin to Florida and was flabbergasted how expensive everything is. He had been living in FL for years and own property here. So his opinion is not that of an occasional visitor. I receive pension from the Eurozone and it hurts how my income is shrinking every month. I guess I have to book another cruise in Europe because during my last cruises the Euro was up when I took my trips.

There might be another reason for the jump in the Euro....I was in France when the US invaded Iraq in the first gulf war...that is when, overnight, the Euro went from $ .85, to $1.40....basically because NO ONE liked the fact that the US made a unilateral attack when we were not attacked. We are seen as the "new Nazis" by a large segment of the world as a result of our wars in the Middle East.

It might be that the recent Climate Conference had much more coverage world wide than it did here, and that Europeans take the issue of climate change seriously. I wasn't our finest hour, because we, as the world's pollution leader for the past century, still don't have to actually do much to hasten the demise of fossil fuels. The media in Paris has made widely known, the fact that our Congress intends to rollback the executive orders that have been the only means to proceed in the struggle to reduce atmospheric pollution. There are a lot of people that will feel less likely to buy American if they are pushing their governments to take climate action, while we roll back. Obama sounds like a hypocrite, when he speaks about "freedom" while imposing our military on most of the world, and more so for telling the Paris Conference on Climate that everyone must share the cost of our pollution,