I suppose my 2016 outlook for MLPs and pipelines should begin with a mea culpa about something I wrote earlier in 2015. On September 24th, I wrote:

“I generally regard pipelines as being a historically defensive area of the stock market, comprised of relatively steady, fee-for-service businesses. (Pipeline companies’ stocks) may be receiving undue punishment in the midst of the oil crash of the past 15 months. (Their) prices are down about 16% since June 20, 2014, compared to nearly a 38% decline for the overall energy sector, and a 63% crash in oil prices.”

The First Trust North American Energy Infrastructure ETF (EMLP) closed at $22.17 that day; and while EMLP did rise to nearly $24 over the next couple weeks, it then plateaued in October and plunged below $20 again by December 4th. It closed Tuesday at $20.15.

I regret having used adjectives like “defensive” or “steady” to describe these stocks. The past 7 or 8 months have certainly demonstrated otherwise!

The jury is still out on whether these stocks are “receiving undue punishment,” though. Perhaps 2016 will provide the verdict on that.

Pipelines’ Historical Performance

The Tortoise North American Pipeline Index (TNAP) boasted annualized total returns of about 15% from January 1, 2000, through June 30, 2014, according to my own calculation from TNAP index data on Tortoise’s website, accessed on 12/29/15.

Since June 30, 2014, though, the TNAP index has given back about 35% of its value – most of which has been shaved off since about April 30, 2015. The index actually held up very well for the first 10 months of this oil & gas crash, before expectations of falling production (and therefore, demand for transportation) finally began catching up with MLPs and pipelines in the 2nd quarter. The ensuing months have been brutal.

Note: Of course, you can’t invest directly in an index like the TNAP; however, Tortoise now has an ETF designed to track the TNAP index (less an expense ratio of about 0.70% per year). I covered both Tortoise’s ETF (TPYP) and EMLP in the aforementioned September 24th article. In addition, I covered some other MLP ETFs – including my reasons for preferring TPYP and EMLP – on September 2nd.

Can Pipelines Ever Return To Their Prior Glory?

I don’t believe MLPs or pipelines necessarily owe investors a 15% return, such as they delivered for the first 14 ½ years of this century. Nor do I believe total returns in excess of 8-10% are likely in the future, on any type of consistent basis. The dividend yields can be nice, but to me, dividends are no guarantee of an attractive total return.

Whether pipelines can, at least, stabilize in 2016, though, and resume delivering competitive returns once again, obviously depends a lot on oil and gas prices and production. Here are some thoughts on that (as if there were a shortage of commentary about the future of oil and gas prices). Company-specific factors will also play into pipelines’ 2016 performance, as will (I expect) merger and acquisition activity. And finally, pipelines stocks’ performance in 2016 may be influenced by some correlation to the broader energy sector and the overall stock market.

Not All Pipeline Stocks Are Created Equal

The 4th quarter has shown a wide divergence in stock performance in the midstream category (pipelines, transportation, and storage). Even since December 14th, some midstream stocks have mounted a furious rally while the year’s worst performers continue to wallow in the sludge, seemingly.

Enterprise Product Partners (EPD) and Magellan Midstream Partners (MMP) have shot higher lately, to the tune of nearly 14% in just 10 trading days. TransCanada (TRP) is holding up well, and others like Williams (WPZ) and Plains All-American Pipeline (PAA) have seen dramatic (dead-cat?) bounces off their lows.

Yet, other well-respected firms like Kinder Morgan (KMI) and Energy Transfer Equity (ETE), have fallen badly behind. KMI is down 7.5% during the same 10-day period. ETE is essentially flat. Both stocks have had extremely rough years, too – down 66% and 54% respectively, through Dec. 29th. By comparison, MMP is down only about 20% YTD, and EPD and TRP have each shed about 31-33%. Most of KMI’s and ETE’s divergence has happened since Oct. 8th/9th.

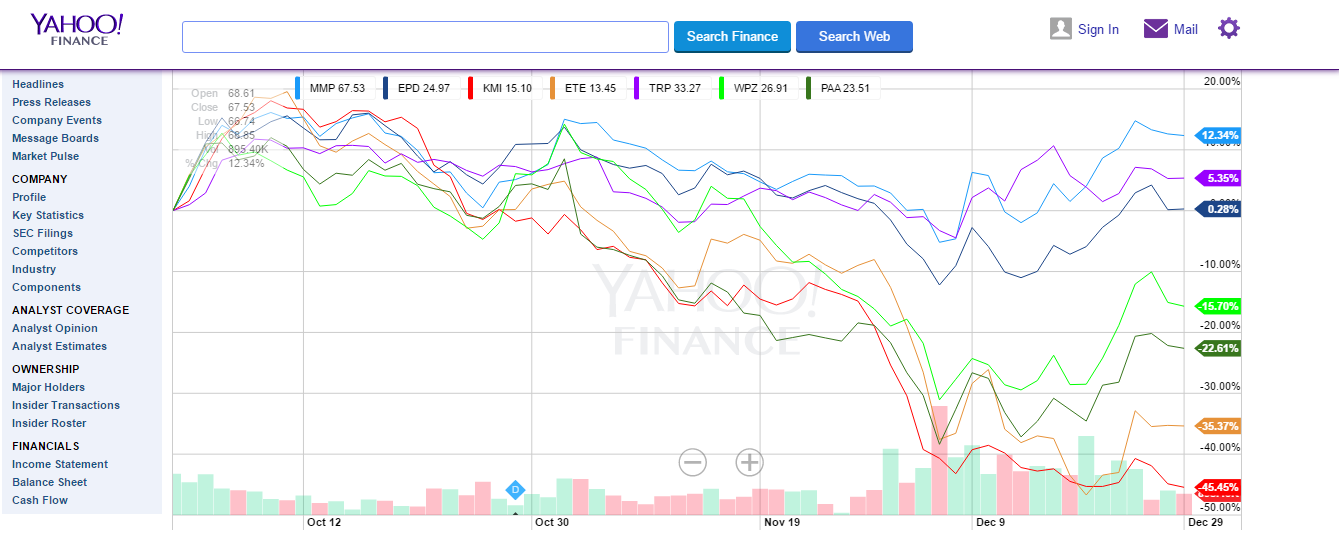

This graph of the last 3 months shows KMI and ETE (red and orange lines, on the bottom) have been clobbered and continue to languish. Meanwhile, MMP, EPD, and even TRP (blues and purples) have held up quite well.

Chart courtesy of Yahoo Finance

I won’t have time or space to evaluate all these stocks here in this article. Let’s take a closer look at MMP and EPD compared to KMI. Have MMP and EPD put in their lows? When will KMI finally begin to recover?

First, some quick key terms:

Distributable Cash Flow

“Distributable cash flow” is a big deal in the pipeline business. These companies own assets that generate cash flow, and that’s where dividends come from, boys and girls.

Another widely followed measure of a midstream company’s health is the “distribution coverage ratio,” which describes how much revenue the company is raking in, in relation to dividends being paid out. MMP and EPD both have very robust 1.3x coverage of their distributions. In fact, MMP has stated its 1.3x coverage ratio is fine for now, but the company ultimately feels comfortable moving toward 1.1x… implying MMP not only intends to maintain, but also to continue regularly increasing its dividend. The market has to like the sounds of that!

Those 1.1 – 1.3x distribution coverage figures are very popular among midstream investors today. Companies with cash can continue funding any projects and/or acquisitions with minimal need to raise capital from the stock or bond markets – an iffy proposition for any energy company these days.

KMI has gone to equity and debt markets repeatedly to fund projects while maintaining minimal coverage of its dividend… until the company announced a 75% dividend cut in early December. Much more on KMI in the next section.

Meanwhile, ETE, like KMI, has kept its distribution coverage around 1.0x, and has also gone to equity markets and taken taking on more debt in order to raise capital. ETE and will take on, even more, debt in connection with its cash purchase of Williams.

Kinder Morgan (KMI): Among The Biggest Losers Of 2015

The biggest recent news about KMI is still its 75% dividend cut. The announcement came on the heels of a 7-day, 34% drop in KMI’s stock price. But how bad are the implications really? Here’s my feeling on it:

Notwithstanding the market’s immediate reaction, the cut gives KMI important flexibility to retain more of its cash internally in order to weather the storm – and possibly even grow through projects and acquisitions. Interestingly, the dividend cut arguably wouldn’t have been possible without KMI’s 2014 move to restructure as a corporation instead of an MLP (since MLPs are required to distribute most of their earnings to shareholders).

Before the rate-cut announcement, KMI came out with a statement to the effect that its distributable cash flow would be sufficient to maintain and even increase dividends in 2016; but that management “alternatively” would consider using some or all that cash flow “to fund some or all of Kinder Morgan’s equity needs.” When KMI later chose the dividend reduction, CEO Steve Kean explained, “Today's decision is about finding the most economic way to fund our set of attractive return expansion projects."

Tom Gardner of the Motley Fool wrote in a recommendation for subscribers December 18th:

“By choosing to retain these cash earnings and use them on the business, Kinder Morgan can continue investing in high-return projects during a period where new stock and bond issuance (the industry's traditional method of financing) is at a standstill.”

Essentially, KMI’s dividend cut should help earnings. So it’s a tradeoff. Because KMI wants to fund expansion projects that are projected to be immediately accretive to cash flow and earnings, management has the option to either raise capital through the stock or bond markets or to simply retain capital that would have otherwise gone to shareholders in the form of dividends. Right now, cutting the dividend is the firm’s least expensive way to pursue these projects that should boost future earnings and cash flow.

In contrast, an MLP in need of cash wouldn’t have the option to decrease dividends. An MLP, instead, would be forced to either scrap the new projects or go to the markets for capital at a highly inopportune time. Either way would impact future earnings, cash flow, and even the MLP’s future distributions (by extension). So again, KMI’s non-MLP status gives it the flexibility to cut the dividend now rather than see it erode in the future.

Gardner also noted KMI is trading for basically its book value, compared to a 2.77 average multiple over the last 3 years. This despite the fact KMI owns the nation’s network of largest natural gas pipelines and continues to expand its reach. By the way, the dividend ain’t what it used to be, but still gives KMI shareholders a 3.3% projected yield based on Dec. 30th closing price of $15.10 per share.

Still nervous about KMI’s dividend cut? Try looking at it this way: Maybe a business should return dividends to shareholders only if management sees no better opportunities to use those dollars for growth itself. Quoting from Gardner again:

“The board could very well have decided that the dividend was too important, but it went for value creation instead. To not do this, as Kinder said recently, ‘would be giving up some very important, very profitable long-term projects.’"

I wouldn’t sweat KMI’s dividend cut too much. I’d actually rather see management use that cash rather than go to equity or credit markets for the capital it needs to wrap up its current projects. And since the projects will be immediately accretive to earnings, it seems worthwhile to use cash to finish them. Besides, it looks to me like the market is already in the very painful process of discounting the news. In fact, markets often over-correct in times like these. Add KMI to your watchlist so you can check the MarketClub Trade Triangles for signs of a reversal at some point. Be patient, though. This one’s still a powder keg until things settle down.

Enterprise (EPD) and Magellan (MMP)

In contrast to KMI, EPD and MMP have taken off since December 14. The market doesn’t expect a dividend cut from either of these 2 mainstays, and neither do I.

Many midstream stocks can now dangle a higher yield than EPD and MMP; but my conviction is that investors should select stocks based more on the underlying business and the quality of management, rather than whatever the dividend happens to be at the moment. Don’t get me wrong; I love a solid dividend, particularly when management is committed to it (and better yet, when they’re committed to regularly increasing it). But dividends are only one part of the return, and when a stock drops 60%, its dividend doesn’t matter very much.

EPD’s and MMP’s management teams have shown skill in navigating cycles while maintaining solid dividend coverage.

I’d argue KMI’s management this month demonstrated wisdom, too, but in a completely different way. KMI’s cash and coverage levels were too high compared to its debt and other obligations. KMI, to their credit, made the decision to finance the company’s remaining projects using cash that would have otherwise been paid out in dividends, rather than going to markets at an inopportune time. They’re paying the price in the short term, but living to fight another day.

One has to admire EPD’s and MMP’s slow, steady, measured approach to maintaining higher cash levels than other pipeline companies and going to markets less frequently as well. The companies are highly confident in their dividend coverage, as well as their own prospects for continued financial success.

Motley Fool analyst Tyler Crowe recently wrote:

“Back in 2013, or even 2014, a lot of investors might have questioned Enterprise's decision to keep a more conservative payout policy. After all, debt was cheap, and equity prices were very strong, which suggested the company could return more cash to its investors while still having plenty of financing options to fund growth.

“At the same time, many of Enterprise's peers were pushing more cash out the door to investors and growing their payouts at astounding rates. Instead of giving into that pressure, Enterprise kept a considerable amount of cash in house.”

EPD’s management recently said:

“We believe Enterprise is well positioned to manage, adapt and prosper through this cycle, as we did through the 2008 and 2009 cycle. Our business model has withstood a number of commodity price cycles, and we are confident in our ability to produce solid results while maintaining financial flexibility consistent with our BBB+, Baa1 investment-grade debt ratings, and we continue to provide healthy distribution coverage.”

This past month, pipeline companies have been severely punished for high dividend payouts (or in KMI’s case, a formerly high payout). The more conservative firms like EPD and MMP have been rewarded.

On another note, a Christmas Eve WSJ article reported that in early January, EPD will ship “the first freely traded cargo of U.S. crude oil to be shipped overseas” since the US banned oil exports in 1975. The 600,000 barrel sale will reportedly go to a refinery in Switzerland owned by Vitol Group, a Dutch oil trading firm. The announcement came less than 1 week after President Barack Obama signed the budget bill that lifted the ban.

Bottom line, I’d patiently wait for a reversal to green on EPD and MMP also (like KMI). My view is these are all quality companies to own in a diversified portfolio. EPD and MMP haven’t been beaten down as much as KMI, but there’s something to be said for their ability to outperform as well. And they may yet have been overly punished during this tumultuous time.

Best,

Adam Feik

INO.com Contributor - Energies

Disclosure: At the time of post publication, this contributor owns TPYP and EPD, but did not own any other stock mentioned. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

I guess these are still good holds

Very good indeed!