I’ve written many articles highlighting the advantages options trading and how this technique, when deployed in opportunistic or conservative scenarios may augment overall portfolio returns while mitigating risk in a meaningful manner. Options trading in layman’s terms can be described as a parallel to owning a rental property. One owns an asset that he is willing to leverage in the form of a tenant occupying his home for monthly rent. In the case of options trading, one owns shares and he is willing “leverage” these shares for “rent” or in the case of options, a premium. In this scenario, the owner of the home gives the tenant the option to buy the property or rent to own if he/she desires prior to a specified date. For the owner of the stock, he is providing the option to buy the underlying security at a specified price on or before a specified date. From the renter’s perspective, if the home value is increasing and the housing market is strong and on an uptrend, the renter would exercise this option and elect to buy the home. In the case of options trading, the renter of the stock would exercise the option to buy the shares if the shares rise significantly and lock in the lower, agreed-upon price. In the housing scenario, the renter elected to have the option to buy however didn’t have the obligation to purchase the home. The tenant witnessed home values increasing and decided to exercise the option to buy and capitalize on the rent he was already paying into the property. For the renter of the stock, the renter had the option to buy the underlying shares however he didn’t have the obligation to purchase these shares. The renter of the shares witnessed the stock take off and decided to exercise the option to buy and capitalize on the “rent” he had already paid into the option contract. As the owner of the property/stock, the ideal scenario is to own the property/stock and continuously collect rent/premiums on a monthly basis without relinquishing the property/stock. I will provide an overview of my empirical case study based on my options activity during Q2 2016 (Table 1). Here, I’ll provide details focusing on optimizing stock leverage via covered calls. Emphasizing the ability to sell these types of options in an opportunistic, aggressive and disciplined manner to generate liquidity while accentuating returns and mitigating risk via empirical data.

NOTE: I utilize options to extract additional value out of my long positions in addition to mitigating risk. I earmark a portion of my portfolio solely for options trading in more volatile stocks. The empirical example demonstrated here is part of my overall options strategy. There are numerous positions that I’ve written covered calls on in which my overall position realized a net loss, despite the options income. I do not want to misconstrue readers into the belief that options are trivial in any sense.

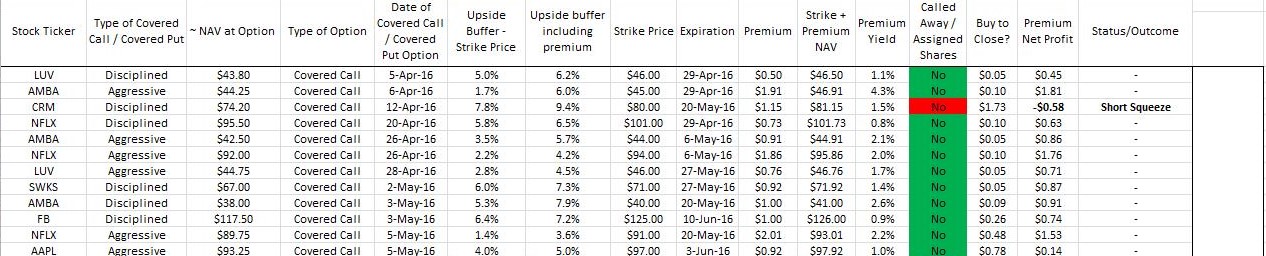

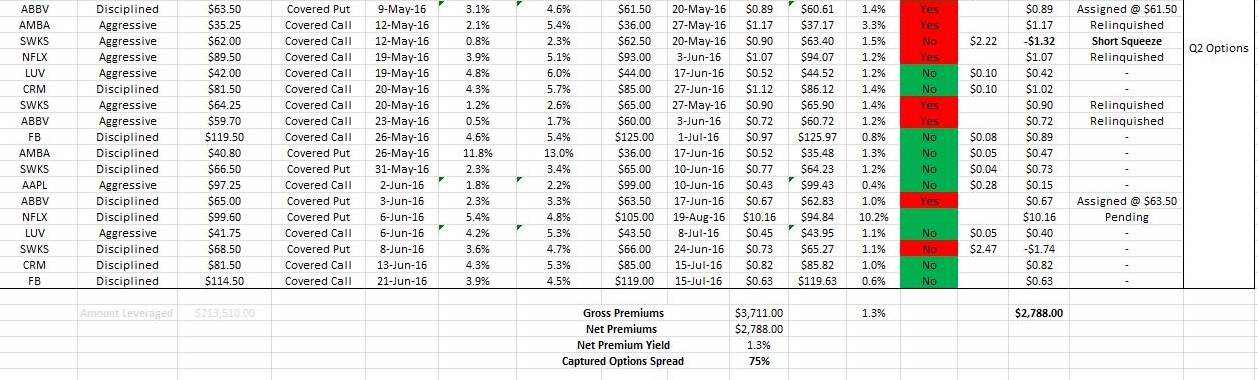

Table 1 – Summary of my options trading throughout Q1 and Q2 2016

Key Characteristics In Options Trading

1. Strike price: Price at which you can buy the stock (buyer of the call option) or the price at which you must sell your stock (seller of the call option).

2. Expiration date: Date on which the option expires

3. Premium: Price one pays when he/she buys an option and the price one receives when he/she sells an option.

4. Time premium: The further out the contact expires the greater the premium one will have to pay in order to secure a given strike price. The greater the volatility, the greater the time premium received for covered call writing.

5. Intrinsic value: The value of the underlying security on the open market, if the price moves above the strike price prior to expiration, the option will increase in lock-step.

My Classification And Types Of Options

1. Opportunistic: When a stock price increases dramatically based on earnings or an extraneous event in the range of 7%-15% in one day or over the course of a few days.

2. Aggressive: Writing a covered call at risk near the money in order to lock in a high yielding premium. Relinquishment of shares not an issue as the security of interest is not a long holding.

3. Disciplined: Writing far out of the money covered calls with a substantial upside buffer to mitigate risk of relinquishment and capture small spreads over long periods of time as this is an iterative process.

The upside strike buffer should be in the range of 7%-10% for one-month contracts while being cognizant of the stock price as it approaches expiration.

The Holy Grail Of Investing

If an investor makes the decision to purchase a stock for its long-term prospects, he can create the ideal scenario where he retains the shares, collects the “rent” or premium and the dividend payouts while renting his shares. Writing covered calls to leverage his position results in a scenario where at the expiration of the contract the strike price is not reached. This allows the investor to retain his shares, mitigate risk, increase the cash position in his portfolio and collect any dividends that are paid out. I will walk readers through a multi-tiered approach to leveraging different types of covered calls that I employ on a frequent basis to optimize my returns on long positions. If one is long a stock and has healthy unrealized gains, he may elect to write a covered call against his position to extract additional appreciation. Writing a covered call far enough out-of-the-money will likely lock in a cash premium on the front end with a low risk of relinquishing shares on the back end. Thus, the premium, shares, and any dividends are retained, and now the ability to write another covered call against this equity position is now available. This recalibrating of strike prices as the underlying equity appreciates enables traders to ride the uptrend on a bi-weekly or monthly basis. The idea here is to allow enough of an upside buffer that is built into the strike price relative to the stock price at the time the covered call is written depending on the scenario. This will likely result in a very low-risk scenario that shares will be relinquished at expiration while maintaining a long position. A soft upside buffer target that I focus on is 7%-10% for monthly contracts. Thus, shares have another 7%-10% to run over the course of roughly a month in order to reach the strike price and risk relinquishment. This soft rule of thumb can be scaled as needed based on time, volatility and recent price swings to the upside.

Layering In Covered Puts To Augment Covered Calls

Starting in Q2, I added another layer into my options strategy to augment my covered calls. I initiated a covered put or secured put strategy where I do not own any shares, however, I would be interested in owing shares if the price was lower in the future. In this case, I may like company X yet the share price isn’t appealing enough for me to commit to purchasing the shares. However, I’d be willing to purchase the shares at a lower price while someone pays me to do so. If shares of company X are currently trading at $50, I may elect to sell the put option to give someone who owns the shares the right to sell them to me at $48 while paying me ~$1.00 per share rendering my effective purchase price to $47 per share. For me, my goal is to leverage my cash and not be assigned the shares however I wouldn’t mind owning the shares if the option buyer exercises the option. In that case, I would buy the shares at the agreed upon price of $48 less the $1.00 per share that was already paid out to me from the premium payment. The premium is received due to taking on the risk of purchasing the shares at $48 since your potential loss is substantial. Theoretically, the price could go to zero, so the risk is great by definition. In my case, I look at stocks that have already come down significantly and sell the covered put in an effort to only collect the premium. My belief is that the shares won’t fall much further and in the event, they do I wouldn’t mind owning the shares while being paid to do so at a lower price than it currently stands (Figures 1 and 2).

Figure 1 – Panel one of my detailed Q2 options contracts

Figure 2 – Panel two of my detailed Q2 options contracts

Premiums Can Make A Meaningful Impact To Overall Returns

Based on my scenario above, extracting ~1% realized a gain on a monthly basis per equity holding via writing far out-of-the-money covered calls doesn’t seem like much on the surface, however, extrapolating out on an annualized basis may augment returns by 10%-15%.

The Short Squeeze

The major risk to this approach is attributable to any potential gains beyond the strike price. Put another way the call/put seller takes on the risk of relinquishing his shares/being assigned shares at an agreed upon price by an agreed upon date while receiving a premium to take on this risk of relinquishment/assignment. Thus, any price appreciation beyond the strike price will result in unrealized gains and relinquishment of shares at the strike price plus the premium received at the time of selling the call contact. In the put option scenario, this is ideal as only the cash was leveraged, and the premium was received without being assigned the shares. The option seller has the ability to buy-to-close at a higher price as the intrinsic value appreciates beyond the strike price. If one elects to purchase the contact at a higher price than originally sold, a short squeeze occurs. In order to substantially reduce this risk for a long investor that wishes to extract value throughout holding the underlying security will need to focus on writing far out-of-the-money covered calls/puts. Using my example above and my soft upside buffer of 7%-10% you can see that this allows plenty of upside while extracting a ~1% cash premium on a monthly basis. This buffer will substantially decrease one’s risk of relinquishing his shares.

Closing Out Contracts (Buy-To-Close)

One of the advantages of writing covered calls/puts is the ability to buy back the contact (buy-to-close) at a lower price and capture the spread prior to expiration. As the stock declines and rises the underlying call and put option will decline, respectively. As the stock of interest fluctuates throughout the contact timespan, the seller can cancel the contract via buying to close the option position (buy-to-close). This method accelerates closure of contracts to free up shares or cash to no longer run the risk of relinquishment or assignment and the ability to write another covered call/put on the same underlying security.

Conclusion

The covered call and put option strategy can serve as an opportunistic, aggressive or conservative way to utilize options to mitigate risk, generate cash via premiums and augment portfolio returns. This is a meaningful way to accentuate portfolio returns if the stock of interest decreases in value, trades sideways or trends upward (without crossing the strike price threshold) as the premium will be kept despite any of these outcomes. To offset the risk of losing out on potential appreciation, the option seller is paid a cash premium and never relinquished. Taken together, the owner of an underlying security/cash can leverage his/her shares/cash in a meaningful manner to mitigate risk and augment portfolio returns. This can be performed in a variety of ways as long as the options are sold out-of-the-money. This exercise can be repeated on a monthly basis for small yields that can be very impactful to any portfolio over the long-term. Thus far in 2016 I’ve had a few short squeezes however these were confined to more volatile stocks with less predictable outcomes and market upswings near expiration of the contacts. On an empirical basis, taking into account my pending option contacts, for Q1 and Q2 I’ve been able to capture 68% and 75% of all premiums and a 1.4% and 1.3% yield on the leveraged capital, respectively (Table 1). I will update readers periodically on my options updates.

Thanks for reading,

The INO.com Team

Disclosure: The author currently holds shares of FB, LUV, AAPL and CRM and the author is long all these positions. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.