Introduction

McKesson Corporation (NYSE:MCK) along with other pharmaceutical distribution companies such as Cardinal Health and AmerisourceBergen have been under tremendous pressure as of late due to political pressures regarding the pharmaceutical supply chain and drug pricing concerns. I recently wrote an article “McKesson Jumps 34% Off Lows – Now What” stating that the easy money had been made from the ~$150 level to the roughly ~$200 level. I also pointed out that greater than 98% of McKesson’s revenues come from pharmaceutical distribution and services domestically and abroad. Thus any impact to this business model will likely have direct negative implications with regard to revenues and EPS. At the closing of that article I stated that currently, McKesson’s P/E ratio sits at the top of its peer cohort and considering the stock has risen over 34% along with the potential erosion of the middle model, I’d be cautious buying at these levels despite additional upside based on its 52-week high of $240. Now enter the latest EpiPen fiasco and subsequent drug price scrutiny being thrusted into the spotlight. Due to a Tweet by Hillary Clinton regarding her distain for Mylan’s price increase, McKesson saw a $7 per share drop or roughly 4% drop in that same session. Since any disruption in this business model will negatively impact McKesson disproportionally compared to the insurance, pharmacy and pharmacy benefit manager (PBM) companies, I’d avoid McKesson especially after the ~30% move to the upside.

McKesson - Pharmaceutical Supply Chain Complexities

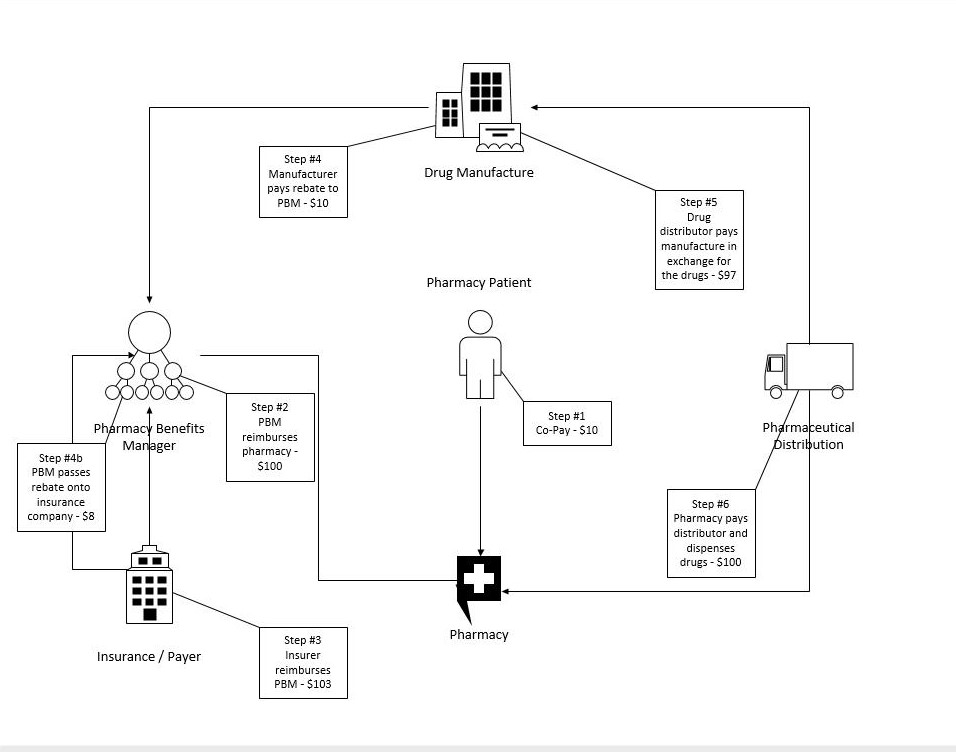

The interplay within pharmaceutical supply chain players can be a challenging dynamic to grasp. McKesson positions itself on the distribution side of the network, essentially serving as an intermediary between the drug manufacturer and the pharmacy. McKesson and other middlemen such as Cardinal Health and AmerisourceBergen purchase drugs directly from the manufacturer and then sell them to the pharmacy and capture the spread between the price they pay (to the drug marker) and the price they sell (to the pharmacy) the drugs. Below is a step-by-step breakdown of the pharmaceutical supply chain steps (Figure 1):

Step #1 – The patient pays co-pay for medication received at the pharmacy

Step #2 – Pharmacy Benefits Manager - PBM (CVS and Express Scripts) reimburses the pharmacy for the medication, PBM accepts a dispensing fee

Step #3 – Insurance companies reimburse the PBM for its members’ drugs

Step #4 – The drug manufactures pays a rebate to the PBM which is subsequently passed onto the insurance company. A portion of the rebate is retained by the PBM

Step #5 – Drug distributor (McKesson, Cardinal Health and AmerisourceBergen) pays the manufacturer in exchange for the drugs while collecting a fee in the process for distributing the drugs to pharmacies

Step #6 – The pharmacy pays the distributor and dispenses the drugs

Figure 1 – Original schematic - adopted from CNBC via Evercore ISI managing director Ross Muken

Is The Model Shifting Away From The Distribution Side?

In a previous article, I wrote that I had growing concerns about the middleman in the pharmaceutical drug supply chain. This is the bread and butter of many companies in this space, notably McKesson, Cardinal Health and AmerisourceBergen. Cardinal Health’s recent earnings report spooked investors as they lowered their full-year guidance albeit reporting top and bottom line beats for the quarter. The middleman model is slowly shifting away from the traditional means of delivering drugs to hospitals and pharmacies. More often than ever hospitals and pharmacies are establishing direct relationships with manufacturers thus buying direct. Manufacturers have increased their use of direct accounts when shortages arise thus disrupting the traditional distribution model long dominated by companies such as AmerisourceBergen, Cardinal Health and McKesson. Some drug makers will intermittently pull their products from distributors when manufacturing issues strain their supply. This action hits distributors particularly hard since they make their money by moving product. Drug distribution companies such as McKesson can continue to add value via consulting, analytics and knowledge surrounding providers’ purchasing habits. Additionally, the number of resources needed to build-out infrastructure in absorbing these duties would place a major constraint on many business models within hospitals and pharmacies.

I don’t think we’ll know the impact of this shift for some time however this is concerning considering McKesson just laid off 1,600 workers throughout the company. This move could be unrelated to the middleman business and more attributable to customer base losses. The company determined “reductions in our workforce would be necessary to align our cost structure with our business model.” Greater than 98% of McKesson’s revenues come from pharmaceutical distribution & services domestically and abroad. Any impact to this business model will likely have direct negative implications with regard to revenues and EPS.

Are McKesson’s Earnings Throughout 2016 A Red Flag?

The most recent quarterly results for Q1 2017 missed revenue by $630 million while revenue was up only 4.6% year-over-year. The quarter prior, Q4 2016, revenue targets were missed as well by $170 million while revenue was up 3.9% year-over-year. Even more, Q3 2016 results missed revenue targets again by $890 million while revenue was up 3.0% year-over-year. Although I’m not accounting for EPS or net profit figures, qualitatively, I’m looking at the overall growth from a total revenue standpoint. This figure cannot be inflated while EPS can artificially be engineered by removing shares via share repurchases. These missed revenue targets are a potential red-flag.

Moving Forward

MCK is doing what it can to be well positioned for future growth and success in the growing healthcare space assuming the middleman model remains intact. Despite concerns of the traditional distribution model being challenged, MCK has been highly acquisitive, growing dividends over time and buying back its shares to drive shareholder value. The dividend yield isn’t impressive however the company has plenty of room to increase the payout. Its major acquisitions and partnerships via UDG Healthcare plc, Sainsbury's pharmacies, Vantage Oncology, Biologics, Rexall Health, Albertsons and Wal-Mart position MCK to continue its competitiveness in the marketplace. The recent 1,600 layoffs in concert with three consecutive quarters missing revenue targets, I’d be wary of this stock. Currently, McKesson’s P/E ratio sits at the top of its peer cohort and considering the stock has risen over 34% along with the potential erosion of the middle model, I’d be cautious buying at these levels despite additional upside based on its 52-week high of $240. Since McKesson is lever to any political induced sell-off and/or legislative action within the space I’d avoid the stock at these levels.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author relinquished his position in MCK and has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.

I have just seen Hillary's plan for reducing drug costs. She must think we are a socialist country, not a democratic one, and we all know how many new drugs have been discovered and brought to market in the socialist and communist countries in the world. We have a viable and wonderful pharmaceutical industry that gives hope to so many individuals with life threatening diseases and she seems to be trying her best to destroy it. Her plan took six pages in small type to print out. It is like the Obamacare plan that we were told to pass first and than read it. There are changes that could be discussed that would give relief to those less fortunate than others, but Washington is so out of control with its rules and regulations, how about giving the local pharmacists a chance to show somebody how to lower drug prices without destroying an industry.

I have been in retail pharmacy for over fifty years and having direct accounts with the drug manufacturers used to be .the norm for most stores I worked in including my own which I operated for thirty years.

Most of the companies I did business with are no longer in operation, having been bought by larger companies,

Gone are Schering, Upjohn, and many more. The only companies I remember as not having direct accounts were Lilly, SKF, but there were others. You had a direct account because you were able to buy for less than the wholesaler charged and you had deals only available to direct accounts. There was little insurance business in the beginning and definitely no PBMs. If there were no PBMs and less interference from the insurance industry, the prices to the consumer would in my opinion drop dramatically. So many independents with the benign neglect of the government have been forced to close or sell and so, whoever is left standing can pretty much do what they want.

I'm in the health field and think its absolute thievery these distribution companies make and subsequently mark-up to retail pharmacies and thus the consumer and give the kickback to the insurance company.

We do not need a middle man distribution bureaucracy and its about time they (the federal government) eliminate this costly venture entirely. How much more in the way of pricing can the American consumer take? What sells in Europe and Canada for less than one dollar (or less) can cost upwards of $50 a pill. Ridiculous, a waste and a great short if I were playing this market because something has to give here folks.

a.caps

Great points and thanks for the comment. I think one overlooked area is how the U.S. subsidizes the rest of the world in terms of R&D and innovation. It's the U.S. where most of these cutting edge therapies originate and thus the majority of the expenses, infrastructure, taxes, employment, failed clinical programs and overall risk occur. This risk in deploying billions must have a financial reward on the back end or innovation, R&D, venture capital and employment in this field will drastically decrease. Patents expire and there must be a window to recoup the invested capital and expand the portfolio of compounds. The rest of the world didn't support these development efforts so in a way the U.S. subsidizes other geographies. The middleman model can definitely be refined however I think it's unfair to blame the pharma companies for pricing when these drugs save lives and only make up 10% of the overall cost of healthcare in the U.S.

Thanks, Noah

Well, all I have to say is that about ten percent of the US population has type 1 or 2 diabetes (this percentage will likely increase if we continue consuming high fructose corn syrup at the rates we currently do), and since 2001, the price of insulin has shot up into the stratosphere in the US alone but not other countries. Something has to give at some point.

venuspluto67

Thanks for the comment, I'm be writing a piece addressing the middleman system and how at each step within the supply chain, fees and charges are assessed. The amount of money that makes it back to the drug manufacturer is a fraction of the total cost. Using the EpiPen as an example, Mylan only receives ~$280 of the $610 list price so the current supply chain is definitely adding to the cost in a substantial way contrary to popular belief that big pharma pockets all this money. It's complicated and I agree that something has to give at some point. Too bad the sky rocketing costs of education and pensions aren't talked about in the way drug prices are in the media.

Thanks, Noah