It’s been barely five months since the Brexit referendum and yet here we are again, another European referendum, another political battle. This time around, it is Italy’s future in the balance and the Euro’s integrity at stake.

This upcoming referendum, due on Sunday, is a vote for constitutional reform that will abolish Italy’s dual parliamentarian system. Currently, Italy’s Parliament has two chambers, the Senate and the Chamber of Deputies. And, peculiar as it may sound, both have the same powers, but rather than balance they simply paralyze one another.

Why It Matters For The Euro

So, that begs the question, why is a referendum in Italy so important for the Euro? In one word: Banks. In the past few months, the Eurozone economy has started to show some signs of life. Among the data releases, Eurozone Manufacturing PMI rose to 53.7, retail sales in Germany has their strongest monthly gain in five years, and the Eurozone trade balance surplus rose by 37.8% over last year. Even in Italy, the Manufacturing PMI is holding above the 50 level, signaling expansion. All of which is "courtesy of a low Euro” that benefits European exporters. And yet, core inflation in the Eurozone is incredibly low at 0.8% and credit activity is weak, with the M3 level turning stagnant. Even the ECB’s €80 billion in monthly liquidity operations have thus far been insufficient to revive credit growth which is essential for the Euro recovery. At the heart of the problem is Europe’s banking system and its need to capitalize.

Because when banks are undercapitalized they are reluctant to lend, even when they face a tsunami of stimulus from the ECB. The lion share of undercapitalized banks are, unsurprisingly, in Italy. Italian banks, including Unicredit the county’s largest bank, require a massive capital injection. According to the Financial Times, the capital shortfall is so great in Italy that Italian banks have roughly €360Bln of bad loans but merely €225Bln in equity capital. In other words in order to survive, Italian banks need a massive capital injection that will largely be funded by Eurozone governments but will also include capital raised from investors. And for this to happen, there needs to be political stability, both in order to pass legislation to rescue the banks as well as to lure investors to invest in them. Moreover, other areas in the Eurozone banking sector would have a hard time raising capital amid fears of growing uncertainty in the region.

Two Scenarios To Watch

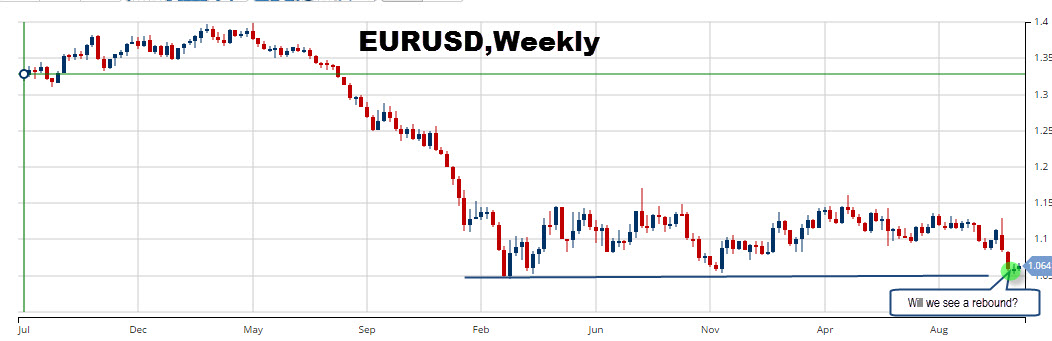

Naturally, the upcoming referendum embodies a rather binary scenario of yes or no; a yes vote for reform or a no vote against reform and in favor of keeping the current political gridlock. Currently, as the latest EUR/USD chart indicates, the market is pricing a high likelihood of a no vote. Among the reasons are the latest polls that suggest a majority favoring the no vote. Furthermore, there is wide support among the various political parties, towards maintaining the status quo. Both on Renzi’s right and left flank, from Silvo's Berlusconi’s Forza Italia party to Beppe Grillo’s Five Star Movement party.

If indeed, the no vote is the result, investors will hardly be surprised. This would mean that the much-needed rescue for banks will come later rather than sooner, as Renzi will be forced to resign, and what the next Italian government might look like will be unclear. And investors, fearing those political uncertainties, will be reluctant to “shoulder the burden” and invest in European banks and, as such, credit growth will expectantly remain stagnant. With Eurozone growth less likely to change (and more likely to deteriorate and lag the US), that will propel the Euro towards another selloff, with the EUR heading to parity with the dollar.

But, if we have learned anything from the Brexit vote and from the US election, it is that the polls can be wrong, and voters can always surprise. And, therefore, we should ready ourselves for both the likely and the unlikely. If Italy votes for reforms this Sunday, it means banks are more likely to get the capital they so desperately need, and credit flows will improve in Italy and the Eurozone which will allow the Eurozone recovery to gather more steam. Moreover, the Euro could get a windfall of foreign capital from encouraged foreign investors. All of which could narrow down to an impressive EUR/USD rebound, even though the long-term trend is likely to remain bearish.

Of course, the outcome is unknown, but those who prepare for either scenario are wise to do so. But, be forewarned, with polls being so unreliable, and unlikely scenarios materializing more and more, shorting the Euro is no longer a one-way bet.

Chart courtesy of MarketClub

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.