Due to drug pricing controversies, there has been much concern about how the outcome of the upcoming election will affect pharmaceutical stocks. Dr. Len Yaffe of Stoc*Doc Partners sheds light on the issues in this analysis of drug price negotiation policy, and focuses in on one California ballot proposition that aims to rein in costs.

One issue of focus in the election rhetoric is Medicare drug price negotiation, which is specifically precluded in the Medicare Modernization Act of 2003. Furthermore, a noninterference provision was included:

"In order to promote competition under this part and in carrying out this part, the Secretary (of Health and Human Services): (1) may not interfere with the negotiations between drug manufacturers and pharmacies and PDP sponsors; and (2) may not require a particular formulary or institute a price structure for the reimbursement of covered Part D drugs."

Additionally, the Affordable Care Act (ACA) subsequently made into law that Part D drug plans give nearly full access to drugs in six therapeutic categories: anticonvulsants, antidepressants, antipsychotics, antineoplastics, antiretrovirals and immunosuppressants, effectively eliminating price negotiations.

A Millman study found that these six protected classes represent 17–33% of Part D drug costs by Part D plan administrators. Also, the Congressional Budget Office (CBO) examined the effect of striking the noninterference provision and estimated that it would have a negligible effect on spending versus what private plans negotiate. It should be noted that a repeal of this provision would require action by both Houses of Congress.

"The recent weakness in pharmaceutical stocks affords an excellent buying opportunity in select names with promising pipelines, includingDURECT Corp."

California's Proposition 61 would require state agencies to pay the same price as the U.S. Department of Veteran Affairs (VA) for prescription drugs. California spent $3.8 billion on prescription medicines in fiscal year 2014–2015, and almost 83% of that was for Medi-Cal and the Public Employees Retirement System. It should be understood that many programs are excluded, including Medi-Cal Managed Care, local school district employees and local government employees, as well as the majority of Californians with private insurance. Included are the 3.0 million low-income people covered by Medi-Cal Fee for Service, prison inmates, Department of State Hospital patients and some state employees and retirees.

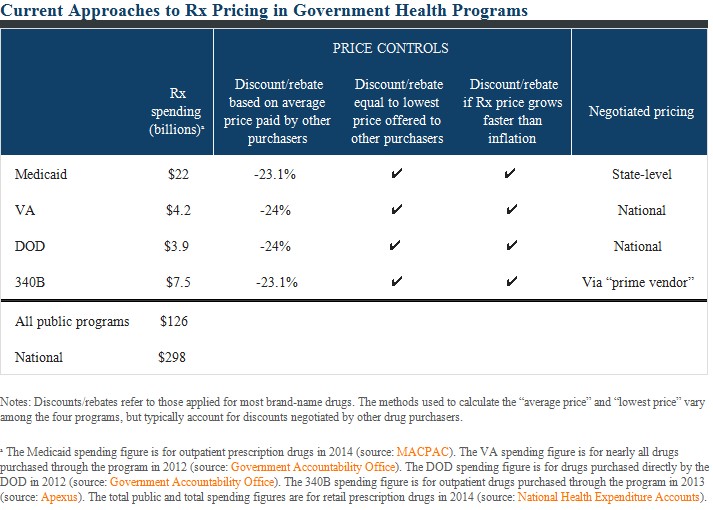

As it relates to Medi-Cal, the table above lists the price discounts afforded to various government health programs.

The VA pays the lowest price, and also directly negotiates even greater discounts with manufacturers. It has this ability due to assured volume based on compliance, and very aggressive formulary management. This can result in total discounts approximating 40%, versus the 23% for Medicaid.

However, Medicaid, in exchange for this discount, agrees to cover most drugs. For example, an analysis by the Lewin Group showed that, of the 300 drugs most prescribed to senior citizens, 35% are not included in the VA formulary, versus 6% in Medicare Part D formularies. A separate analysis by Einthoven and Fong stated that fewer than 33% of the 4,300 drugs available to Medicare beneficiaries are on the VA national formulary. Furthermore, according to Frank Lichtenberg, only 38% of drugs approved by the FDA in the 1990s, and 19% of the drugs approved since 2000, are on the VA national formulary.

The first issue for consideration is the disclosure of VA pricing. Without additional discounts, the VA and Medi-Cal should be charged similarly for prescription medicines. If the VA is not forced to disclose the incremental discounts it receives for market share guarantees through compliance and formulary control (neither of which is robustly permitted by Medicaid), then Medi-Cal's savings would be minimal. If Medi-Cal were to receive the full VA discount, then I would expect the drug companies to lower the incremental discount to the VA to strike a balanced price, and perhaps even raise prices to the private sector (20 million Californians). Therefore, in the aggregate, Californians would end up paying more for their drugs.

This is in no way intended to justify the high cost of prescription pharmaceuticals. As I have previously written, I maintain that there are more appropriate methods to control these costs. Additionally, it is critical to understand that the drug spend represents only 12% of total U.S. healthcare dollars. I forecast healthcare costs to grow at an average annual rate of 6% through 2030, at which time they will exceed $7 trillion, or 25% of GDP. I have provided a means of bending the cost curve in my article, "Solving America's Health Care Crisis."

From an investment standpoint, I think the recent weakness in pharmaceutical stocks (iShares NASDAQ Biotechnology Index [IBB] and VanEck Vectors Pharmaceutical ETF [PPH] down 10% and 9%, respectively, in the last month) affords an excellent buying opportunity in select names with promising pipelines. In this group I include Merck & Co. Inc. (MRK:NYSE), Celgene Corp. (CELG:NASDAQ), Regeneron Pharmaceuticals Inc. (REGN:NASDAQ), Tesaro Inc. (TSRO:NASDAQ), Ardelyx Inc. (ARDX:NASDAQ)and DURECT Corp. (DRRX:NASDAQ).

Dr. Len Yaffe has spent 30 years analyzing the healthcare sector, and he currently runs Stoc*Doc Partners, a healthcare hedge fund in San Francisco. He holds an MD from the Feinberg School of Medicine, Northwestern University.

Want to read more Life Sciences Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Dr. Len Yaffe: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: DURECT Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Clients of or funds controlled by Stock*Doc and/or Kessef Capital Management hold shares of the following companies mentioned in this article: Merck, Celgene Corp., Regeneron Pharmaceuticals Inc., Ardelyx Inc. and DURECT Corp. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: DURECT Corp. The companies mentioned in this article were not involved in any aspect of the article preparation. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview/article until after it publishes.

Article Source: Streetwisereports.com