Chinese policymakers are in the midst of a very delicate maneuver. With a hyped housing market and an unloved stock market, China’s policymakers want the “hot money” from real estate investment to be funneled away from housing and into the stock market. The problem? It won’t be easy and may require sacrificing economic growth, just at the point when growth has begun to stabilize.

The Bubble Returns

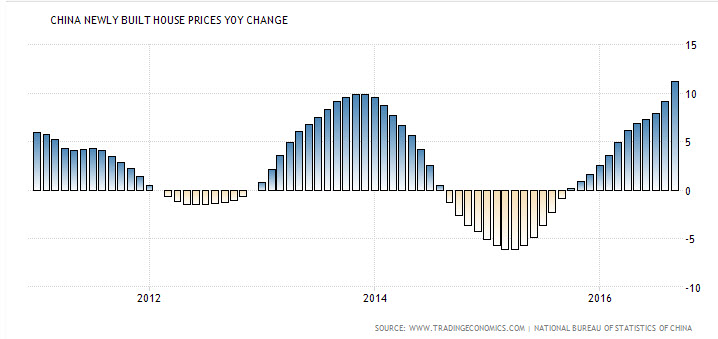

For some time now, Beijing has been well aware of the bubbly housing market. In fact, China has experienced two housing slumps in past decade, back in 2011-2012 and in 2014-2015, in both cases, the slump was largely due to the government’s efforts to curb prices in the preceding years. Those efforts were primarily through the implementation of new housing regulations and by clamping down on shadow lending. More importantly, the Chinese government put to good use its main monetary tool, the Yuan. By allowing the Yuan to strengthen, credit became more expensive and, as a result, the hype ended. But the price tag was dear because tightening efforts also resulted in a sharp slowdown in the Chinese economy and a meltdown in the Chinese stock market.

In 2015, the crisis was so severe, in fact, that Chinese policymakers had no choice but to drastically reverse policy by cutting lending rates, intervening in the stock market and, yes, as you might have surmised, devaluing the Yuan. But ironically, just when the easing measures have started to make a real impact, the housing market has once again become overheated and has turned bubbly.

China’s latest housing index, which encompasses the average prices of 70 major Chinese cities, rose by 11.2% year-over-year, the fastest pace since the housing market peaked back in 2014. In other words, the bubble is back.

Chart courtesy of Tradingeconomics

This time around, however, Chinese policymakers are trying a different tactic. Rather than focus solely on curbing the housing bubble, a secondary goal is to lure real estate investors into the stock market and replace their investment in real estate with stocks.

In the housing market, efforts to curb prices are focused on limiting even the possibility of purchasing more than one home, raising the minimum down payment needed for a mortgage and clamping down on brokers that hype the market.

And how exactly will Beijing lure investors back into the stock market after last year’s crash? That is the real news; China has embarked on new reforms that will seed the management of pension funds across several regions to China’s National Social Security Fund. Because China’s National Social Security Fund has a mandate to invest up to 40% of funds in the stock market, it will generate a steady flow of funds from pensions into the stock market. Notably, that is akin to what currently happens in developed countries. This means that not only billions will start flowing into China’s stock market but a steady flow of funds will also reduce volatility in China’s stock market, thus making investors feel more confident.

Delicate Solution, Tough Consequences

The solution of balancing the overvalued Chinese housing market with the stock market and reforming China’s pension market in the process sounds like a good solution for a long-term balance. But in the short term, the transition probably won’t be a smooth one. China’s real estate market is so hyped that in Beijing and Shanghai home prices jumped by 27.8% and 32.7% respectively. Such hype could only be curbed by tighter policy. But China’s banks are already fragile; in fact, only this week, Bloomberg reported that Bank Industrial & Commercial Bank of China Ltd was so short of capital due to bad loans that its bad loan coverage ratio fell to 136%, below the regulatory requirement of 150%. It’s not hard to speculate what will happen if policy tightens and the Yuan starts to rise. Banks will be under pressure and will have difficulty supporting growth. Furthermore, weakness in China’s banking sector will weigh on stocks, thus making the transition of funds from housing to stocks even more difficult.

So, what is China likely to do? Beijing will likely attempt to postpone, or at least minimize, the pain by gently curbing the Yuan weakness. That could mean some stability in the Yuan in the short-term. But that will hardly be enough; the Yuan must appreciate much more to curb the hyper inflationary-driven housing market. In the mid-term, China will likely have no choice but to tighten more; thus, the bust will be inevitable and so will the pain. And then, maybe, in the long-term, a delicate balance will be reached.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.