OPEC, led by Saudi Arabia, blundered when it decided to engage in a battle for market share in November 2014. It assumed it could drive American shale oil companies bankrupt and then pick up their market share.

But this strategy was destined to fail. For one thing, they didn’t take into account that American shale oil companies had hedged their future production. That protected the companies from experiencing the impact of lower prices to the extent that they had hedged.

Second, they didn’t take into account the American bankruptcy system. Companies can continue as “zombies” surviving by cutting costs to the bone, and selling assets to other companies at a discount to keep afloat. The buyers then have a lower “cost basis.”

Third, they didn’t take into account their own vulnerabilities. Sure, their national oil companies have low production costs but their oil revenues largely support the national budgets. They need high oil prices to balance their budgets, effectively making them high-cost producers (e.g., KSA about $65/b in 2017).

Round Two Blunders

The stated objective of the production cuts in November/December 2016 was to bring the rebalancing of the market forward, depleting excess inventories. Based on simple economics, lower supplies mean higher prices, ceteris paribus.

But higher prices have implications for supply. They provide an economic incentive for greater production than at lower prices. The net effect of a cut in supply is not simply the number of barrels cut, but rather the cuts less the new supply added.

Saudi Energy Minister Khalid Al-Falih was asked about the shale oil response to the cut at the press conference following the non-OPEC announcement on December 10, 2016. He explained the time lags involved in drilling, fracking and connecting the wells up to infrastructure. He concluded that there would not be any (production) response in 2017 (Watch Video at 51.34 for a complete discussion of the issue, or at 52.45 for the quote).

Source:OPEC

This was a major blunder, as I pointed out after I heard it. He didn’t take into account that there were 5,000+ “Drilled But Uncompleted” wells (DUCs) in the U.S. Nor did he take into account infrastructure projects near completion, such as the Dakota Access Pipeline (DAP).

CLR, for example, is devoting 90% of its budget in the Bakken to completing DUCs, which can be produced within months. And CLR claims it can earn a 100% ROR by completing DUCs at $50/b WTI.

And the DAP has been completed and will be pumping by the end of May. Bakken production in 2017 will be below pipeline capacity, according to CLR. The DAP effectively lowers the breakeven cost of Bakken crude by about $5 per barrel on crude that was being shipped by rail.

U.S. Production Response

Although the Energy Information Administration’s (EIA)’s weekly statistics are only estimates, and at times have been inaccurate, its numbers imply a very robust increase, contrary to Mr. Al-Falih’s assessment in December. Specifically, the EIA estimates that crude production has increased by 482,000 b/d from the last week of December to the second week of April. For perspective, KSA had agreed to cut 486,000 b/d in the first six months of 2017, and so the U.S. has already offset it.

Furthermore, the EIA projects that the U.S. production of crude and other liquids (primarily natural gas liquids, which are part of the petroleum supply) will rise by 1.37 million barrels per day (mmbd) by the end of this year from end-December 2016. For perspective, the total OPEC cut agreed-upon was just under 1.2 million barrels per day.

The end-December year-over-year rate of growth in crude production implied by the EIA projection is 26%, assuming all of this increase is due to shale oil. CLR expects to increase its production by 24%, so EIA’s number does not appear to be unreasonable. And we know that some long-cycle projects started years ago will be coming online in 2017-2018.

Equilibrium Price

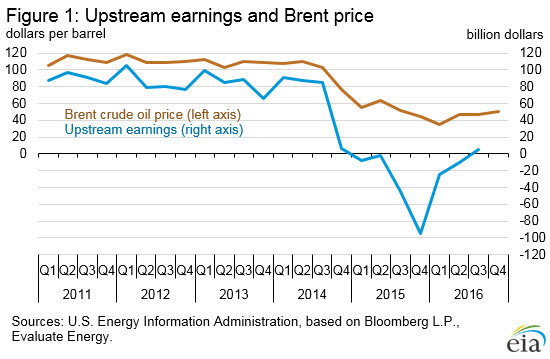

In addition, according to a study by the U.S. Energy Information Administration (EIA), global oil companies recorded positive earnings from the upstream operations in the third quarter of 2016. Total earnings from the 102 companies amounted to $4.8 billion. The companies in the study produced 33.9 million barrels per day, more than one-third of world output.

I calculated the average price of the nearby WTI crude oil contract during the third quarter, and it comes out to be about $45/b. Based on the EIA breakeven data, I would say that oil prices of $45 represent the best estimate of the short-term market equilibrium because upstream companies can survive but not add to production capacity.

OPEC is meeting in a month (May 25) with non-OPEC producers to decide whether to roll over the cutbacks to the second half of the year. The Saudi energy minister has indicated that OPEC is likely to extend the agreement.

Conclusions

If oil prices remain in the range experienced thus far in 2017, the additions to U.S. supply will offset OPEC’s entire cut by October, based on the EIA projections. Therefore, oil prices are likely to have already peaked in 2017, as U.S. supplies increase.

Furthermore, the futures market will be focusing on what will happen at the end of the cut in 2018. OPEC’s cut of 1.2 mmbd, and the non-OPEC cut, will be coming back on the market. That expectation will weigh heavily on prices.

In addition, American shale oil producers will have hedged into the future, a factor OPEC fails to even mention, let alone consider.

Given the above, I have reached the conclusion that extending the cut will actually lead to extending the glut, instead of shortening it. The reason is that the supply response is simply too robust, and hedging extends it into the future.

Therefore, I believe an extension would be another blunder. Not extending it would lead a sharp price drop, but would also cause shale oil production to drop once again, with a time lag.

That is the most effective way to (eventually) end the glut, as opposed to supporting oil prices. Either way, the oil market will likely face further supply problems for the foreseeable future.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

I have read many similar projections regarding the potential for the oil market to face supply shortages very soon. I look forward to reading the rest of your posts on this topic, as this one is extremely well-written and informative. I love your use of infographics - they really help me understand the stats.

A thorough discussion of the Supply side of the equation. But no discussion can be complete without at least

a mention of the Demand side.

Please see my previous article which includes a demand discussion: http://www.ino.com/blog/2017/04/crude-oil-seasonality-inventory-rebalancing-and-production-cuts/#more-42510

Thanks, Robert