Arrogant OPEC members thought they could beat American shale oil producers into submission in a market share battle. But instead, they caught a tiger by the tail, and now the tiger is turning on them.

OPEC producers were bragging back in late 2014 that they had much lower costs of production than American shale oil producers and could easily win back market share by undercutting their prices. But they failed to take into account that they needed higher prices than shale oil producers because oil revenues largely support their national budgets.

Low oil prices caused huge national budget deficits in OPEC countries. They did hurt the smaller, leveraged shale producers; however, they were able to take advantage of the bankruptcy laws in the U.S., not a real option for the producing countries. Their best response is to devalue their currencies, but there are a host of economic issues associated with exercising that option.

Fresh data were reported by OPEC and the U.S. Energy Department recently. The data imply that global oil stocks will rise, instead of decline in 2017, even with the OPEC-non-OPEC production cutbacks.

OPEC’s Outlook

OPEC released its 2017 Monthly Oil Market Report (MOMR) for May. It includes a feature article. It concludes by stating:

“A large part of the excess supply overhang contained in floating storage has been reduced and the improvement in the world economy should help support oil demand. However, continued rebalancing in the oil market by year-end will require the collective efforts of all oil producers to increase market stability, not only for the benefit of the individual countries, but also for the general prosperity of the world economy."

In December, OPEC Secretary General stated in a speech in New York that U.S. companies should join OPEC in reducing production. And in Houston in early March, he stated that shale oil producers were not a risk but a "strategic partner." I find these statements completely detached from reality. U.S. law specifically prohibits collusion on production or prices with cartels.

The May MOMR has increased its projections for U.S. crude production in 2017. Since the November OPEC agreement, its projection of non-OPEC supply growth in 2017 (976,000 b/d) is now four times its prior estimate.

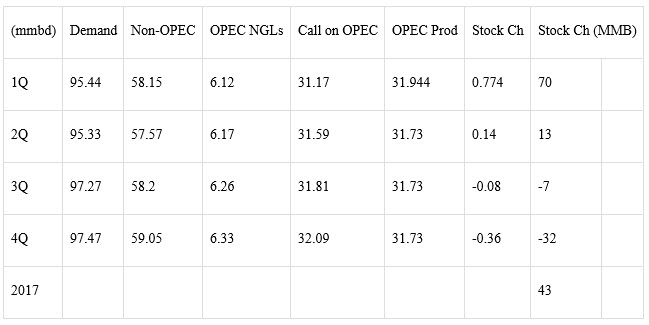

OPEC estimates that global inventories are 276 million above the 5-year average. And it estimated its production in the first quarter to be 31.944 million barrels per day. Assuming April's production of 31.7 holds for the remainder of 2017, there will be a total global stock build of 43 million in 2017:

Energy Department’s Outlook

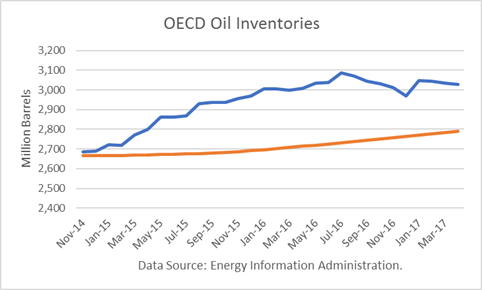

The Energy Information Administration (EIA) reported that global OECD oil inventories dropped by six million barrels to end at 3.027 billion barrels. That is sixty million barrels higher than end-December, when the OPEC-non-OPEC cuts went into effect.

As a result, the size of the surplus, compared to the 5-year moving averaged, increased from 204 million barrels December 2016 to 237 million in April 2017. OPEC’s goal had been to reduce OECD to the 5-year average, and it had made remarks that it thought it could by the end of the first six months of the agreement.

Even worse, the EIA data show that OECD global stocks will end 2017 66 million higher than 2016. Furthermore, it projects an additional build in 2018 of 75 million barrels.

The EIA data reflect a rise in OPEC crude production from the January-April period. That is likely if Libya and Nigeria impose peaceful conditions to ramp their output back up.

The EIA also projects that December 2017 crude production in the U.S. will be about 960,000 b/d higher than in December 2016. U.S. production is forecast to surpass the cyclical peak of 9.6 million barrels per day in November 2017. The EIA expects U.S. production to ramp-up another 610,000 b/d in 2018.

Conclusions

Global oil inventories will increase notwithstanding the production cuts being extended. As a result, I expect continued downward pressure on oil prices.

The second half of 2017 will provide some relief, but the market will begin focusing on early 2018, when stocks begin to rise again.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

gostei do produto - "I like the product"

Translated via Google Translate

We're living in fantasy land. EIA numbers are not believable and OPEC lies all the time. Note that most of the shale producers reporting low cost production are public companies. They care more about their stock price than the oil price. Smaller, private oil producers in the U.S. are going broke. Timing is the eternal question.

thank you