The S&P 500 (CME:SP500) closed for the week at 2,472.10, after hitting an all-time record, after gaining 10.5% year-to-date. The S&P’s forward Price-to-Earnings ratio, a key ratio for investors, is 17.8 above the 10-year average of 14. And this brings up the inevitable pondering; is there any juice left in the S&P 500?

In searching for an answer, the intuitive starting point might be the S&P’s valuation. We’ve already pointed out that the S&P 500 is trading at a high valuation compared to its 10-year average. Furthermore, according to Factset research, earnings for the 500 companies which comprise the S&P 500 are expected to rise by 9.3% as compared to 9.26% in 2016. Now, while that is a solid figure, it also suggests earnings growth is not accelerating and may even suggest the acceleration in earnings growth is over. And if earnings growth is likely to decelerate in the coming years it cannot account for the S&P500’s 17.8 PE ratio. So, there’s no valid reason why the S&P’s valuation would be the catalyst for another surge. Why not? Simply because it's too high. In fact, the real catalyst isn’t within the S&P500 or even within the stock market; instead, the real reason lies within the Bond market.

S&P500 vs. Treasuries

When stocks are tanking, and especially during times of turbulence, Treasuries are investors’ go-to safety net for the secured yield they provide. But what happens when inflation is on the rise? Bond prices tank and stocks become the “safety net.” You read that right. Because there is no viable alternative, investors, in their race for yield, will pile into equities, in our case, the S&P 500, and sell their bonds.

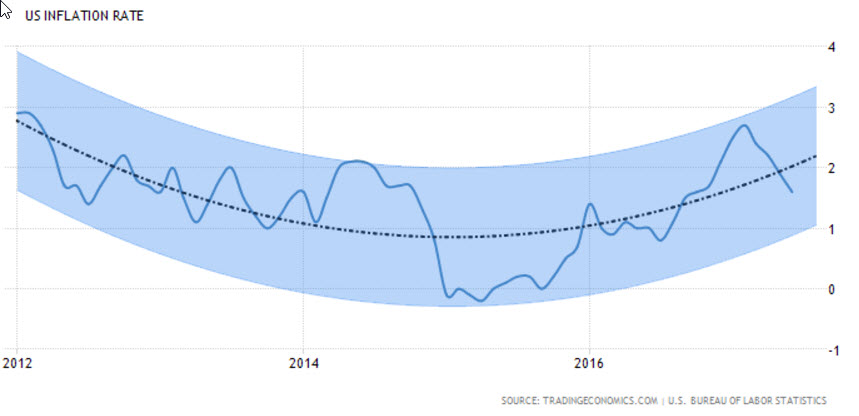

As can be seen in the chart below, despite the latest setback in headline inflation, the overall trend for inflation is higher. Indeed, after a period of subdued inflation between 2015 and 2016, it only makes sense that inflation will be making a comeback.

Chart courtesy of Tradingeconomics

And evidently, what we’ve got on our hands is a rising inflation trend and a tanking bond market. And that inevitably will propel the S&P 500 higher. Earnings took us so far, but with lofty valuations, and no acceleration in earnings growth, the next push for the S&P 500 will came from the Bond market exodus.

Indeed, Treasuries have been gaining some ground, and Treasury yields have fallen since 2014, generally on the back of easing inflation, but that is a mere blip in an overall changing trend. With inflation set to rise again so will the bearish trend for bonds. If we apply some basic technical analysis to the Treasury yields chart below, we can see that the latest peak in the first quarter of 2017 broke the bearish trend in yields and the bullish trend in growth. Combined with the latest support at 2.2%, it signals a potential uptick in yields and a fall in bond prices.

Chart courtesy of Bloomberg

But there’s more, a “wild card,” if you will, that should be mentioned, and that is the Fed. The Federal Reserve currently holds approximately $2.5 Trillion of Treasuries on its balance sheet. As inflation begins to trend higher the Fed could eventually be compelled to start offloading its Treasury holdings, thus placing further pressure on the bond market and forcing investors to, once again, pile into equities.

So, how much juice is left in the S&P 500 (CME:SP500)? Once the inflation rate hits the 3% level, it could signal that the mid-term inflation cycle is over and investors will feel confident enough to hold bonds again. When that happens and if, as expected, earnings growth does not accelerate, the lofty valuations of the S&P 500 will be back in focus and investors will flee to the safety of the bond market. But, until then, the S&P 500, despite being expensive, has further to go and more gains to squeeze.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Why wouldn't investors leave both the equities and bond markets in favor of Precious metals and the fundamentally strong PM miners? I think this was overlooked and the most probable scenario. Cheers!

Stay tuned for future results. Markets can be and stay over valued for extended periods of time. Like the saying says. The Market Climbs a Wall of Worry. We are all scared as hell right now. This might be the time to invest.

It would seem logical that investors would leave an overpriced market to find an underpriced market(s). Europe and China would both seem to be markets worthy of attention.

Fantastico