Peak demand for crude at refineries and for products to consumers is drawing to a close this season. Together, they caused total U.S. oil inventories to drop by 49 million barrels from their peak in the week ending June 9th. Total U.S. oil inventories stand at 1.304 billion barrels in the week ending August 11th, 58 million barrels lower than a year ago.

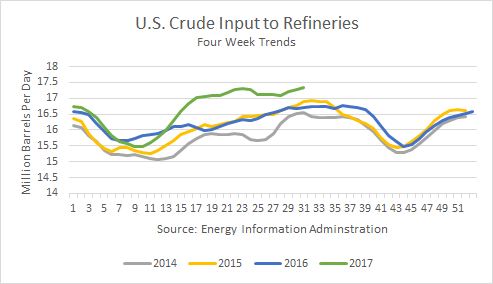

Refinery demand for crude oil set a new record high this summer, as the 4-week trend reached 17.458 million barrels per day, 4.4% higher than last year. As depicted in the graph below, refiners will soon be dialing back their operations for maintenance, and this will reduce the demand for crude at U.S. refineries by about 1.5 mmbd.

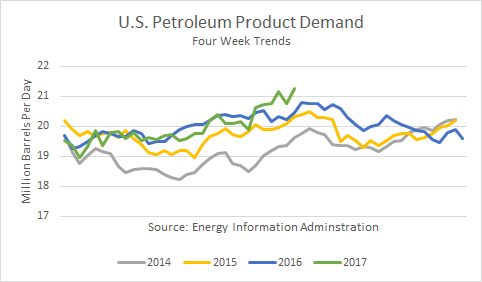

Domestic demand was relatively strong this summer, up about 2.0% from last year. Gasoline demand was somewhat disappointing, but distillate demand spiked. As shown in the graph below, seasonal demand has likely peaked and will be headed lower in the weeks and months ahead.

The primary driver for high refinery operations was the demand for exports. Petroleum refiners increased exports by over 500,000 b/d, about 15 percent. Reports have been circulating that refineries in Mexico and throughout Central and South America are in need of maintenance and have been operating at lower-than-normal levels.

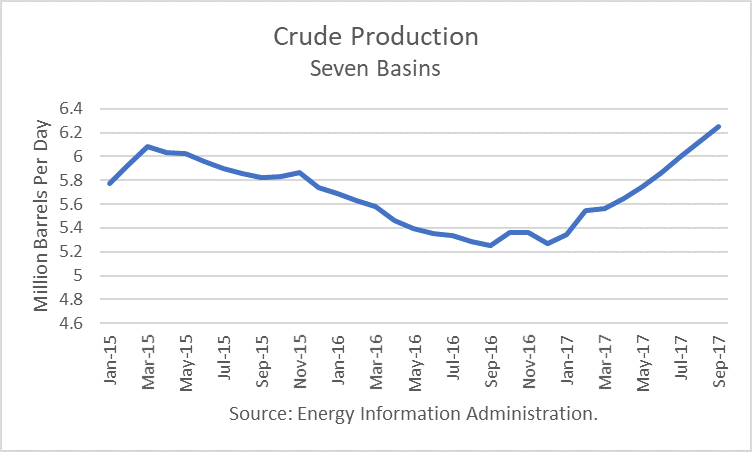

While the demand for crude and products is likely to decline, the production of domestic crude is likely to keep rising. Specifically, production over the past 4 weeks is 11.0% higher than the same period last year, and the Energy Dept. projected that shale oil production in the seven primary shale oil basins should increase by 117,000 b/d in September, an annualized rate of gain of 1.4 million barrels per day (mmbd). In the year-to-date, oil production will have increased by a 1.3 mmbd annualized rate through September. However, the September gain is slightly slower than the gains estimated for July and August of 130,000 b/d. Crude production in September is projected to be about 220,000 b/d higher than the peak in March 2015.

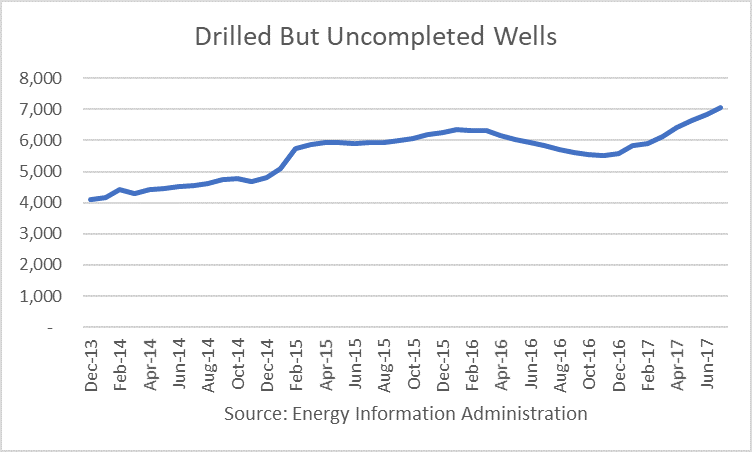

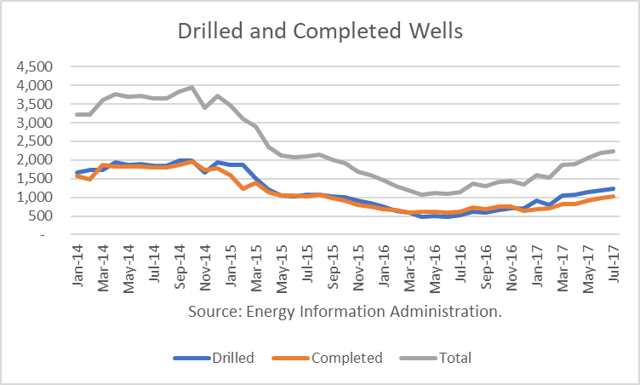

The EIA also reported that “Drilled But Uncompleted” wells (DUCs) rose to a record high of 7,059 in July, up 208 from June. The inventory of DUCs represents production that theoretically can be brought online in a matter of months, given the availability of completion crews.

The number of drilled wells has exceeded the number of completed wells since November. The total number of drilled and completed wells rose by 60 in July, as shale oil activity continues to ramp higher despite prices averaging below $50 since May.

Saudi And Russian Exports

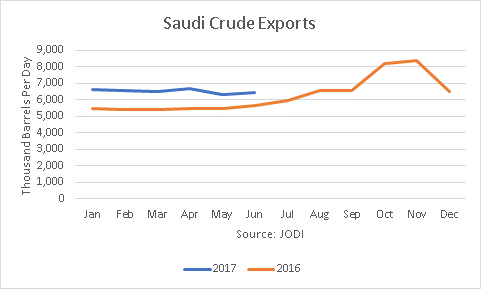

On July 24th, Saudi energy minister Khalid Al-Falih stated that KSA would limit August crude exports to 6.6 million barrels per day (mmbd). The media reported that would be a reduction of one million barrels a day from August 2016.

But the latest data reported by JODI shows that August 2016 production was 6.6 mmbd, effectively no reduction after the “cuts” have been in effect. Saudi Arabia itself had reported the data to JODI.

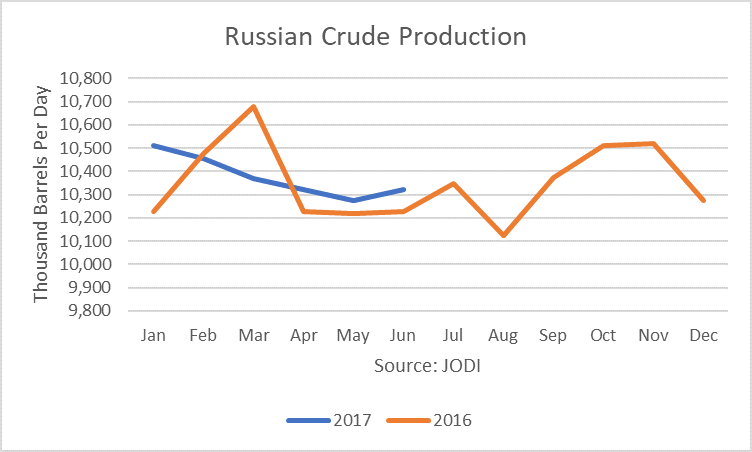

The latest data reported by JODI shows that Russian crude production averaged 10.377 million barrels per day (mmbd) for the first half of 2017, up slightly from 10.342 mmbd in the first half of 2016.

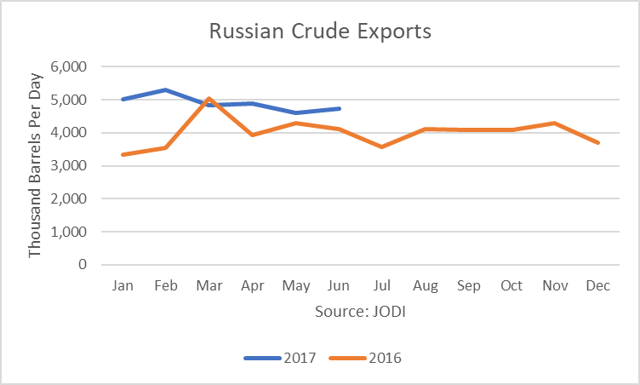

However, its crude exports were 4.892 mmbd in the first half of 2017, up 21% (851,000 b/d) from the first half of 2016. This data was provided by Russia itself and contrasts with the impression that Russia has reduced exports to support oil prices.

Conclusions

WTI crude oil futures were unable to hold at $50/b during the peak demand period this summer. With market conditions likely to deteriorate in the weeks and months ahead, look for oil prices to test their June low of around $42/b.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Thank you for a succinct overview. While I hold Chevron and Exxon/Mobil, most materials that I review and read lack the clarity thatI just received. With hurricane Harvey racing in there should be a short term domestic effect.