According to OPEC, global OECD oil inventories fell 22 million barrels in June to end at 3.033 billion. But that figure is 252 million barrels above its five-year average. OPEC has targeted reducing those inventories to the average level, but its own supply-demand projections imply that goal will not be met through 2018, assuming it maintains production at the July 2018 level. In fact, there will be a 45 million barrel build in 2017, and an additional 162 million barrel build in 2018, even if production does not rise after the extension ends in March 2018. This implies that oil prices will need to be below marginal production costs for some time in order to limit production growth.

July Production

OPEC reported that production rose by 173,000 b/d in July to average 32.869 million barrels per day (mmbd). OPEC’s 32.5 mmbd ceiling included Indonesia but did not in Equatorial Guinea, and so the adjusted July figure was 33.449. This implies that OPEC produced 949,000 b/d above its ceiling, a large failure, especially considering that it had been claiming to be 100% (or more) compliant with its quotas.

The biggest gain in July came from Libya, 154,000 b/d. That country’s production topped one mmbd for the first time in years. Production in Saudi Arabia rose by 32,000 b/d to 10.067 mmbd, which is above its production ceiling, according to secondary sources.

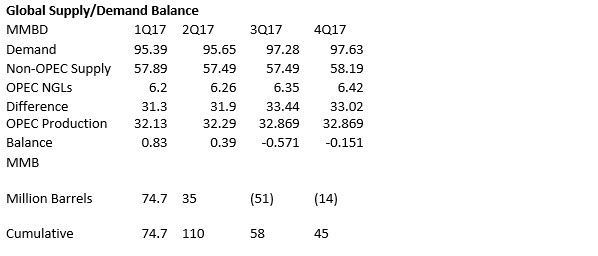

2017 Global Supply/Demand Balance

I combined OPEC’s own projections of demand and non-OPEC supply with OPEC’s July production to forecast for the balance of 2017. The figures show a 51 million barrel decline in the third quarter and a 14 million barrel decline in the fourth quarter. However, inventories rose by 110 million barrels in the first half of the year. And so the annual impact is a 45 million barrel build for the year.

At the May OPEC meeting, Saudi Arabia's Minister of Energy, Industry and Mineral Resources, Khalid A. Al-Falih, remarked, "The market is now well on its way toward rebalancing." After the meeting, Mr. Al-Falih said in a press conference that the current production quotas will "do the trick" of rebalancing stocks to normal levels within six months.

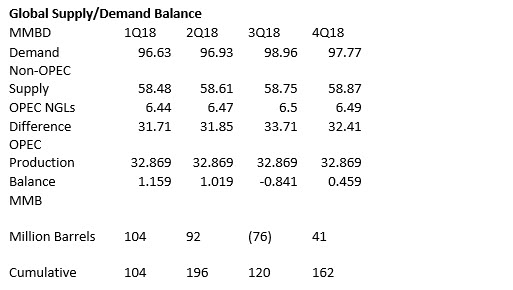

2018 Global Supply/Demand Balance

The OPEC deals are expected to extend through March 2018. If they end then, a large “slug” of oil may be hitting the market. But for the sake of argument, I assumed that OPEC’s July 2017 production extended through 2018.

Using OPEC’s own estimates for global demand and non-OPEC production, OECD oil inventories would rise by 162 million barrels in 2018. In other words, instead of an improving outlook, the glut would increase considerably.

Conclusions

Because world storage capacity has limits, I would expect the market to solve this problem by pushing oil prices enough below marginal production costs, for a long enough period, to dis-incentivize oil production. This implies a price range of about $35-$40 per barrel for an extended period of time, six-to-nine months, or more if the OPEC/non-OPEC production slug comes to market in the second quarter of 2018.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

I'd imagine a price regime of $35-40/bbl would leave the shale companies in even greater financial distress, and the numbers of bankruptcies to continue apace throughout 2017 and into 2018. At this point, shale company investors and lenders must be getting pretty impatient with non-performing shale investments. Indeed, most shale company debt will never be paid back; it is collectively a whopping $350+ billion for the industry as of 2017. The chances of this ever getting paid back are, IMO, pretty dim.