Introduction

Facebook Inc. (NASDAQ:FB) is on tap to report Q4 FY2017 earnings along with its full-year FY2017 numbers. Facebook recently breached the $189 level as earnings approached, however it recently sold off from these highs following news that Facebook would overhaul its news feed in favor of “meaningful social interactions” versus “relevant content.” I think this news was timely with the upcoming earnings announcement as Facebook will once again deliver phenomenal growth numbers across the business with beats on both top and bottom lines. Once the growth trajectory is affirmed with EPS moving in lock-step, the stock only becomes cheaper, and thus this pull-back could be a rare buying opportunity before the stock breaking through the $200 barrier. Facebook ended 2017 with a monster return of 53%, however, considering its growth the stock remains relatively cheap with a P/E of 34.8 and PEG of 1.23 implying an annual EPS growth rate of 28.3%. Once the newly designed news feed launches in conjunction with earnings later this month, I think the stock could break through the $200 level imminently. I feel that Facebook represents value even after this massive run through 2017 and I maintain my long thesis with a price target of $230 by the end of 2018.

News Feed Overhaul

Facebook announced major changes are coming to its news feed to prioritize “meaningful social interactions” on the social media’s news feed as opposed “relevant content.” With this reformatting, users will start seeing less public content from businesses or publishers and more posts from their friends. Mark Zuckerburg expects that the time people spend on the social media network will decrease as a result however it will be “more valuable.” Facebook sold-off on the news as investors and analysts regarded this as an overall negative impact on earnings. Facebook sold-off over 5% on the news or $10 per share as analysts weighed in on the new roll-out. Overwhelmingly, analysts remain positive on shares of Facebook with JP Morgan’s Doug Anmuth maintaining his overweight rating and a $230 target price. I feel that the news feed overhaul will be negligible to earnings, especially over the long term. This sell-off is an excellent opportunity to enter the stock before what will likely be a fantastic earnings announcement.

Facebook Is An Inexpensive Stock

Per Fidelity, Facebook trades at ~$179 per share with a P/E ratio of 34.8 and a PEG ratio (P/E ratio divided by growth rate) of 1.23 suggesting an annual growth rate of ~28% in EPS. EPS at the end of 2016 was $3.56 thus factoring in a 28% premium we would theoretically arrive at $4.55 at the end of 2017. However, Facebook has already surpassed this estimate and currently sits at $5.16 EPS with one more quarter remaining in FY2017. Assuming Facebook continues to trade at a P/E of ~35, this translates into an EPS of $6.60 and stock price of $231 per share by this time next year.

Like analysis from Noah Kiedrowski?

Get Our Free Political Plays Newsletter

This free, bi-weekly newsletter from Noah Kiedrowski will give you actionable stock plays based on political action. Spot and profit from the political plays that matter.

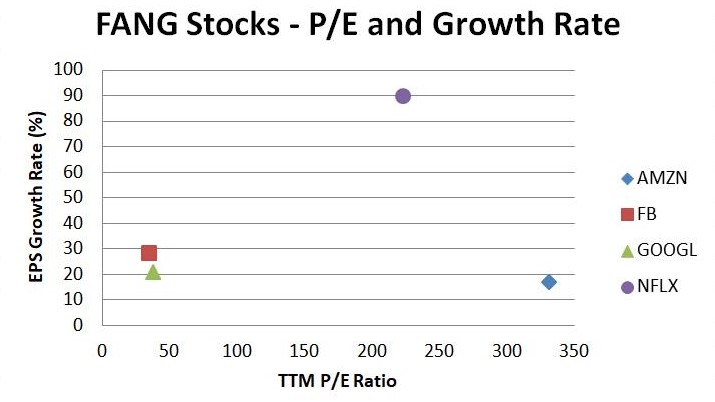

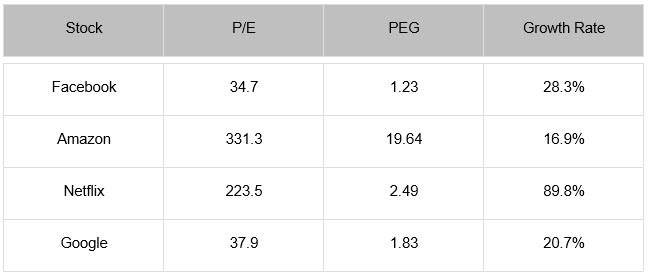

Currently, similar high growth technology companies such as Google, Amazon, and Netflix possess a less favorable profile when looking at the P/E ratios and growth rates (Figure 1 and Table 1). Facebook's projected growth is greater than Google's, yet Facebook has a P/E ratio that's less than Google's and a fraction of Amazon's and Netflix's. Facebook has the lowest PEG ratio of any FANG stock as well. On a relative basis, Facebook is inexpensive as compared to other large tech companies with a similar growth profile.

Figure 1 – EPS growth rate (derived from PEG ratio) versus TTM P/E ratio

Table 1 - Comprehensive valuation and growth overview of the FANG stocks

Facebook’s Ubiquity and Growth

Facebook’s ecosystem includes its flagship Facebook social media platform, Instagram, Messenger, and WhatsApp while the company is making inroads into virtual reality via Oculus and artificial intelligence. All these digital platforms are ubiquitous as society migrates to social, mobile and cloud as the primary means of conducting business and personal communication. Facebook and its properties have dominated the social media landscape for years and will likely continue its dominance. Instagram, in particular, has been growing its audience by leaps and bounds growing from 400 million active users in September of 2015 to over 700 million monthly active users as of August 2017.

Facebook has posted robust growth in all metrics about user growth and engagement while monetizing has moved in lock-step, the latter more specifically in the last few years. Facebook's earnings growth has been tremendous and has posted accelerating revenue growth over the past four years. EPS has increased from $0.02 at the end of 2012 to $3.56 at the end of 2016. For such a large capitalization company such as Facebook, this growth is very impressive. Utilizing the previous four quarters as a barometer, this growth doesn't appear to be slowing down anytime soon while silencing rivals such as Snap Inc. (NYSE:SNAP) in its path. Facebook makes acquisitions to drive the business now with Instagram and WhatsApp and into the future of virtual reality with Oculus. Facebook just recently acquired teen app called tbh in October of 2017. Based on my analysis, Facebook provides the most durable growth out of all the other FANG stocks with a lower P/E and PEG ratio and thus provides a margin of safety. Facebook has plenty of room to appreciate into the years ahead given its growth, and even if the stock appreciates to ~$200 range soon, it will still be inexpensive on a relative basis. Facebook makes a compelling case that it is the superior choice for long-term growth with a low-risk profile within its cohort.

Facebook Dominates While Snapchat Struggles

Facebook and its properties have witnessed a virtual monopoly in the general social media space logging more than 2 billion users worldwide. Instagram has witnessed phenomenal growth over the past few years as well logging 700 million users. Recently, Snapchat was projected to be a significant threat to Facebook and its social media dominance. Snapchat was met with stiff resistance when Facebook launched a direct competitor with Instagram Stories. In August of 2016, the launch of Instagram's clone of Snapchat's Stories coincided with a substantial decrease in Snapchat's growth. By October of 2016, Instagram Stories had 100 million active users, just shy of Snapchat's total number of 153 million at that time. Now Instagram stories have over 250 million daily active users far exceeding Snapchat's user base of 166 million.

It's clear that Facebook has outcompeted Snap at its own game while potentially arresting any future growth. I think Snap was the most legitimate potential competitor in the social media space and now it's clear that Facebook retains the title of the go-to platform for users and advertisers. To further substantiate this thesis, recent data has demonstrated plummeting app downloads for Snapchat. SensorTower a firm that tracks app analytics showed Snapchat's year-over-year downloads had dropped 22% in the first two months of the second quarter in 2017. All this while Instagram downloads have grown and WhatsApp released its version of Stories to further the arresting of Snapchat's growth.

Conclusion

Despite the negative comments regarding the revamped news feed on the social media platform, Facebook represents value and could be a great buying opportunity moving into earnings later this month. In my opinion, Facebook is the most compelling high-growth technology stock when compared to other companies with a similar growth profile and market capitalization such as Amazon, Netflix, and Google. Facebook and its properties are the go-to social media platform for both users and advertisers. Facebook has shown double-digit growth in revenue, EPS, and free cash flow and has continued this trend through Q3 2017, posting double-digit growth across all earnings metrics. Assuming Facebook continues to trade at a P/E of ~35, this translates into a stock price of $231 per share by next year which is in-line with recent analyst upgrades and boosted price targets. On a relative basis, Facebook remains inexpensive as compared to these other large growth technology companies and I feel Facebook Inc. (NASDAQ:FB) is the superior stock with a lower risk profile that could easily break through the $200 barrier imminently.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses. The author is the founder of stockoptionsdad.com a venue created to share investing ideas and strategies with an emphasis on options trading.