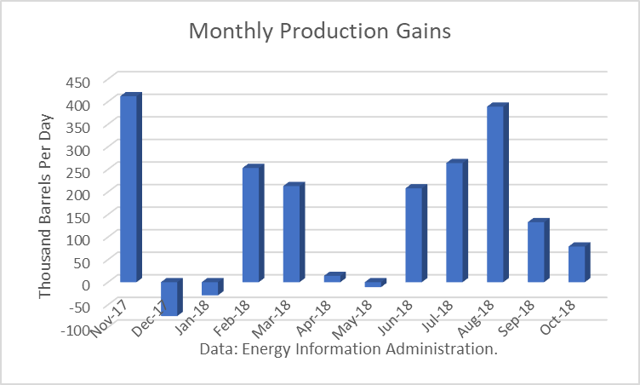

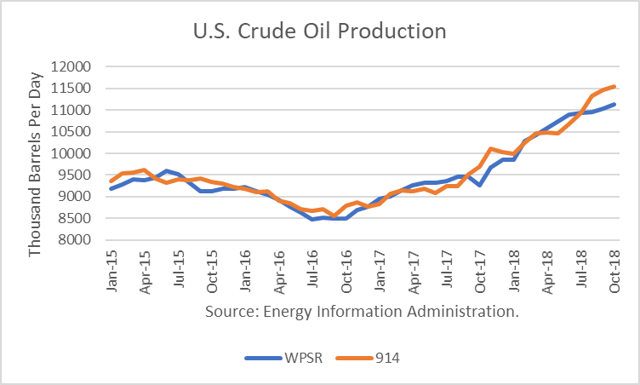

The Energy Information Administration reported that October crude production averaged 11.560 million barrels per day (mmbd), up 79,000 b/d from September. This was a slowdown in growth from the spectacular numbers recorded in July and August.

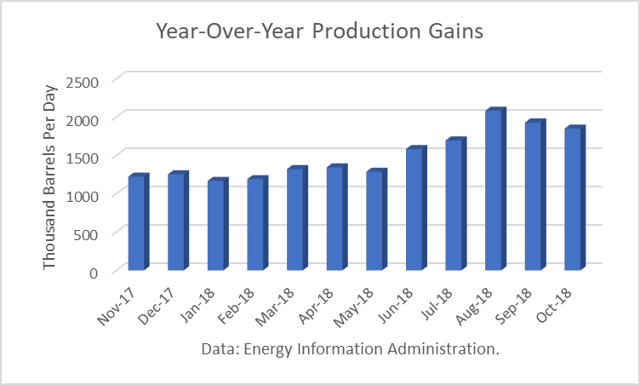

However, the year-over-year gain was still a very impressive 1.850 mmbd. And this number only includes crude oil. Other supplies (liquids) that are part of the petroleum supply add to that. For October, that additional gains is about 600,000 b/d.

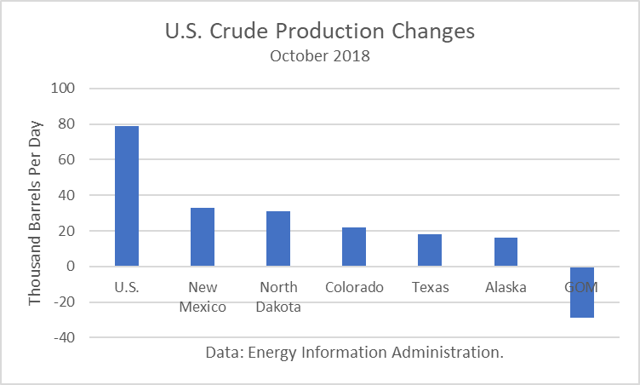

The gain was led by a 33,000 b/d increase in New Mexico, a 31,000 b/d rise in North Dakota and a gain of 22,000 b/d in Colorado. Weather factors affected the overall gain, as production fell by another 29,000 b/d in the U.S. Gulf.

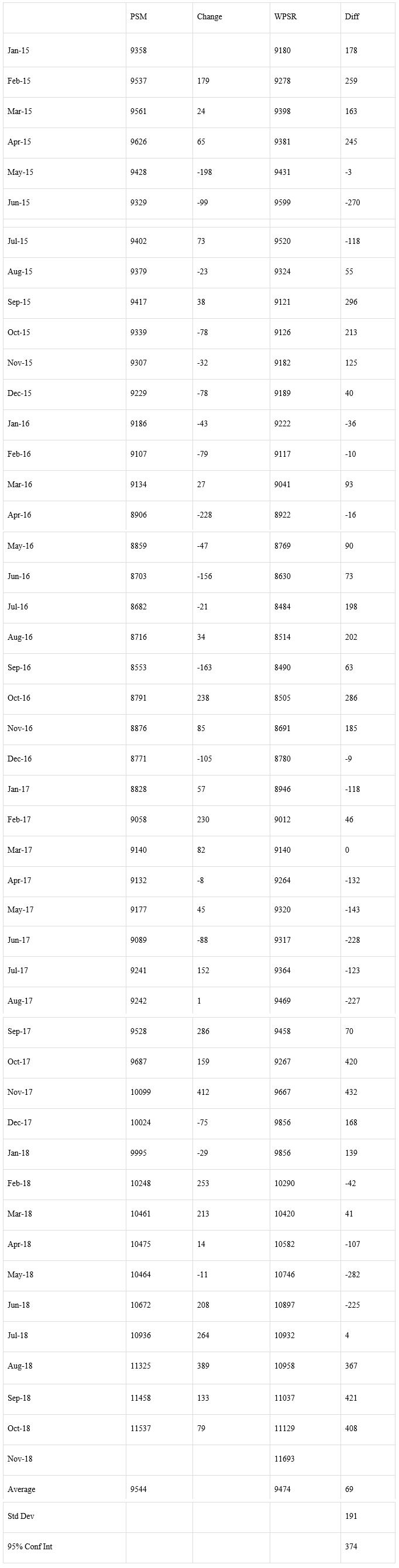

The EIA-914 Petroleum Supply Monthly (PSM) figure was 408,000 b/d higher than the weekly data reported by EIA in the Weekly Petroleum Supply Report (WPSR), averaged over the month, of 11.129 mmbd.

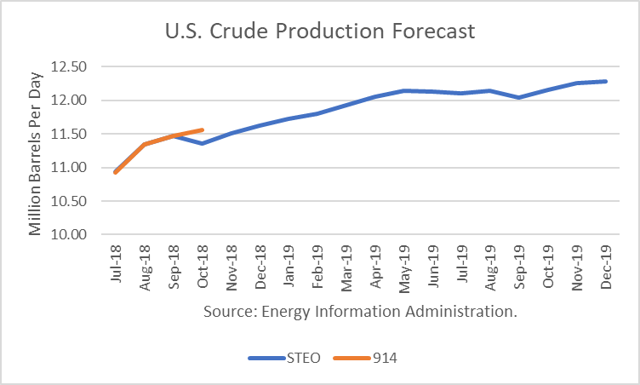

The October figure was also 200,000 b/d higher than the 11.360 mmbd estimate for that month in the December Short-Term Outlook. That implies a potential upward revision to EIA’s model in future production levels.

The EIA had been projecting December 2018 output of around 11.240 mmbd for much of the year. Instead, it will be around 11.8 mmbd.

The EIA is projecting that 2019 production will average 12.06 mmbd. As shown below, the growth rate is very slow through September.

According to another report, the Permian Basin is expected to add as much as 2.0 mmbd in 2019 as three new pipelines come online. And in 2020, more new pipelines are expected.

Conclusions

Shale oil production continues to exceed expectations that have been revised upward substantially. The drop in crude price should be expected to slow down the rate of growth. However, shale production growth lags prices by about six months. And the additional pipeline capacity in the Permian will effectively lower breakeven costs. And so EIA’s 2019 forecast still looks conservative.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.