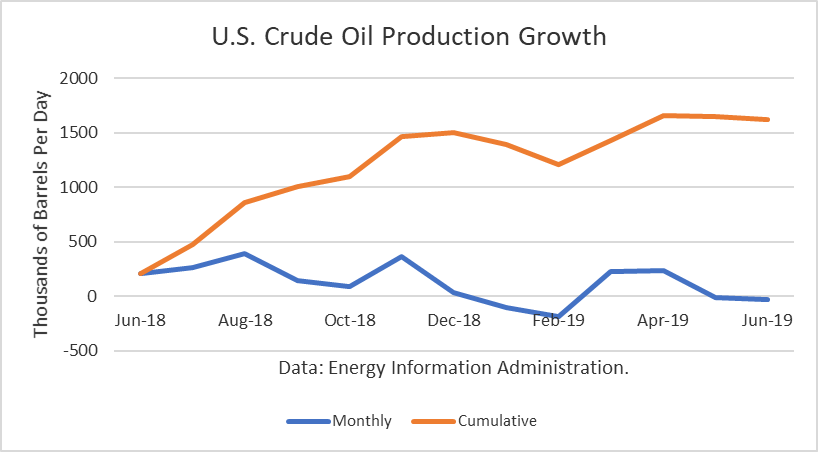

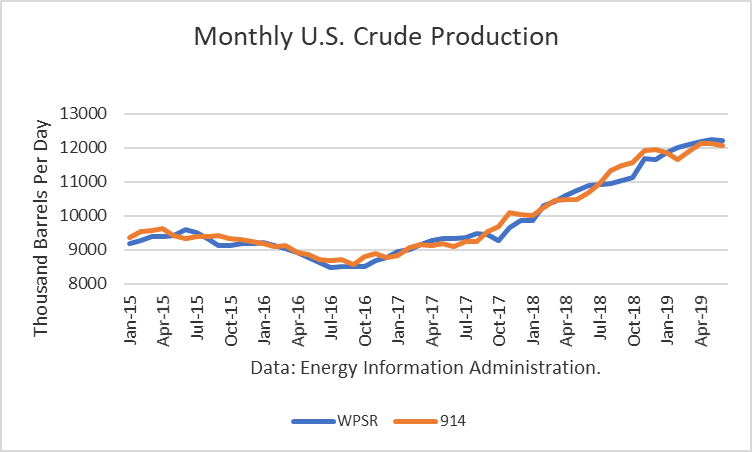

The Energy Information Administration reported that June crude oil production averaged 12.082 million barrels per day (mmbd), down 33,000 b/d from May. The drop resulted from a drop of 58,000 b/d in Oklahoma. Production gained the most in North Dakota (58,000) and Colorado (19,000) while production in Texas was only up 13,000 b/d.

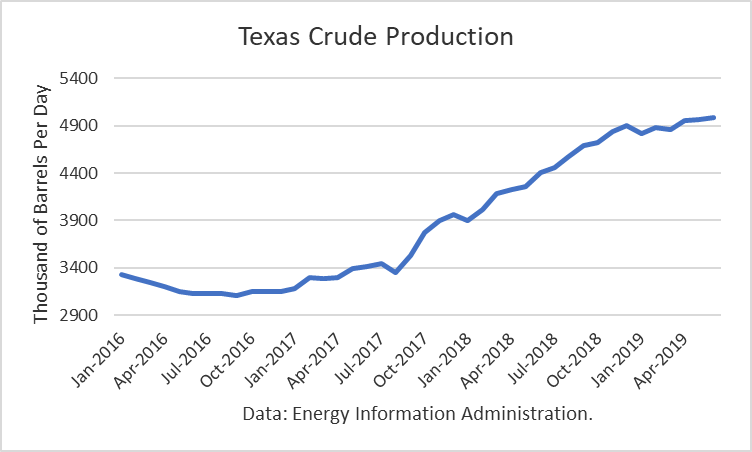

A pause in the growth rate in Texas had been expected due to pipeline constraints, which are expected to be alleviated in the second half of 2019 and first half of 2020. Nevertheless, Texas production reached a new all-time high of 4.982 mmbd.

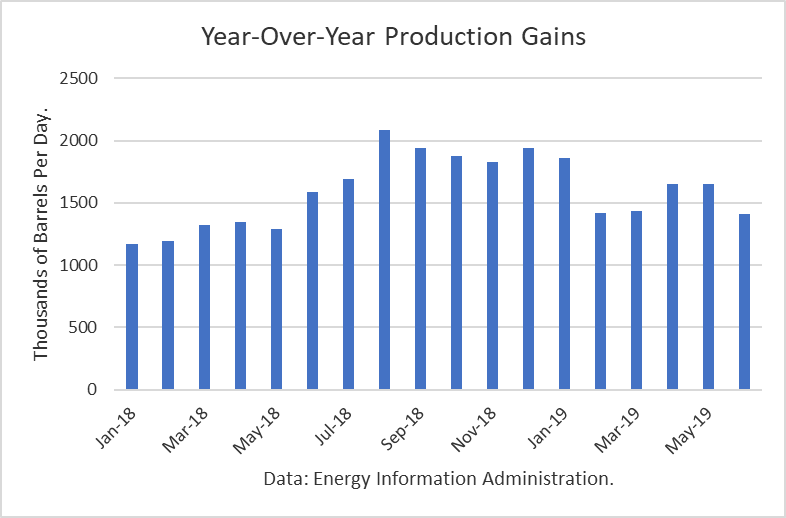

The year-over-year gains have been especially impressive with the June figure being 1.410 mmbd. And this number only includes crude oil. Other supplies (liquids) that are part of the petroleum supply add to that. For June, that additional gain is about 540,000 b/d.

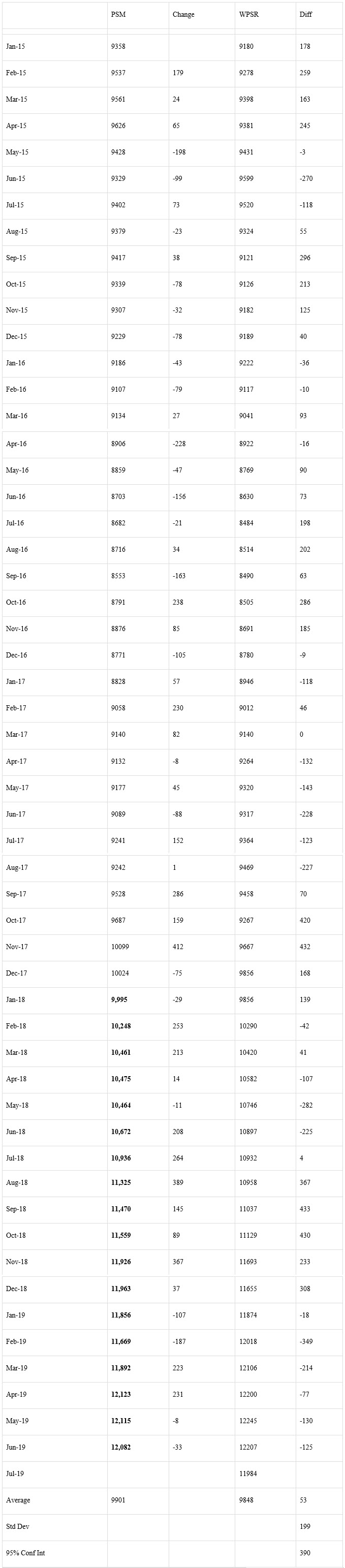

The EIA-914 Petroleum Supply Monthly (PSM) figure was 125,000 b/d lower than the weekly data reported by EIA in the Weekly Petroleum Supply Report (WPSR), averaged over the month, of 12.207 mmbd.

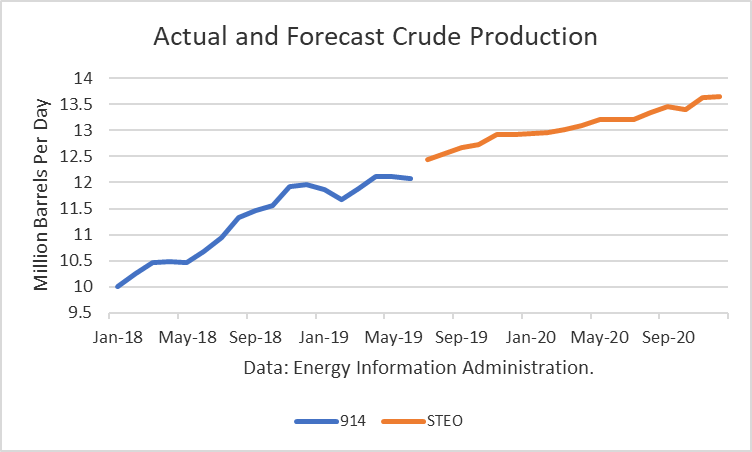

The June figure was about 60,000 b/d higher than 12.020 mmbd estimate for that month in the August Short-Term Outlook. That implies no need for another upward “rebenchmarking” to EIA’s model in future production levels at this time since the difference was not large enough to warrant it.

The EIA is projecting that 2019 production will exit the year at 12.95 mmbd. For 2020, the EIA is projecting an exit at 13.642 mmbd.

Permian Pipelines

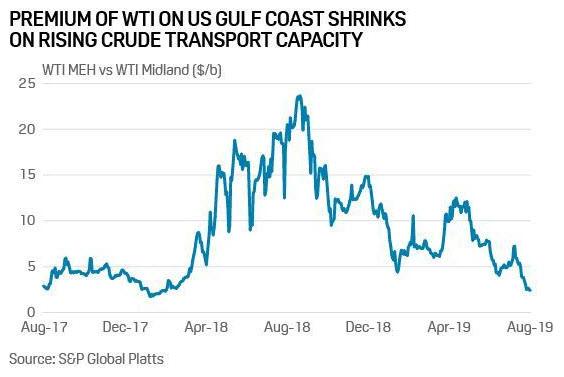

Two Permian crude oil pipelines have begun shipping oil to the Gulf Coast in the past two weeks, and a third is scheduled to begin shipments by year-end. Plains All American Pipeline LP’s (PAA) Cactus ll pipeline is expected to ship 300,000 b/d in August and to be at full capacity, 670,000 b/d, in September. EPIC Midstream’s crude oil pipeline began shipping 400,000 b/d. It is designed to ship 440,000 b/d from the Permian and another 150,000 b/d from the Eagle Ford.

Phillips 66 Partner’s Gray Oak pipeline is expected to ship an additional 900,000 b/d. It is scheduled to being shipments by year-end.

The effect of the pipeline additions will narrow the spread between Midland and the U.S. gulf prices, effectively lowering breakeven costs in the Permian.

Conclusions

The gain in crude production growth was stymied in the first half of 2019 due to constraints in takeaway capacity from the Permian Basin. However, the EIA just estimated U.S. production of 12.5 million barrels per day, and the outlook for the balance of 2019 and for 2020 is for renewed growth.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

I know you think that because of what some horizontal producers have said about efficiency gains (Hamm) that production will rise even given the fact that rigs are being laid down left and right. Hamm has to make statements like that to protect his stock price. They, meaning most everyone, are laying rigs down because they are losing money with oil at $50/b. Time will tell, but I think we may not even sniff that 12.95 exit rate. The 2020 predicted rate is a pipe dream unless prices improve dramatically.