How can you effectively run an options-based portfolio when trading with a small account? For example, how can you trade options on stocks like Tesla (TSLA), Ulta Beauty (ULTA), Apple (AAPL), Disney (DIS), Facebook (FB), etc., that possess such a high price per share when account balances are limited? People often shy away from options trading due to low account balances. However, limited capital doesn’t preclude you from trading, and in fact, you can run an effective options portfolio regardless of account size. Options enable you to leverage a minimal amount of capital, which opens the door to trading virtually any stock, all while defining your risk.

Over the past 13 months, ~315 trades have been made with a win rate of 86% and a premium capture of 57% across 69 different tickers. When stacked up against the S&P 500, an options strategy generated a return of 9.1% compared to the S&P 500 index, which returned 3.7% over the same period. These returns demonstrate the resilience of this high probability options trading in both bear and bull markets. Moreover, these results can be replicated irrespective of account size when following the fundamentals outlined below.

Myth Busting Small Account Limitations

Options can be leveraged, using small amounts of capital to trade what otherwise would require much greater capital requirements. How is this possible? It’s possible because options can be traded in a risk-defined manner. Therefore, entering any options trade, the required capital equals the maximum loss while the maximum gain equals the option premium income received. Since the risk-defined approach has a max loss, the required capital is equivalent to the max loss. The maximum loss value only needs to be covered by the available account balance. The aggregate price of the underlying shares within an option contract (contracts trade in 100 share blocks) is irrelevant.

The overall options-based portfolio strategy is to sell options that enable you to collect premium income in a high-probability manner while generating consistent income for steady portfolio appreciation regardless of market conditions. This is all done without predicting which way the market will move since options are a bet on where stocks won’t go, not where they will go. This options-based approach provides a margin of safety, mitigates drastic market moves, and contains portfolio volatility. This strategy is agnostic to account balance and applies to accounts of all sizes.

10 Option Trading Rules for Small Accounts

It’s noteworthy to point out that trading in small accounts limits the amount of room for errors; thus, a set of trading fundamentals must be followed to run an options-based portfolio successfully. Specifically, position-sizing, sector diversity, maximizing the number of trade occurrences, and risk-defined strategies are some notable areas that traders need to heed for long-term successful options trading not only in small accounts but in accounts of all sizes.

To effectively and successfully run an options-based portfolio over the long term, the following option trading fundamentals must be exercised in each and every trade. Violating any of these fundamentals will jeopardize this strategy and possibly negate the effectiveness of this approach on the whole. Below are 10 option trading rules for small accounts and accounts of all sizes but specifically small accounts as it pertains to risk-defined strategies when capital is limited.

-

1) Be an option seller to collect premium income while taking advantage of time decay

2) Set the probability of success (delta) in your favor (70%, 85%, etc.) to ensure a statistical edge

3) Manage winning trades by closing the trade and realizing profits early in the option lifecycle

4) Sell options in high IV Rank environments to extract rich premiums

5) Sell options on tickers that are liquid in the options market

6) Maximize the number of trades to allow the expected probabilities to play out

7) Appropriate position sizing/portfolio allocation to manage risk exposure

8) Sell options across tickers with ample sector diversity

9) Keeping an adequate amount of cash on hand (~25% - 40%)

10) Risk-defined trades (put spreads, call spreads, and iron condors)

Risk Defined Strategy

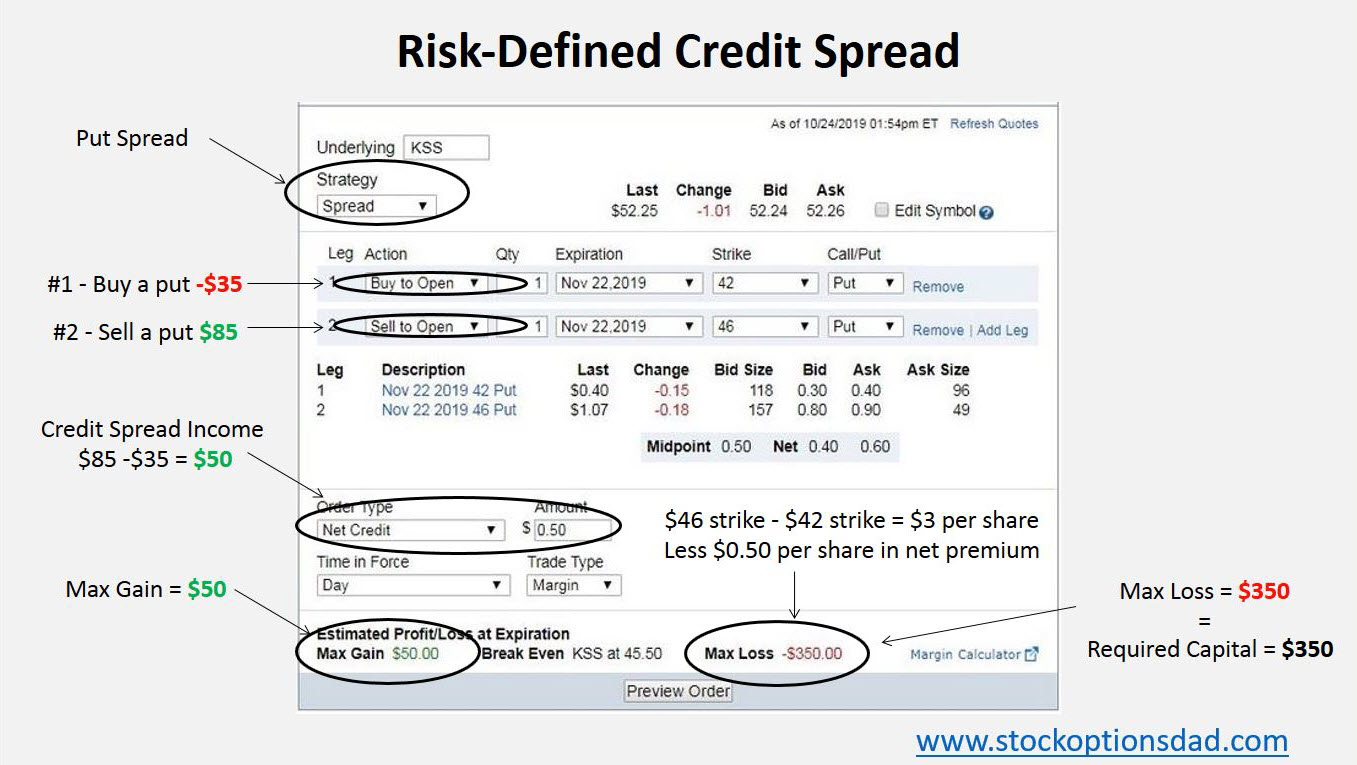

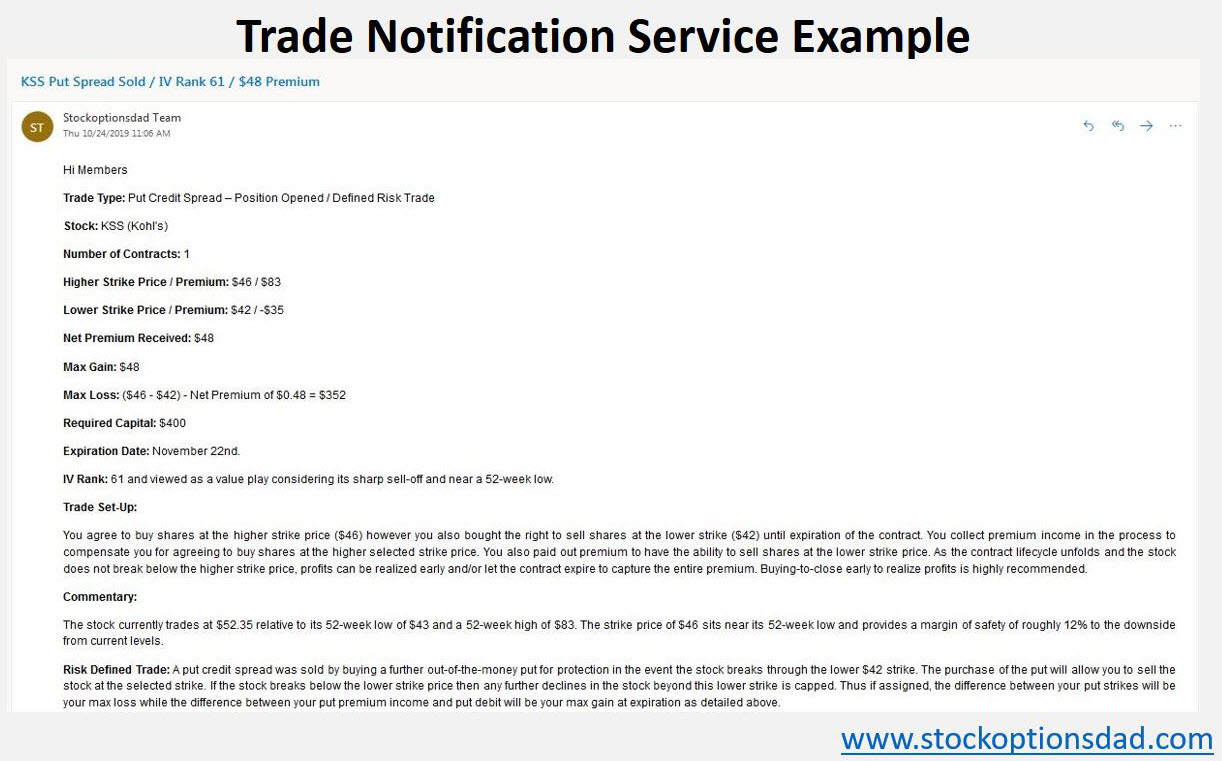

A credit spread is a type of options trade that risk-defines your trades and involves selling and buying an option. Let’s review a put spread as an example below.

Selling an option, you sell a put option, and you agree to buy shares at an agreed-upon price by an agreed-upon date in exchange for premium income.

Buying an option, you buy a put option using some of the premium received from selling the option above, and you now have the right to sell the shares at an agreed-upon price by the same agreed upon date in exchange for paying out a small premium.

Taken together, an option spread is where you sell an option and also buy a further-out-of-the-money option for downside protection. The difference in the premium received and premium paid out is the credit spread income collected.

For example, if you sell a put option at a strike price of $46 in exchange for $85 in premium, you can use some of that premium income to buy the $42 strike put option for $35 to net $50 on the trade ($85 - $35).

In this manner, you agree to buy shares at $46; you also have the right to sell shares at $42. This will cap your losses at $350 if the stock tanks since you would be assigned at $46 and exercise your right to sell shares at $43 per share less the net premium received of $50. The $4 per share loss is the max loss you can incur, and factor in the $50 of premium income, the net loss is capped at $350. The stock can drop to $0 per share, and your loss is still capped at $350 (Figures 1 and 2).

Figure 1 – Kohl’s example of a put spread generating $50 in net premium income while only requiring $350 of capital for the trade

Figure 2 – Example of the Kohl’s put spread

Maximizing Number of Trade Occurrences

Maximizing the number of trades is essential for any options-based strategy. Placing only 10 trades or 50 trades over a given time period is simply inadequate for an options-based approach. Instead, trading through all market conditions at a specific probability of success level, given enough trades and time, the probabilities will reach their expected outcomes. This maximizes the number of shots on goal. Over a long enough time period, these data will be smoothed out over the various market conditions to reach your expected probability of success. To achieve the expected probability level, hundreds of trades need to be placed and closed before the probabilities really begin to play out. As these trade data grow in size, plotting all of your trades over time, you’ll see the numbers align more and more with your expected probabilities. Taken together, trade as often as you can at your desired probability of success to achieve the win rate of interest (Figure 3).

Figure 3 – Dot plot summarizing ~315 trades over the previous 13-month period highlighting the importance of maximizing trades and trading through all market conditions

Position Sizing and Sector Allocation

Position sizing is critical, and being over-leveraged and assigned a losing trade can have a disproportionately negative impact on your portfolio and possibly negate all your successes. Restricting position sizing to ~5% or less of your overall portfolio will help to manage risk and contain unrealized losses. If and when positions move against you, maintaining a small position size will keep your risk profile in check. Trading across all sectors will ensure portfolio diversity and effective risk management as a result of the breath of uncorrelated stocks. Selling options across a wide array of tickers and sectors will safeguard your portfolio from any given sector downturn.

The Takeaway

Options trading allows one to profit without predicting which way the stock will move. Options trading isn’t about whether or not the stock will move up or down; it’s about the probability of the stock not moving up or down more than a specified amount. Options allow your portfolio to generate smooth and consistent income month after month for steady portfolio appreciation. Running an option-based portfolio offers a superior risk profile relative to a stock-based portfolio while providing a statistical edge to optimize favorable trade outcomes. Options trading is a long-term game that requires discipline, patience, time, maximizing the number of trade occurrences, and continuing to trade through all market conditions. Put simply; an options-based approach provides a margin of safety with a decreased risk profile while providing high-probability win rates. The basic building blocks of running an options-based portfolio includes appropriate position sizing, diversity of tickers (stocks and ETFs), diverse sector exposure, trading through all market environments, maximizing the number of trades, managing risk, options liquidity, taking profits early, and layering in risk defined trades.

Over the previous 13 months, the options-based approach outperformed the index by a wide margin (Figures 3 and 4). Over the previous 13 months, my win rate percentage was 86%. Over the same period, the options-based portfolio generated a 9.1% return relative to 3.7% for the S&P 500, outperforming the index by a wide margin (Figures 3 and 4).

Figure 4 – Options based portfolio return (9.1%) in comparison to the S&P 500 return (3.7%) over the past 13 months through both bear and bull market conditions. S&P 500 closed at $2,913.98 on September 30th, 2018, and closed at $3,022.55.74 as of October 28th, 2019

Conclusion

Account size does not preclude anyone from starting an options-based portfolio since the required capital is minimal. Selling option spreads is a great way to leverage a minimal amount of capital and define your risk. Maximizing the number of trade occurrences, position-sizing, diverse sector exposure, trading stocks and ETFs, managing winning trades, and risk-defined trades is essential for an options-based portfolio to succeed over the long term regardless of account size. In addition, options trading allows one to profit without predicting which way the stock will move to allow your portfolio to generate smooth and consistent income month after month since options are a bet on where stocks won’t go, not where they will go.

Selling options with a favorable risk profile and a high probability of success is the key. Options provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves. For example, I’ve demonstrated an 86% options win rate over the previous 12 months through both bull and bear markets while outperforming the S&P 500 over the same period by a wide margin producing a 9.1% return against a 3.7% for the S&P 500 with a lower risk profile. Taken together, options trading is a long game that requires discipline, patience, time, maximizing the number of trade occurrences, and continuing to trade through all market conditions with the probability of success in your favor.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares in AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY and USO. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.

Noah, could you explain the IV Rank metric for this novice. Thanks

Hi Dean

No problem, basically each stock has a historic implied volatility (IV) range, say the range is 30-60 over the past year. A low of 30 and a high of 60. Based on that, future volatility is predicted by the options market activity. It's been determined that predicted volatility is almost always over-estimated (the stock fails to be as volatile as predicted). When the predicted volatility approaches it's historic max is when implied volatility (IV) rank is high (i.e. how it's current IV "ranks" in relation to its historic range). When this value is high, option premiums are rich and time decay as a function of IV collapsing is rapid. If the current IV value is say 45 then this would equate to a rank of 50 since it's in the middle of the range. I've closed option contracts in days many times before.

Calculation: (current IV - 52-week IV low) / (52-week IV high - 52-week IV low)

I have YouTube videos and examples on my site as well: https://www.stockoptionsdad.com/

Vertical spreads don't take much advantage of time decay. The options tend to have about the same theta, which tells you what the time decay is, so the time decay on the two are similar, where the short option decays in your favor and the long option decays against you. Calendar spreads might be a better mechanism if you want to take advantage of time decay. You sell an option that has a couple of weeks left for maximum time decay. You buy an option that has many months left. This allows you to have maybe 3 times the time decay on the short option. Selling cash secured puts allows one to take full advantage of time decay.

Hi Brad

Thanks for the comment! The focus here is to educate readers on how to leverage small accounts with defined risk without the nuances of more complex options strategies. IV Rank is a better metric that will accelerate time decay due to the fact that implied volatility is high and when the stock fails to live up to that volatility expectation, the time premium falls rapidly and you can profits early. I sell a lot of cash covered puts however put spreads are nice since I can use much less capital and only take a small hit on the premium received.