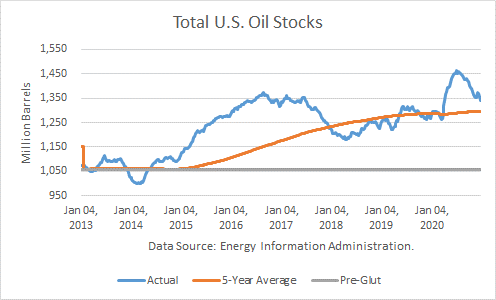

According to the Energy Information Administration, U.S. oil inventories (excluding SPR) fell by 14.9 million barrels last week to 1.342 billion, and SPR stocks were unchanged last week. Total stocks stand 47 mmb above the rising, rolling 5-year average and about 81.0 mmb higher than a year ago. Comparing total inventories to the pre-glut average (end-2014), stocks are 283 mmb above that average.

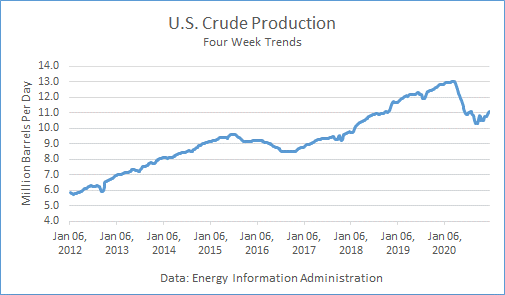

Crude Production

Production averaged 11.0 mmbd last week, unchanged from the prior week. It averaged 11.025 mmbd over the past 4 weeks, off 14.25 % v. a year ago. In the year-to-date, crude production averaged 11.504 mmbd, off 6.5 % v. last year, over 600,000 b/d lower.

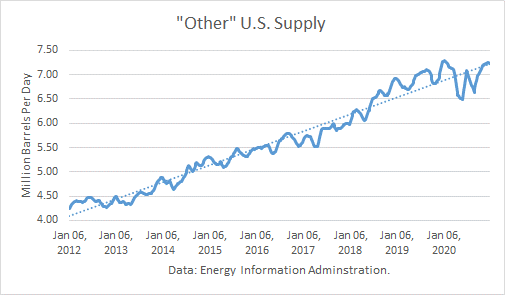

Other Supply

I have previously noted in an article how the “Other Supply,” primarily natural gas liquids and renewables, are integral to petroleum supply. The EIA reported that it fell by 24,000 b/d v. last week to 7.195 mmbd. The 4-week trend in “Other Supply” averaged 7.221 mmbd, off 0.5 % from the same weeks last year. In YTD, they are up 0.5 % from 2019.

Crude production plus other supplies averaged 18.280 mmbd over the past 4 weeks, far below the all-time-high record of 20.213 mmbd.

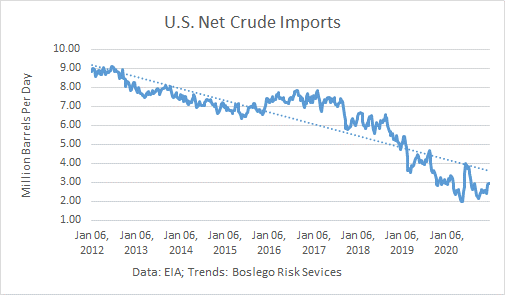

Crude Imports

Total crude imports fell by 238,000 mb/d last week to average 5.326 mmbd last week. This figure was below the 4-week trend of 5.396 mmbd, which in turn was off 14.4 % from a year ago.

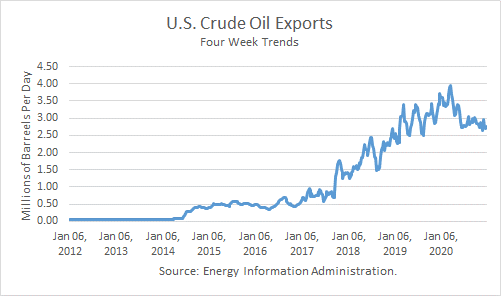

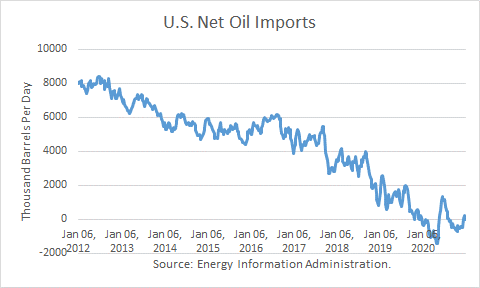

Net crude imports fell by 248,000 b/d because exports rose by 526,000 b/d to average 3.625 mmbd. Over the past 4 weeks, crude exports averaged 2.796 mmbd, 24.9 % lower than a year ago.

U.S. crude imports from Saudi Arabia fell by 79,000 b/d last week to average 118,000 b/d. Over the past 4 weeks, Saudi imports have averaged 167,000 b/d, down 62.0 % from a year ago.

Learn What the Most Successful Players Use to Trade Futures

Whether a trading novice or experienced professional, our Intro to Technical Analysis Guide will give you a clear advantage in today's fast-moving markets.

This 30+page FREE resource is designed to give you a head start in learning the basics of various TA tools and techniques. Numerous charts and descriptions fill this guide and offer the reader a quick way to get up to speed in this skillset.

Crude imports from Canada rose by 8,000 b/d last week, averaging 3.212 mmbd. Imports over the past 4 weeks averaged 3.484 mmbd, down 5.3 % v. a year ago.

Net oil exports averaged 292,000 b/d over the past 4 weeks. That compares to net oil exports of 305,000 mb/d over the same weeks last year.

Crude Inputs to Refineries

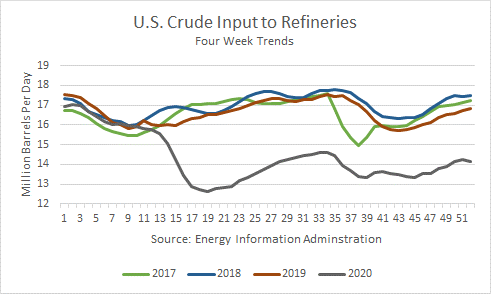

Inputs rose by 273,000 b/d last week averaging 14.287 mmbd. Over the past 4 weeks, crude inputs averaged 14.230 mmbd, off 15.6 % v. a year ago. In the year-to-date, inputs averaged 14.249 mmbd, off 14.2 % v. a year ago.

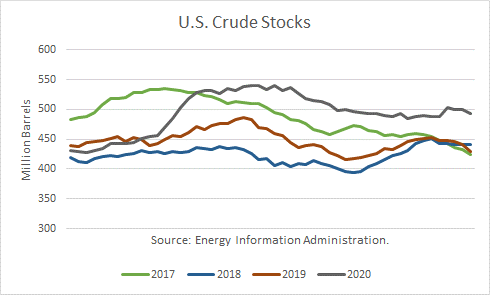

Crude Stocks

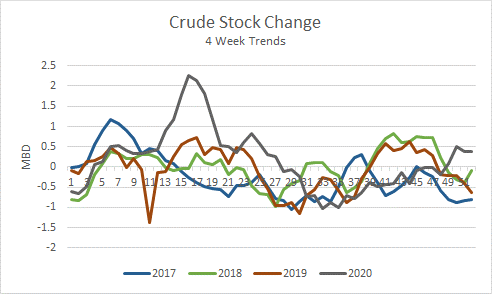

Over the past 4 weeks, crude oil supply exceeded demand by 382,000 mb/d.

Commercial crude stocks 493.5 mmb are now 63.6 million barrels higher than a year ago.

Petroleum Products

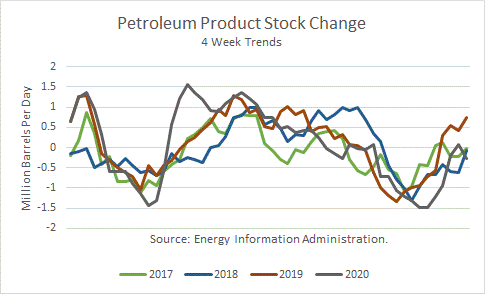

Given the recent net product stock draws, product demand has exceeded supply by 273,000 mb/d.

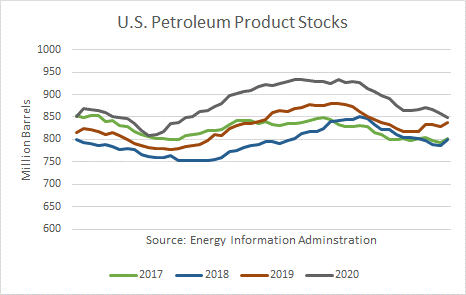

Total U.S. petroleum product stocks at 849 mmb are 11 million barrels higher than a year ago.

Product exports fell by 58,000 mmb/d last week, averaging 5.656 mmbd. The 4-week trend of 5.266 mmbd is off 3.9 % from a year ago. In the year-to-date, exports averaged 5.034 mmbd, off 1.8 % from a year ago.

Demand

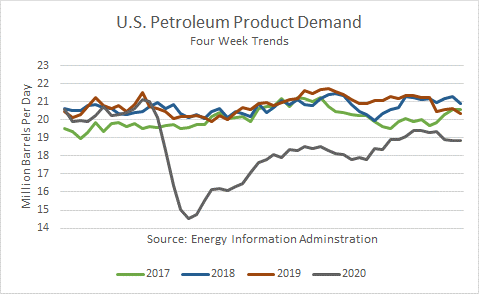

Total petroleum demand averaged 19.068 mmbd over the past 4 weeks, off 6.4 % v last year. In the YTD, product demand averaged 18.343 mmbd, off 12.0 % v. the same period in 2019.

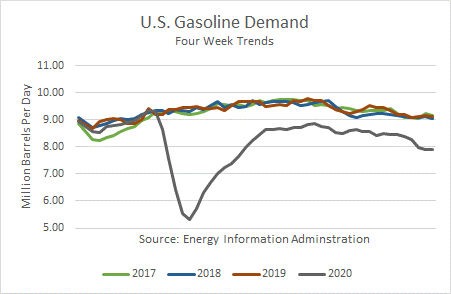

Gasoline demand at the primary stock level fell by 833,000 b/d last week and averaged 7.931 mmbd over the past 4 weeks, off 13.2 % v. the same weeks last year. In the YTD, it reported that gas demand is off 12.8 % v. a year ago.

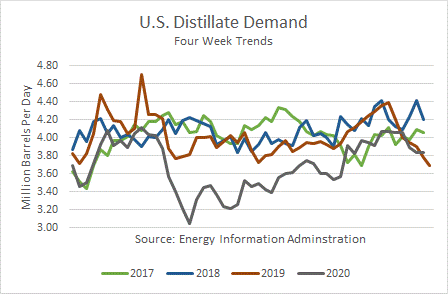

Distillate fuel demand, which includes diesel fuel and heating oil, rose by 539,000 b/d last week, and averaged 3.790 mmbd over the past 4 weeks, up 0.3 % the same weeks last year. In the YTD, demand is off 8.1 % v. a year ago.

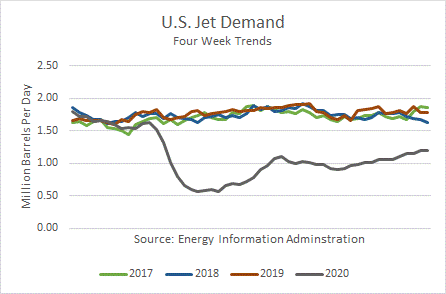

Jet fuel demand is off 31.8 % over the past 4 weeks v. last year. In the year-to-date, demand was off 39.5 % v. 2019.

Product Stocks

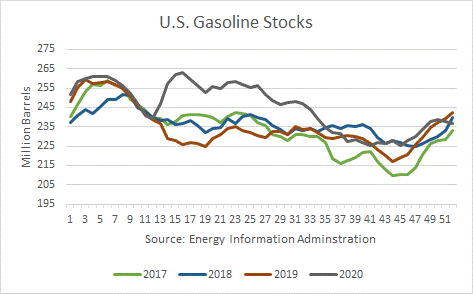

Gasoline stocks are now 5.9 mmb lower than a year ago, ending at 236.6 mmb.

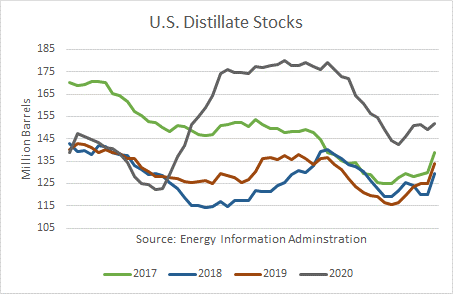

Distillate stocks are 18.3 mmb higher than a year ago, ending at 152.0 mmb.

Conclusions

As perhaps the most eventful year in modern petroleum history comes to a close, we find U.S. petroleum demand still struggling to recover. Even the intro of a vaccine and promises of economic help have yet to stem the majority of the demand loss.

Petroleum product stocks have corrected but crude stocks remain stubbornly high. Low refinery runs have contributed.

The worst of this saga appears over. But the future may be changed forever.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.