The Energy Information Administration released its Short-Term Energy Outlook for January, and it shows that OECD oil inventories likely bottomed in this cycle in June 2018 at 2.802 billion barrels. Stocks peaked at 3.210 billion in July 2020. In December 2020, it estimated stocks dropped by 40 million barrels to end at 3.061 billion, 172 million barrels higher than a year ago.

The EIA estimated global oil production at 93.45 million barrels per day (mmbd) for November, compared to global oil consumption of 95.59 mmbd. That implies an undersupply of 2.14 mmbd or 64 million barrels for the month. About 30 million barrels of the draw for November is attributable to non-OECD stocks.

For 2020, OECD inventories are now projected to build by net 127 million barrels to 3.006 billion. For 2021 it forecasts that stocks will draw by 95 million barrels to end the year at 2.910 billion.

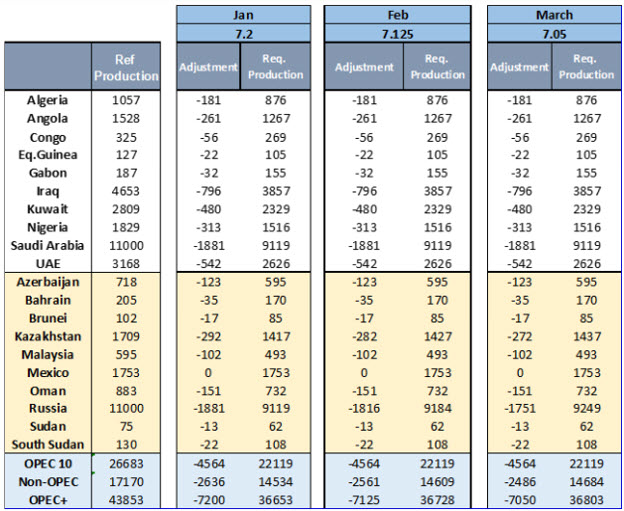

The EIA forecast was made incorporates the OPEC+ decision to cut production and exports. According to OPEC’s press release on January 5, 2021:

“The Meeting acknowledged the need to gradually return 2 mb/d to the market, with the pace being determined according to market conditions. It reconfirmed the decision made at the 12th ONOMM to increase production by 0.5 mb/d starting in January 2021, and adjusting the production reduction from 7.7 mb/d to 7.2 mb/d.”

The adjustments to the production level for February and March 2021 will be implemented as per the distribution detailed in the table below.

The EIA has assumed the following OPEC production levels for its STEO:

Oil Price Implications

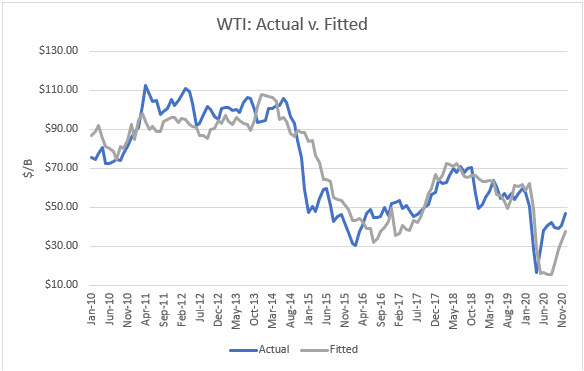

I updated my linear regression between OECD oil inventories and WTI crude oil prices for the period 2010 through 2020. As expected, there are periods where the price deviates greatly from the regression model. But overall, the model provides a reasonably high r-square result of 82 percent.

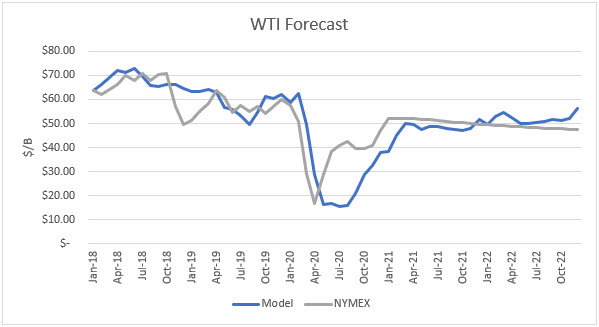

I used the model to assess WTI oil prices for the EIA forecast period through 2021 and 2022 and compared the regression equation forecast to actual NYMEX futures prices as of January 22. The result is that oil futures prices are presently undervalued through the forecast horizon in 2022.

Uncertainties

April 2020 proved that oil prices can move dramatically based on market expectations and that they can drop far below the model’s valuations, whereas prices in May through December proved that the market factors-in future expectations beyond current inventory levels.

The most important uncertainty is how deeply and how long the coronavirus will disrupt the U.S. and world economies. The announcements of vaccines and economic stimulus lends credibility that a recovery is in store for some time in 2021.

But what kind of recovery will it be? How much of business and daily life will be altered for the longer-term? Online meetings instead of face-to-face meetings, work-from-home, and other such changes may alter petroleum demand patterns long-term.

Conclusions

OPEC has contained production more effectively than usual. Saudi Arabia decided to act unilaterally to protect its interests.

Equally, on the supply side, the transition away from fossil fuels has taken a big leap forward in 2020, with the major oil companies announcing investment shifts. The petroleum era is coming to a close, at least in terms of sustained growth as the energy transition moves along.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.