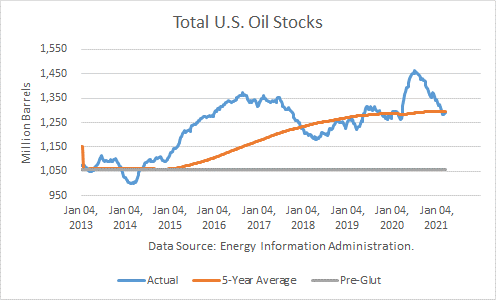

According to the Energy Information Administration, U.S. petroleum inventories (excluding SPR) rose by 4.8 million barrels last week to 1.292 billion, and SPR stocks were unchanged. Total stocks stand 2 mmb below the rising, rolling 5-year average and 31.4 mmb higher than a year ago. Comparing total inventories to the pre-glut average (end-2014), stocks are 233 mmb above that average.

Crude Production

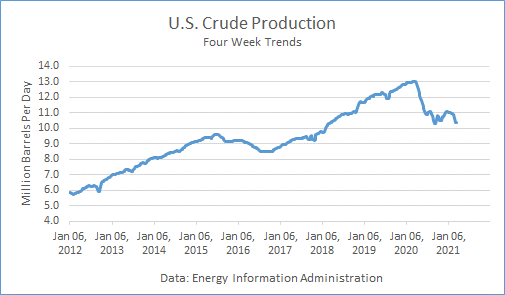

Production averaged 11.0 mmbd last week, up 100,000 b/d from the prior week. It averaged 10.700 mmbd over the past 4 weeks, off 18.0 % v. a year ago. In the year-to-date, crude production averaged 10.736 mmbd, off 17.5 % v. last year, about 2.3 mmb/d lower

Other Supply

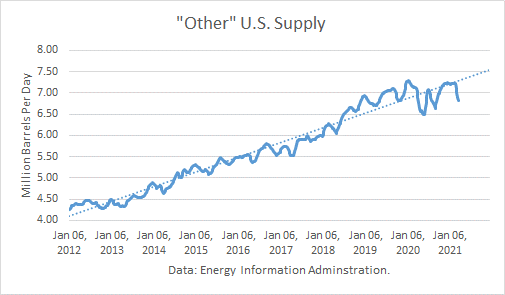

I have previously noted in an article how the “Other Supply,” primarily natural gas liquids and renewables, are integral to petroleum supply. The EIA reported that it rose by 13,000 b/d v. last week to 6.914 mmbd. The 4-week trend in “Other Supply” averaged 6.856 mmbd, off 3.4 % from the same weeks last year. In YTD, they are off 1.5 % from 2020.

Crude production plus other supplies averaged 17.196 mmbd over the past 4 weeks, far below the all-time-high record of 20.213 mmbd.

Crude Imports

Total crude imports rose by 299,000 b/d last week to average 5.622 mmbd last week. This figure was below the 4-week trend of 5.723 mmbd, which in turn was off 9.5 % from a year ago.

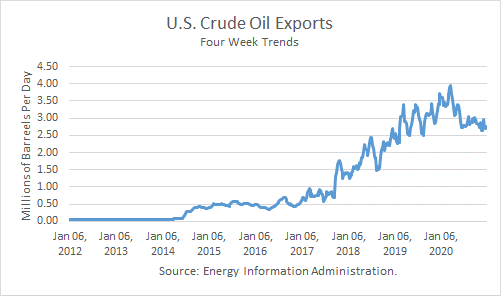

Net crude imports rose by 338,000 b/d because exports fell by 39,000 b/d to average 2.481 mmbd. Over the past 4 weeks, crude exports averaged 2.496 mmbd, 6.8 % lower than a year ago.

U.S. crude imports from Saudi Arabia fell by 28,000 b/d last week to average 280,000 b/d. Over the past 4 weeks, Saudi imports have averaged 302,000 b/d, down 34.8 % from a year ago.

Crude imports from Canada fell by 30,000 b/d last week, averaging 3.418 mmbd. Imports over the past 4 weeks averaged 3.537 mmbd, off 1.9 % v. a year ago.

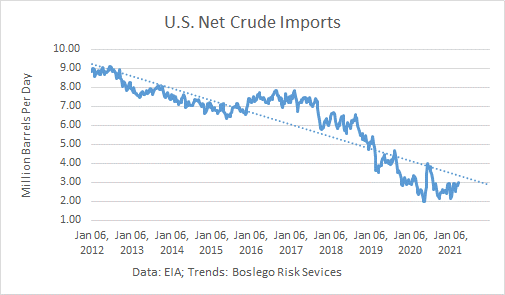

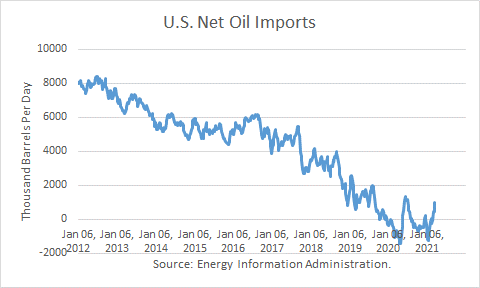

Net oil imports averaged 1.253 mmb/d over the past 4 weeks. That compares to net oil exports of 1.022 mmb/d over the same weeks last year.

Crude Inputs to Refineries

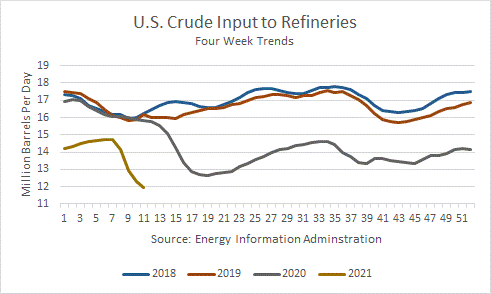

Inputs rose 957,000 b/d last week last week averaging 14.389 mmbd. Over the past 4 weeks, crude inputs averaged 12.509 mmbd, off 20.6 % v. a year ago. In the year-to-date, inputs averaged 13.695 mmbd, off 15.0 % v. a year ago.

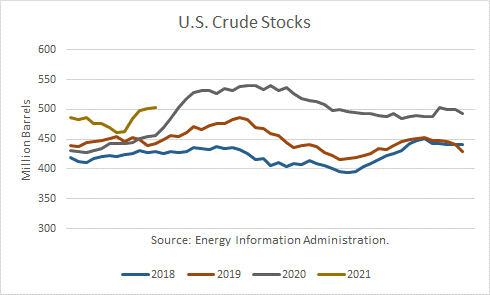

Crude Stocks

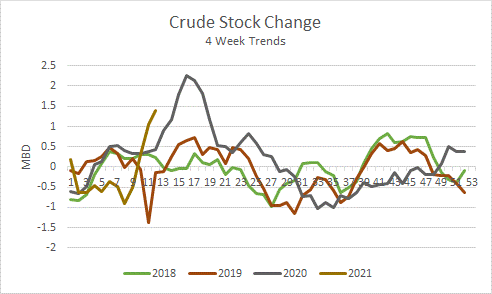

Over the past 4 weeks, crude oil supply exceeded demand by 1.394 mmb/d.

Commercial crude stocks 502.7 mmb are now 47.4 million barrels higher than a year ago.

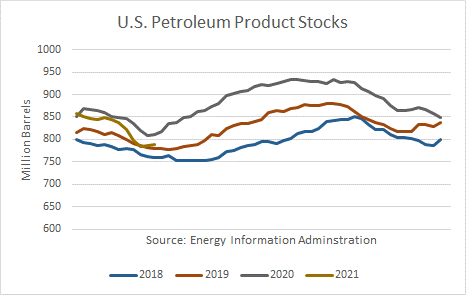

Petroleum Products

Given the recent net product stock draws, product demand has exceeded supply by 1.812 mmb/d.

Total U.S. petroleum product stocks at 789 mmb are 21 million barrels lower than a year ago.

Product exports rose by 895,000 mmb/d last week, averaging 5.222 mmbd. The 4-week trend of 4.445 mmbd is off 20.3 % from a year ago. In the year-to-date, exports averaged 4.780 mmbd, off 13.3 % from a year ago.

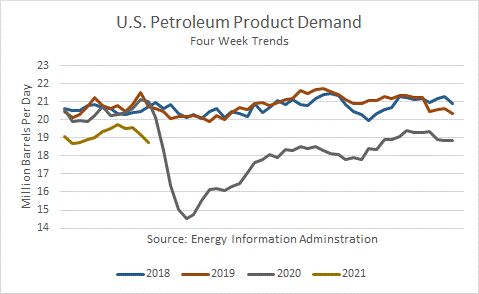

Demand

Total petroleum demand averaged 18.766 mmbd over the past 4 weeks, off 10.7 % v last year. In the YTD, product demand averaged 19.278 mmbd, off 5.8 % v. the same period in 2020.

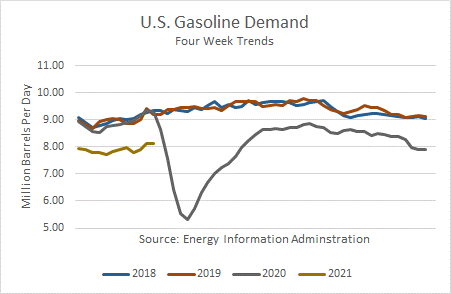

Gasoline demand at the primary stock level rose by 231,000 b/d last week and averaged 8.483 mmbd over the past 4 weeks, off 8.7 % v. the same weeks last year. In the YTD, it reported that gas demand is off 10.1 % v. a year ago.

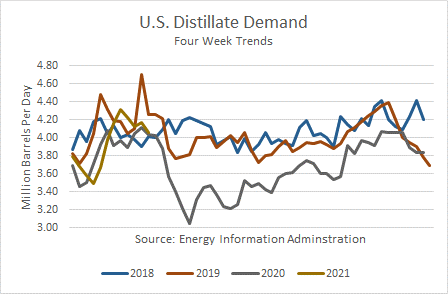

Distillate fuel demand, which includes diesel fuel and heating oil, fell by 436,000 b/d last week, and averaged 3.974 mmbd over the past 4 weeks, off 1.4 % the same weeks last year. In the YTD, demand is up by 2.8 % v. a year ago.

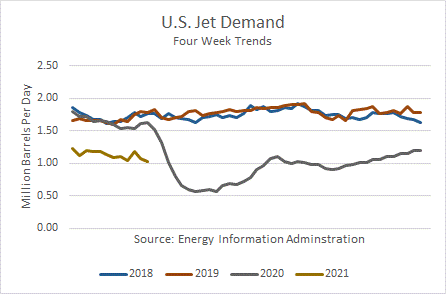

Jet fuel demand is off 35.4 % over the past 4 weeks v. last year. In the year-to-date, demand was off 30.9 % v. 2019.

Product Stocks

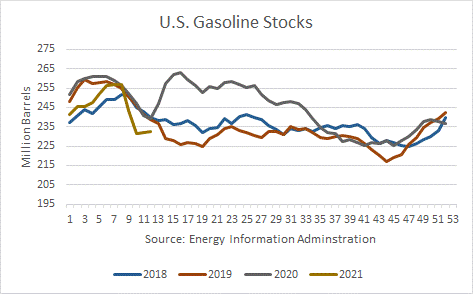

Gasoline stocks are now 7.0 mmb lower than a year ago, ending at 232.3 mmb.

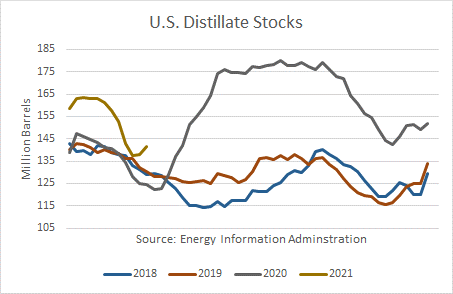

Distillate stocks are 17.1 mmb higher than a year ago, ending at 141.6 mmb.

Conclusions

The correction in crude v. petroleum product supplies continued. Crude stocks have a sizable surplus v. last year, whereas products have a deficit.

Product demand has not responded much to changes in pandemic conditions, in which retail businesses can operate more fully. There are no indications that demand will return to pre-pandemic levels in the foreseeable future.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.