It’s been a roller coaster ride of a year for investors, with the S&P-500 (SPY) finding itself down more than 20% year-to-date in one of its worst starts ever before clawing back following a slight deceleration in CPI sequentially (8.5% vs. 9.1%).

One of the hardest hit groups this year has been the Retail Sector (XRT), with a considerable portion of the sector suffering when consumers adjust their spending habits.

While this has led to some investors steering clear of the sector, some names tilt more towards staples than their peers, like Walmart (WMT), and some discretionary names have seen large enough corrections that a harder-than-expected landing for the economy looks mostly priced in.

One stock that fits the second bill is American Eagle Outfitters (AEO), which is down over 65% from last year’s highs even after its recent rally.

While I wouldn’t be in a rush to buy either name with the market short-term extended, I believe they belong at the top of one’s watchlist if they pull back towards support. Let’s take a look below:

Walmart (WMT)

Walmart released its fiscal Q2 2023 results this week, trouncing estimates with revenue of $152.9BB, up 8% year-over-year after a much stronger second half of Q2 than planned.

While this didn’t lead to any improvement in quarterly earnings per share, which dipped 1% year-over-year ($1.77 vs. $1.78), this was partially due to markdowns taken to reduce inventory levels in areas where it had risks like apparel.

Given the better-than-expected Q2 results, the company is now more upbeat about its fiscal Q3 performance, especially as it enters the period with cleaner inventory and as some consumers look to trade down, hit by rising fuel costs and mortgage rates.

Walmart’s positioning as a beneficiary of trading down is a big deal, but it won't be immune to a weak economic environment. However, it could see migration from premium retailers to lessen the blow.

It also continues to see solid growth in its Walmart+ memberships, providing some insulation as less affluent customers curtail spending in some of its discretionary segments.

This tailwind from growth in Walmart+ and its heavy staples weighting makes WMT a name to own.

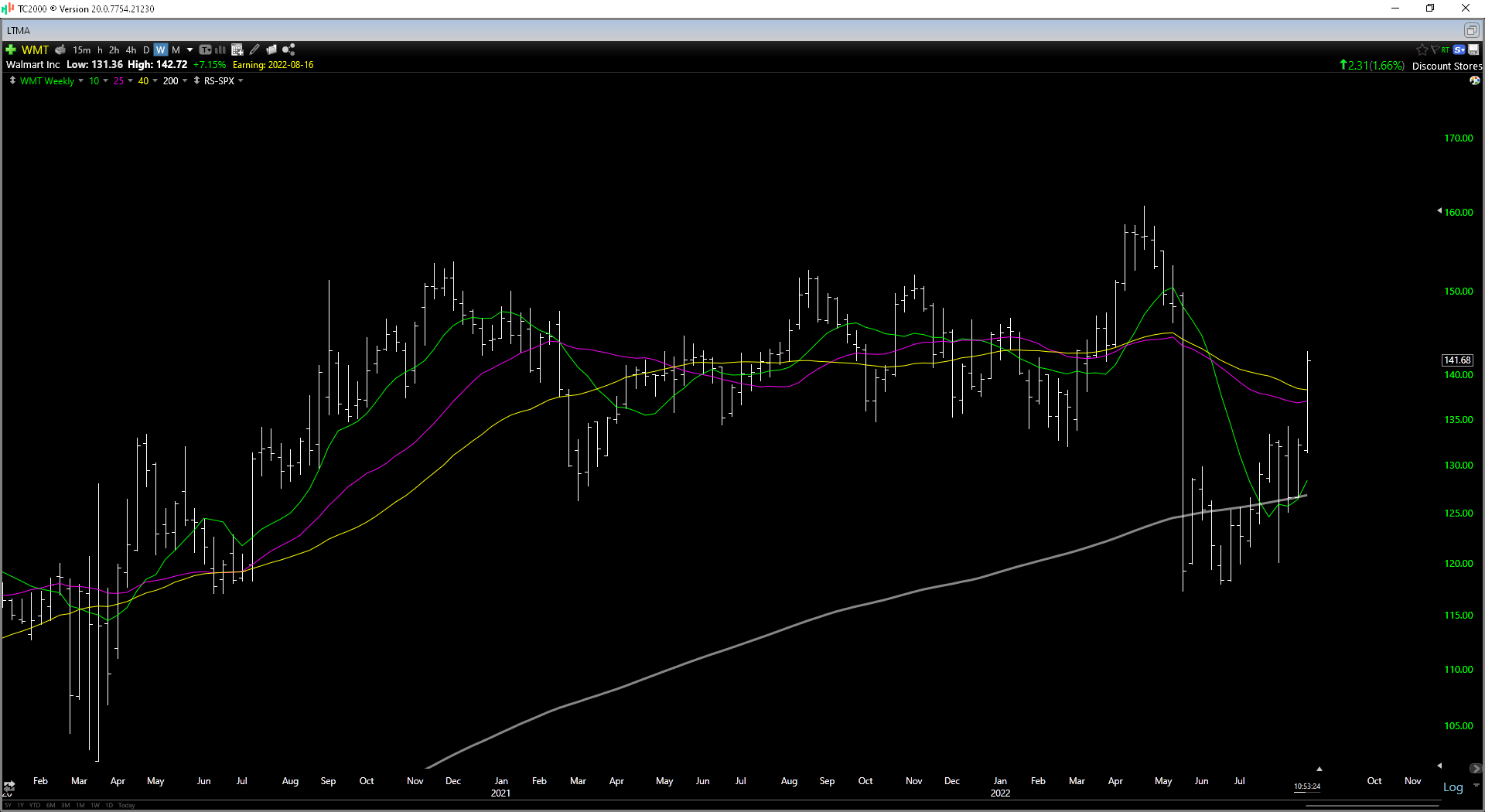

Looking at the chart above, we can see that WMT has historically traded at 20.1x earnings (10-year average), and the stock is currently trading at ~21.7x earnings at a share price of $141.00.

This is a premium to its historical multiple, but it was during a period when Walmart struggled to grow annual EPS (2023 estimates: $5.70 vs. $5.02 in FY2023.

However, looking ahead, WMT is expected to see an acceleration in its growth rate, with annual EPS estimates sitting at $6.50 in FY2024 and $7.16 in FY2025, with its earnings growth rate expected to come in at 14% in FY2024 and 10% in FY2025.

This should command a higher earnings multiple of 26, translating to a fair value of $169.00, pointing to a 20% upside from current levels.

While this might not seem like much upside, Walmart has a much lower beta than the market and an attractive dividend yield of 1.70%, making it a nice defensive play for investors looking to maintain exposure to the market but with lower risk.

That said, I prefer a minimum 25% upside to fair value to justify starting new positions.

So, while I think WMT is a name to own in Q3 and Q4 in a weaker economic environment, I see the low-risk buy zone for the stock coming in at $135.00 or lower, suggesting the better move is to buy on dips vs. rush in above $141.00.

This would coincide with a pullback to its rising 25-week moving average (pink line), which will likely provide support during any pullbacks now that it’s been reclaimed.

American Eagle Outfitters (AEO)

Unlike Walmart, which just came off a surprisingly strong report, American Eagle’s Q1 2022 report in May was a stinker. This was partially due to difficult year-over-year comps after lapping government stimulus and a wardrobe refresh in Q1, but it was also self-inflicted.

The issue was that the company came into the year with a more bullish outlook than it should have been, not considering the possibility of weaker demand in a more difficult economic environment.

Due to this misfire, the company exited the quarter with much higher inventory than planned (also impacted by a colder Q1 that hurt swimwear sales). It will now have to shed some of its inventory, resulting in weaker than expected margins as it ensures it has a fresh fall line-up.

That said, its Aerie business had another strong quarter, up 8% vs. difficult comps in Q1, and this segment is now sporting a 27% three-year revenue CAGR, easily offsetting the softness in the American Eagle segment.

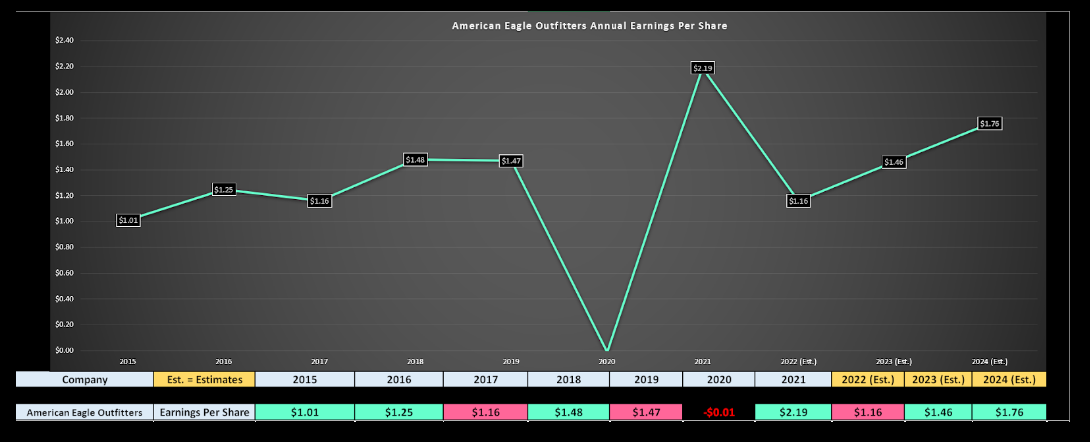

However, as the earnings trend shows below, we’re expected to see a plunge in annual earnings per share [EPS] related to clearing through spring goods, higher freight costs, and higher store wages.

So, even if American Eagle meets current annual EPS estimates, it will see annual EPS tumble to $1.16, down from $2.19 in FY2021, a 47% decline year-over-year.

While this is a terrible-looking earnings trend, it is worth noting that annual EPS should rebound in FY2023 and FY2024 as freight costs should moderate, and American Eagle should see some benefit from its Quiet Logistics acquisition.

So, while an ugly Q2 report is on deck and the company is up against clear headwinds from a weaker consumer, there is a light at the end of the tunnel with earnings set to rebound sharply.

Besides, while the short-term outlook isn’t as pretty, the stock is now priced at its most attractive levels in years.

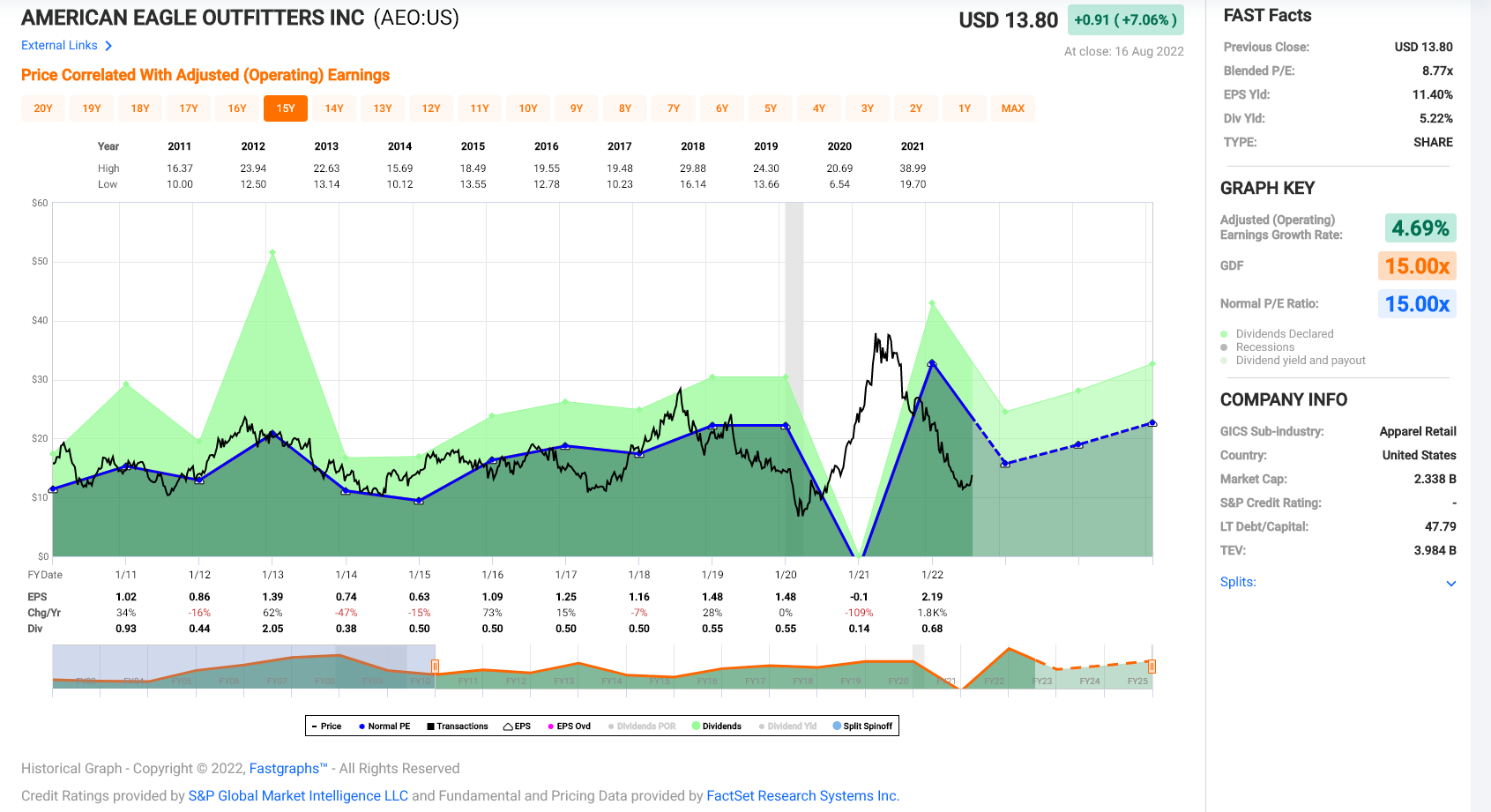

American Eagle has historically traded at 15.0x earnings (15-year average) and is currently sitting at just 9.0x forward earnings at a share price of $13.20 (FY2023 estimates: $1.46).

This is a dirt-cheap valuation for the stock. Even if we assume a more conservative multiple in a recessionary environment that doesn’t favor consumer discretionary names, I see a fair value for the stock of $17.52 per share (12x FY2023 estimates).

So, with a 33% upside to fair value, I would expect any pullbacks to provide buying opportunities.

Looking at the weekly chart, we see that AEO remains in a downtrend but is just above a multi-year support zone at $11.00 per share.

This reinforces my view that the negativity is priced in and that we’re sitting near a lower-risk buy point. Hence, any retracements below $12.60 should provide buying opportunities.

American Eagle and Walmart may not be the most exciting ideas and certainly don’t have nearly the growth rates of high-flying stocks like Celcius Holdings (CELH). Still, both stocks offer attractive dividend yields (5.2% and 1.7%, respectively) and look to have found bottoms after multi-month downtrends.

So, for investors looking to add long exposure at reasonable valuations, I see WMT and AEO as attractive, with buy zones of $135.00 and $12.60, respectively.

Taylor Dart

INO.com Contributor

Disclaimer: This article is the opinion of the contributor themselves. Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing.