Introduction

CVS Health Corporation (NYSE:CVS) has just capped off a fantastic 2015 performance in several metrics (EPS growth, revenue, dividends, share buybacks and acquisitions) that drive shareholder value. As 2016 begins, CVS presents a compelling investment opportunity in the healthcare space. This premise is based on the fact that CVS has been highly acquisitive, continues to deliver robust growth, growing its dividends over time and has an aggressive share buyback program. CVS recently reported a record year in 2015 and continues to drive and position itself for long-term success. With its recent acquisitions and partnerships, specifically, the acquisition Target’s pharmacies and Omnicare will significantly expand its footprint and ability to dispense prescriptions to the general public and in assisted living and long-term care facilities that serve the senior patient population. As the United States continues to absorb an aging population alongside growing overall healthcare costs, more specifically prescription drug costs, CVS looks poised to benefit and continue to outperform the broader market. The most recent earnings report, a record year in 2015 with its rise in its 2016 outlook and a 21% boost in its dividend payout underscores this premise. I content that CVS will continue to deliver continued growth and positioning for long-term success to drive shareholder value.

CVS Delivered A Fantastic 2015

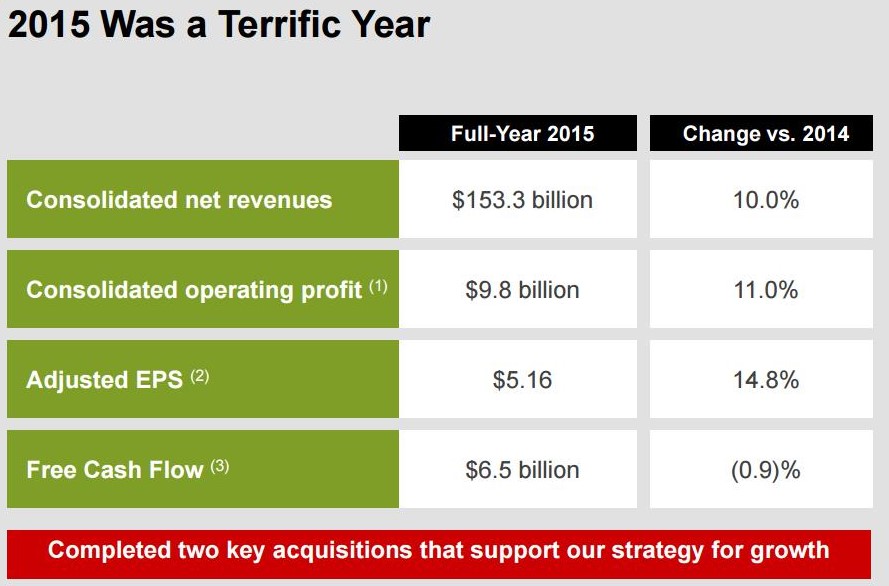

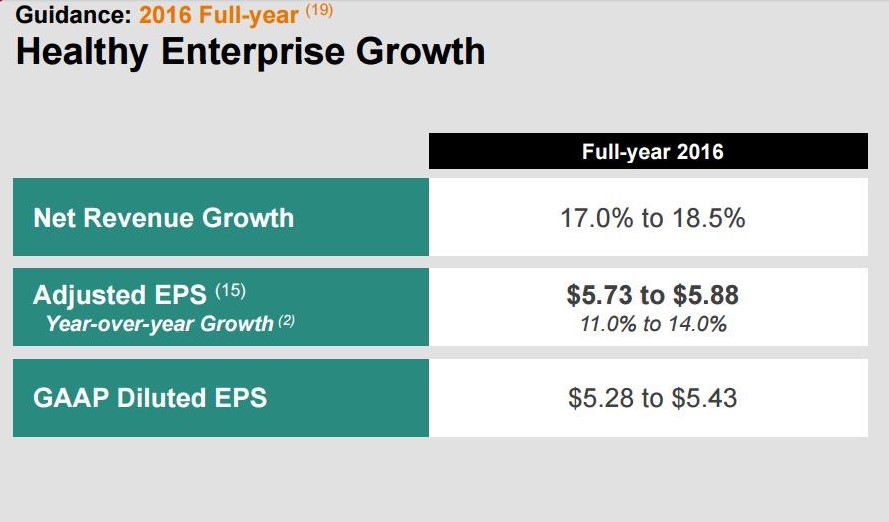

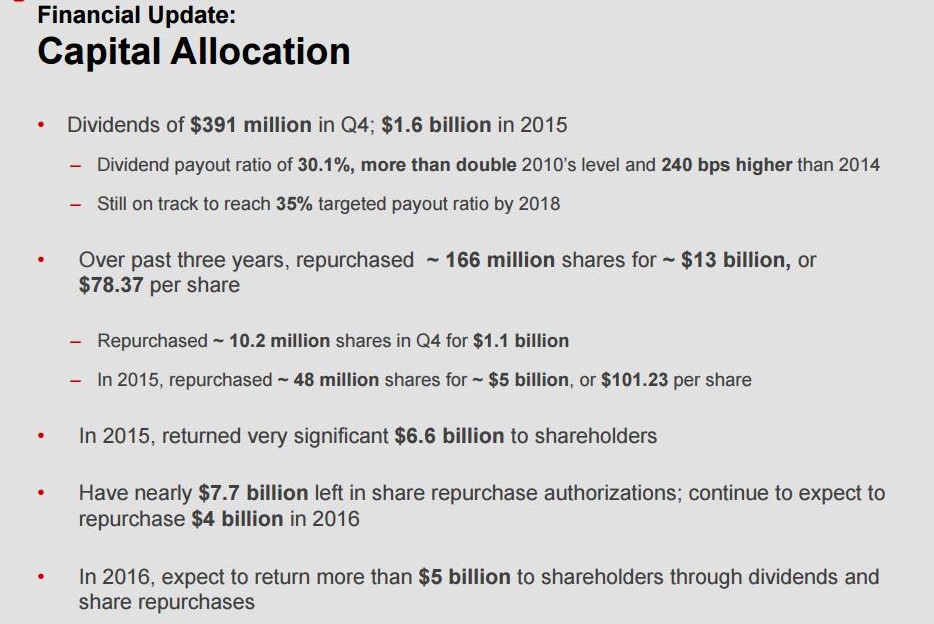

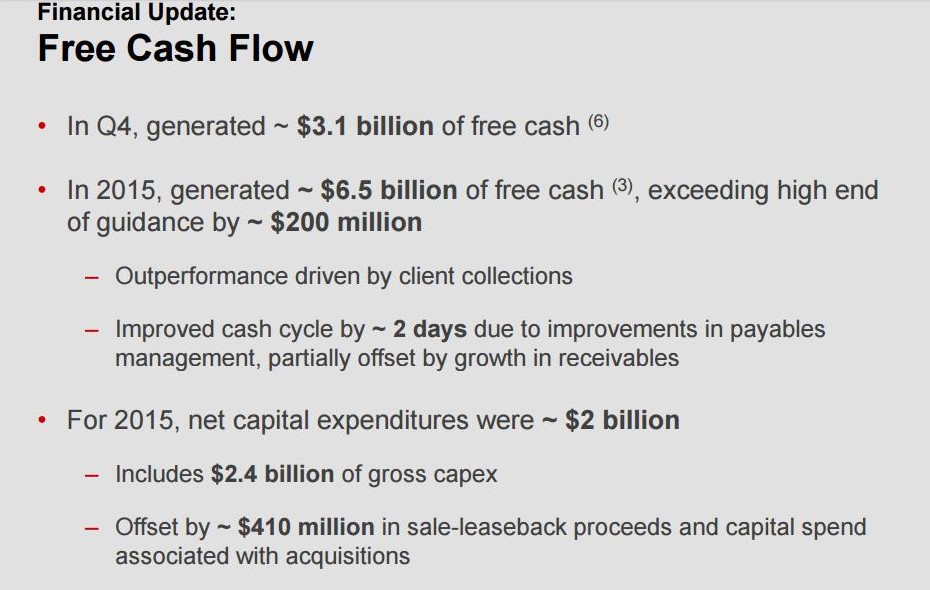

Recently, CVS reported strong earnings for Q4 2015 and year-end results. Net revenue increased 10% to $153.3 billion while adjusted EPS increased to $5.16 or 14.8% as compared to the prior year (Figure 1). CVS also offered 2016 guidance of robust EPS growth of 11% to 14% or $5.73 to $5.88 and revenue growth of 17%-18.5% (Figure 2). At current levels (~$95), CVS boasts a P/E of 20.6 and given its growth rate, acquisitions, partnerships, aggressive stock repurchase program and dividends I believe this company is undervalued. In addition, to this robust earnings report. During 2015, CVS announced that it would boost its dividend by 21% and reiterated its five-year long-term financial targets. Capital returns in the form of share repurchases will likely reach the $4 billion mark during 2016 and the dividend will increase by 21% to $1.70 per year starting in 2016 (Figure 3). CVS repurchased 48 million shares while returning $6.6 billion to shareholders in 2015 and expected to return $5 billion in 2016 (Figure 3). It is noteworthy to point out that this is the thirteenth consecutive year that CVS has increased its dividend payout. In 2015, CVS generated $6.5 billion in free cash flow which exceeded the high end of its guidance (Figure 4).

Figure 1 – 2015 revenues, EPS and free cash flow summary compared to 2014

Figure 2 – 2016 guidance for revenue and EPS

Figure 3 – Capital return program through dividends and share buybacks

Figure 4 – 2015 free cash flow

CVS Driving Growth Via Acquisitions And Partnerships – 2016 Integration

CVS acquired Omnicare for $13 billion earlier this year and just recently acquired all of Target’s pharmacies for $1.9 billion. These two acquisitions, once fully integrated will boost both top and bottom line revenue while geographically expanding its footprint across the US particularly in the Pacific Northwest via the Target acquisition where CVS has limited operations. The Omnicare acquisition will significantly expand its ability to dispense prescriptions in assisted living and long-term care facilities that serve the senior patient population. CVS will also expand its presence in the rapidly growing specialty pharmacy business. In terms of specialty pharmacy, this business increased 31% in 2014 and is expected to grow to 44% of total drug spending by 2017. Omnicare’s complementary specialty pharmacy platform and clinical expertise will augment CVS Health’s capabilities and enable CVS Health to continue to provide innovative and cost-effective solutions to patients. CVS Health expects to achieve significant purchasing and revenue synergies as well as operating efficiencies from this combination.

Per CVS, the Omnicare business is performing well and in line with expectations thus far and multiple opportunities exist to drive enterprise value. CVS expects to complete the majority of Omnicare integration activities by year end. Throughout the first half of 2016, they expect to achieve benefits of purchasing synergies. Opportunities to drive long-term revenue synergies focused on transition of care and care coordination offering for acute care in the home setting enabling CVS to capture a portion of the 2 million patients discharged from skilled nursing facilities annually. CVS should begin to realize revenue synergies in 2H16 and growing thereafter.

CVS Health also acquired Target’s more than 1,660 pharmacies across 47 states and will operate them through a store‐within‐a‐store format, branded as CVS/pharmacy. It’s also important to point that a CVS/pharmacy will be included in all new Target stores that offer pharmacy services. Thus, as Target continues to expand, CVS will continue to expand its pharmacies in lock-step. Target’s nearly 80 clinic locations will be rebranded as MinuteClinic, and CVS Health will open up to 20 new clinics in Target stores. The new clinics will be part of CVS/MinuteClinic’s plan to operate 1,500 clinics by 2017. In addition, CVS Health and Target plan to develop five to ten small, flexible format stores over a two‐year period following the deal close, which will each be branded as TargetExpress and include a CVS/pharmacy.

Per CVS, the Target integration activities are well underway and store conversions expected to be completed by the end of the summer. These conversions will ramp throughout Q1 and Q2. There will be additional core pharmacy offerings available as each pharmacy conversion is complete. CVS is focusing on converting Target guests who don’t currently use the pharmacy.

CVS has also partnered with three telehealth companies – American Well, Doctor On Demand and Teladoc to explore how direct-to-consumer telehealth providers, retail pharmacy and retail clinic providers can collaborate to improve patient care. Taken together, CVS is growing its business organically and via strategic acquisitions and partnerships to drive shareholder value and growth now and into the future. The two key acquisitions are well underway and should bear fruit into 2016.

Growing Revenues Augmented By Dividends And Share Buybacks

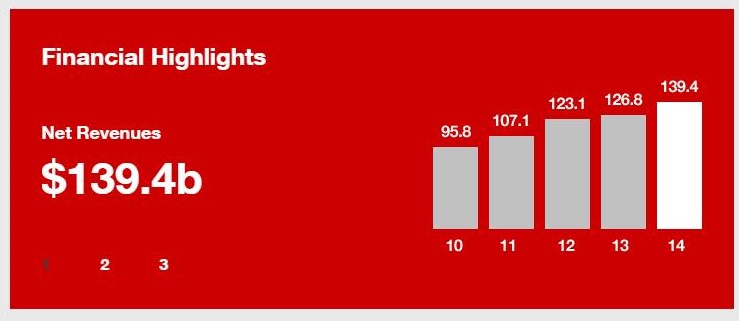

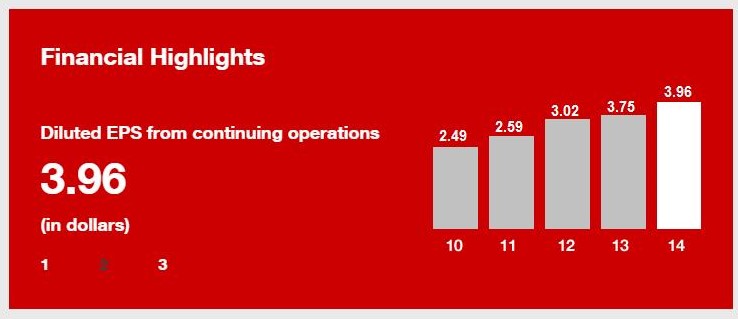

CVS has grown its revenues greater than 45% from 2010 through 2014, growing revenues from $95.8 billion in 2010 to $139.4 billion in 2014 to a current $153.3 billion in 2015 (Figure 5). EPS has increased by 59%, growing from $2.49 to $3.96 in 2014 to a current EPS of $5.16 (Figure 6).

Figure 5 – Five-year revenue history (2010-2014), 2015 revenues were $153.3 billion

Figure 6 – Five-year EPS history (2010-2014), 2015 EPS was $5.16

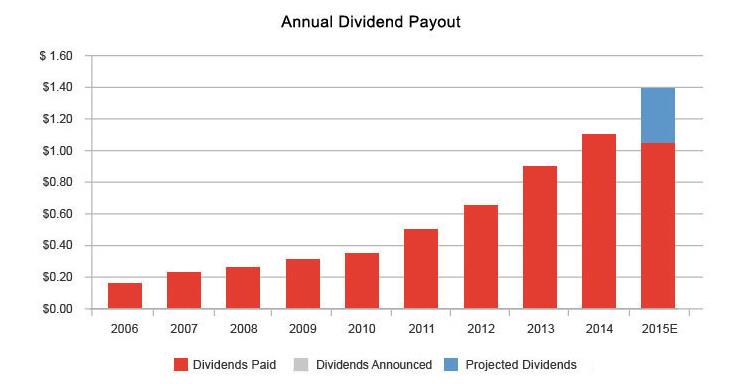

In addition to growing revenues and profits, CVS offers a backdrop of dividend payouts along with a share repurchase program. CVS has increased its quarterly dividend payout by nearly 800% over the past 10 years from $0.04 to $0.35 per quarter. With the newly approved 21% boost in its dividend, beginning in 2016 CVS will have a quarterly payout of $0.4235. This translates into a 1.8% yield based on its current price (Figure 7).

Figure 7 – Dividend History of CVS from 2006 through 2015

Due to the Target pharmacies purchase, CVS Health is reducing its share repurchase guidance for 2015 by $1 billion, from $6 billion to $5 billion. Despite the decrease, the $5 billion earmarked for share repurchases still accounts for more than 4% of outstanding shares. For 2016, CVS has guided that it aims to deploy $4 billion to repurchase shares. This remains an aggressive buyback program and along with its dividend shareholders are doubly rewarded.

Summary

CVS is well-positioned for future growth and success in the growing healthcare space as further supported by its current quarterly and annual 2015 earnings report. CVS has been highly acquisitive, growing dividends over time and buying back its shares to drive shareholder value. Its major acquisitions and partnerships via Omnicare, Target pharmacies and Telehealth companies position CVS to continue its strong performance and competitiveness in the marketplace. These acquisitions are well under way of being fully integrated under the CVS umbrella and will likely make a meaningful impact on revenue and EPS in 2016. The company does not shy away from deploying capital to acquire other assets to drive growth into the future. In addition to their acquisitive mindset, CVS also offers the backdrop of dividends and share repurchases to add value to shareholders. CVS appears to be undervalued based on its growth and future earnings as measured by its P/E and PEG ratios. Considering the most recent quarterly and annual earnings report, CVS may be a great holding for any long-term investor.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author currently holds shares of CVS and the author is long CVS. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.