The last FOMC meeting for 2016 has concluded, and the outcome is a slightly more hawkish tone than investors initially expected. The Fed has hiked the federal fund’s target rate by 25bps to 0.75% for the second time in two years. However, this hike was largely in line with the consensus expectations.

What caught investors by surprise was the revision of the Fed’s projection for rates in 2017. A revision that demonstrates that the median of estimates by the Federal Reserve members point to not two rate hikes, as in the September meeting, but three. Experience suggests that investors should take the Fed’s revision with a pinch of salt. After all, it was only this year that we witnessed the Federal Reserve revise its rate projections down, a move that followed an increase earlier in the year. And yet, judging by the reaction of Treasuries and the dollar, this revision is taken with some gravity. In fact, it paves the way for another dollar higher. The question is why?

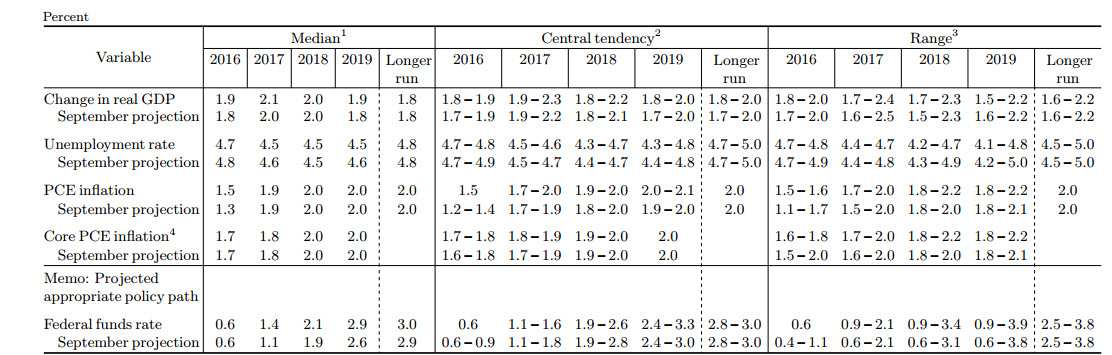

When we examine the Federal Reserve’s press release and the revision of the Federal Reserve board members’ projections, we notice something interesting.

The Federal Reserve’s median projection for rates in 2017 up to 2019 have been revised upward; a moderate revision for the long-term. The median projection of Fed board members is expecting the Federal Funds rate to be 1.4% in 2017, an upgrade from the September projection of 1.1%. A 2.1% rate is projected for 2018, compared with the September projection of 1.9%. A 2.9% rate is projected for 2019, compared with 2.6% in September.

And yet, as the table below illustrates, while the rate outlook has been revised up, the GDP outlook has been left almost unchanged as well as the outlook for core inflation.

Chart courtesy of The Federal Reserve

The reason for the dissonance is the tightening US job market. With unemployment at 4.6% and wage growth at 4.32% Year over Year, we get a classic case of an inflationary cycle. The tight job market leads to higher wages, which leads to higher consumer demand and higher prices aka inflation. And that is why the Federal Reserve wants to ease the pressure, and maintain inflation close to its 2% target by potentially raising rates three times next year. Except that raising three times won’t suffice if US growth accelerates beyond the median than the median forecast of 2.1%. In fact, the latest reading of annualized GDP growth has hit 3.2%. An examination of the chart below may also suggest that the US annualized GDP growth rate has potentially hit an inflection point and could potentially accelerate even further.

Moreover, that is before we consider the Trump effect. The president-elect has already outlaid his plans for a dramatic cut in the US corporate tax, in addition to a significant increase in infrastructure spending. Of course, the president-elect’s plans have yet to become a reality which leaves risk for the upside, both in US deficits and more importantly GDP growth.

Chart courtesy of Tradingeconomics

Additionally, because there is a high likelihood that US GDP growth rate for 2017 will surpass the median estimate of 2017, we could potentially be looking up to four rate hikes next year. That is why the latest Federal Reserve projection paves the way for a dollar rally. Three rate hikes alongside a 2.1% growth rate may be the moderate scenario, while the possible scenario suggests more rate hikes, more policy diversion from Europe and Japan. Therefore, a new dollar rally with the USD/JPY possibly eyeing 125, while the EUR/USD seems to be on the way to 1.00, parity between the euro and the dollar.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

What are your views for the USD/GBP for 2017? Thank you!