Introduction

CVS Health (NYSE:CVS) recently reported what was ostensibly another great quarter reporting a year-over-year increase of 28% and 16% in EPS and revenue, respectively. After reporting its Q3 earnings, CVS sold off 17%, moving down from $84 to $70 at market open. I’ve written several articles putting forth the case that CVS presents a compelling investment opportunity in the growing healthcare space. My investment thesis was based on the fact that CVS has been highly acquisitive, continues to deliver robust earnings growth, revenue growth, growing dividends and has an aggressive share buyback program in place. With its recent acquisitions of Target’s pharmacies and Omnicare, these proactive measures will significantly expand its presence and ability to dispense prescriptions to the general public and in long-term care facilities. As healthcare costs and prescription drug costs continue to rise and the population continues to age with the elderly comprising a larger segment of the overall population, CVS looked poised to benefit. Recent marketplace trends have forced CVS to cut guidance for Q4 2016 and the full-year 2017 numbers. Given this dichotomy between the company’s historically strong fundamentals and share price, was this an overreaction or was the selloff justified?

The Political Backdrop

First, let’s assess the political backdrop and how this has not only been a headwind for the entire sector but has also caused increased volatility. The entire pharmaceutical supply chain from drug manufacturers (i.e. Mylan and AbbVie) to pharmacies/pharmacy benefit managers (i.e. CVS and Walgreens) and the drug wholesalers in-between (i.e. McKesson and Cardinal Health) have been hit particularly hard in 2016. The confluence of proposed legislative action via Proposition 61 in California, continuous threats by presidential candidates such as Hillary Clinton and Bernie Sanders, Senate summons for Valent and Mylan to defend drug pricing and pricing pressures/pricing competition throughout the pharmaceutical supply chain have pummeled the sector. Drug manufacturers, wholesalers, pharmacy benefit managers and pharmacies have not been immune to this massive sell-off. With the presidential election now finalized, the mere absence of political uncertainty seems to have provided a much-needed short-term lift to the sector despite subpar earnings and guidance by McKesson and CVS.

Q3 2016 Guidance Concerns?

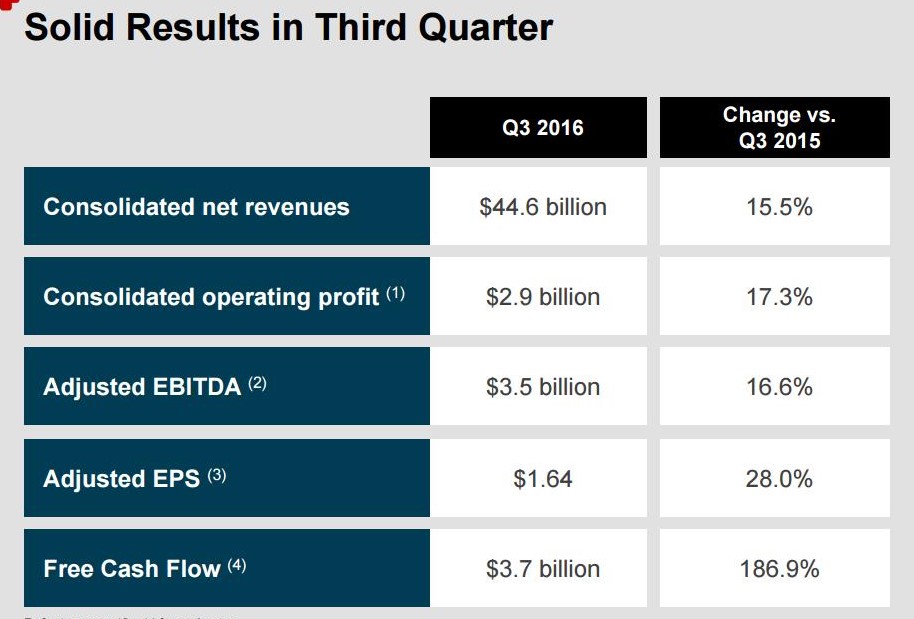

CVS reported solid earnings for Q3 2016 and the stock immediately tanked by 17% shedding $14 per share. At current sold-off levels of $77.50, CVS boasts a P/E of ~16.5 and given its growth rate (despite the lowered guidance), acquisitions, partnerships, newly issued aggressive stock repurchase program and dividends I believe this company is undervalued at these levels. Diving into the Q3 2016 results, net revenues for the three months ended September 30, 2016, increased 15.5%, or $6.0 billion, to $44.6 billion. Over the same time period, adjusted EPS grew by 28%. Operating income, net income and free cash flow grew by 21%, 25% and 187% respectively (Figure 1).

Figure 1 – Q3 earnings highlights

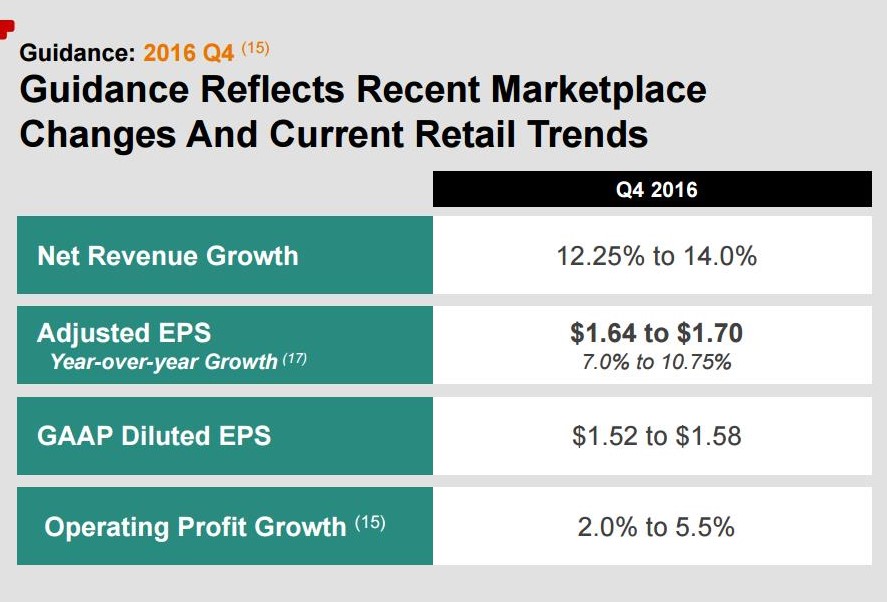

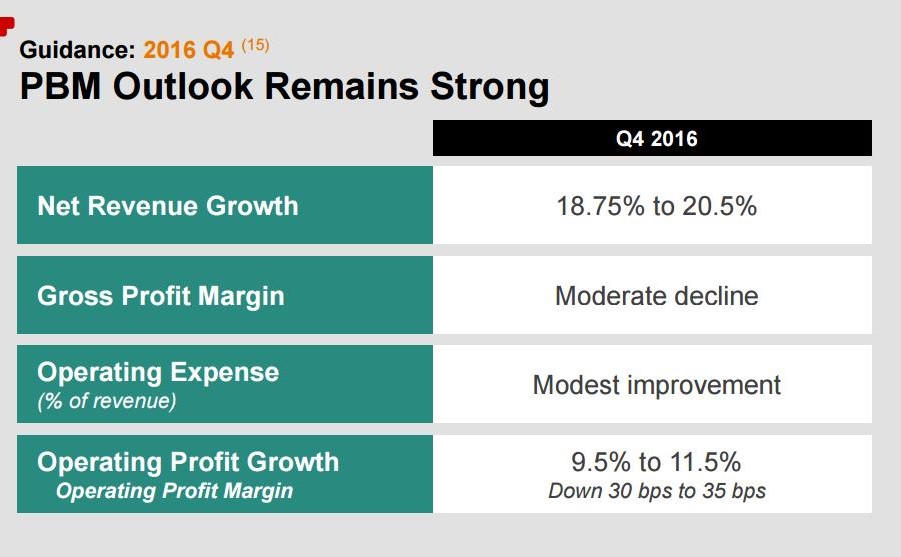

CVS issued guidance that scared investors for both the full-year 2016 numbers and the preliminary 2017 full-year numbers. First off, for 2016, CVS lowered the midpoint of EPS by 5 cents. CVS stated that the numbers were lowered due to “competitor actions restricting us from pharmacy networks as well as current trends in the retail business”. CVS stated that there’s slowing prescription growth in the overall market and a soft seasonal business affecting the pharmacy and the store front. Given the uncertainty, a wider EPS range was provided. Some good news for the Q4 enterprise revenue and operating profit growth will be driven primarily by PBM growth. CVS anticipates Q4 total same-store sales and adjusted prescriptions comparables will sequential decline due to the impact of the network changes and retail trends (Figures 2 and 3).

Figure 2 – Q4 2016 guidance

Figure 3 – Q4 2016 PBM guidance

Unexpected Marketplace Changes and Long-Term Outlook

Recent marketplace trends have forced CVS to cut guidance for Q4 2016 and the full-year 2017 numbers. CVS stated that “unexpected marketplace actions that will have a negative impact on our Q4 2016 results and a more meaningful impact on our outlook for 2017”. These network actions will result in more than 40 million retail prescriptions shifting out of stores on an annualized basis. CVS lost a contract with the Department of Defense to Walgreens which carries tens of millions of prescriptions on an annual basis. New restricted network relationship between Prime Therapeutics and Walgreens impacts CVS Pharmacy’s participation in selected fully-insured networks in several key states and in many cases make CVS Pharmacy a non-preferred provider for Medicare Part D as well. To add insult to injury, these prescriptions tend to be the most profitable prescriptions.

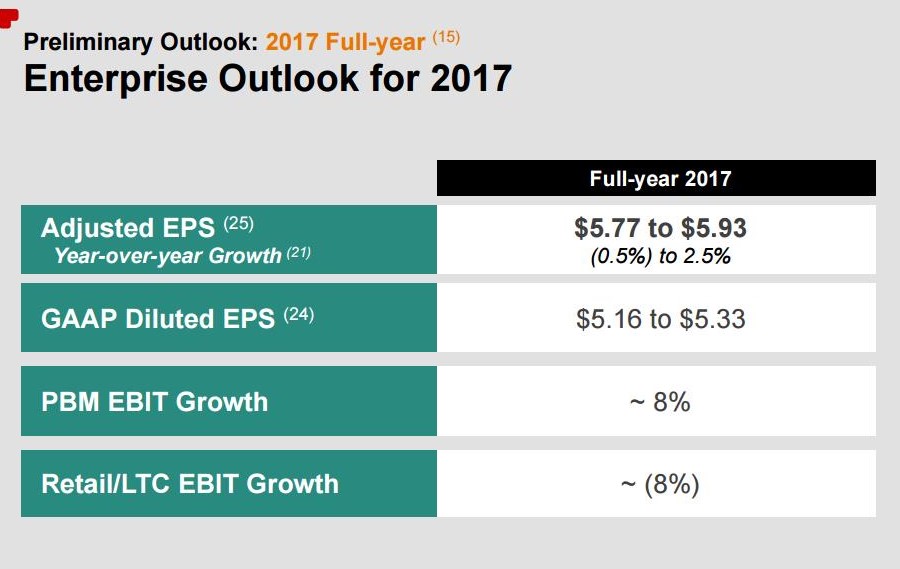

The PBM segment remains a positive for the company with specialty expected to deliver strong growth. The Retail segment is expected to see a significant headwind of more than 40 million prescriptions from network changes and year-over-year growth acceleration from Omnicare and Target slightly slower than anticipated. Currently, CVS expects year-over-year EPS of about 17 cents, which includes impact on CVS pharmacies within Target related to network changes, compared to initial forecast of 26 cents. Despite these negatives, moving into future years CVS is targeting 10% adjusted EPS growth and the generation of $7 billion to $8 billion in free cash flow annually (Figure 4).

Figure 4 – 2017 Guidance

Share Buybacks – The Company’s Long-Term Conviction

CVS continues to drive shareholder value with significant cash generation and deploying this cash in the form of an annual dividend increases and share buybacks. CVS just announced that they are committing $15 billion to repurchase shares. Combined with what is remaining in the prior authorization, CVS now has $18.7 billion available for share buybacks. If all the cash was utilized right now to purchase shares then over 20% of the share float could be bought and retired. Considering the shares have sold off rather drastically, I’m hoping CVS is putting this money to work with an accelerated share repurchase program. CVS also offers a backdrop of dividends which is now a quarterly dividend of $0.4235 which translates into a 2.2% yield based on its current price. Collectively, CVS’s buybacks and dividend payouts doubly reward shareholders. For full-year 2016, $6 billion will be returned to shareholders via a combination of dividends and share buybacks.

Summary

Recent marketplace trends have forced CVS to cut guidance for Q4 2016 and the full-year 2017 numbers. CVS will lose 40 million retail prescriptions on an annualized basis due to Department of Defense business moving to Walgreens and a restricted network relationship between Prime Therapeutics and Walgreens impacting CVS Pharmacy’s participation in selected networks and render CVS a non-preferred provider for Medicare Part D. In addition to the Retail segment experiencing a headwind of more than 40 million prescriptions from network changes, year-over-year growth acceleration from Omnicare and Target will be slightly slower than anticipated. Despite these headwinds, the PBM segment remains a positive for the company with specialty expected to deliver strong growth. Moving into future years CVS is targeting 10% adjusted EPS growth and the generation of $7 billion to $8 billion in free cash flow annually. For 2017, projected EPS growth will be in the range of flat to 2.5%. The company has committed $15 billion to share repurchases which shows the company’s long-term conviction of the business despite these headwinds. CVS has been highly acquisitive, growing dividends over time and buying back its shares to drive shareholder value. I think CVS has guided conservatively and will make the appropriate adjustments to mitigate the aforementioned headwinds. The new administration will likely bode well for the entire healthcare cohort in terms of taxes, mergers and acquisitions and deregulation which may allow further marketplace easing. I remain long CVS Health (NYSE:CVS), particularly at these levels moving into 2017, thus I feel the selloff is an overreaction.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author currently holds shares of CVS and the author is long CVS. The author sold a secured put on CVS with a strike of $85 with an expiration of Q1 2017. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.