OPEC reported in its January Monthly Oil Market Report (MOMR) that OECD commercial stocks fell to 2.993 billion barrels, around 271 million barrels above the latest five-year average. Saudi Arabia's energy minister, Khalid Al-Falih, stated last week that production cuts by OPEC and non-OPEC countries may reduce global oil inventories to the five-year average by June thereby rendering a continuation of the cuts unnecessary.

But three closely-watched sources of energy data do not support such a drop in global oil inventories. The Energy Information Administration (EIA), the International Energy Agency (IEA) and OPEC itself published their monthly reports in January, attempting to include impacts of the production cuts. Two of the sources, EIA and OPEC, provide data that show (or imply) stock builds over the first half, and the IEA data show a drawdown but not of the magnitude suggested by Mr. Al-Fahil.

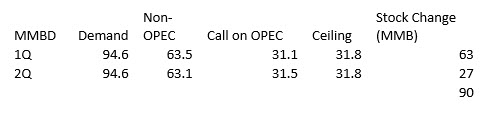

OPEC

OPEC’s Monthly Oil Market Report (MOMR) for January shows figures of its updated estimates of global oil demand, non-OPEC supply, and the "call" on OPEC oil.

Overall, the numbers show a call on OPEC oil of 32.1 million barrels per day (mmbd) for the year. OPEC had set a ceiling of 32.5, but that included Indonesia, which has left OPEC.

Assuming OPEC revises its ceiling down to 31.8 mmbd to account for the loss of Indonesia, the surplus would grow by 90 million barrels during the first half of the year, assuming full compliance with OPEC and non-OPEC production cuts.

EIA

The EIA stats show total OECD commercial inventories ending December 2016 at 3.101 billion. That figure is 309 million higher than the 5-year average.

EIA projects OECD stocks to end at 3.112 billion in March and 3.141 billion at the end of June, a total build of 40 million barrels. The EIA projections do not reflect OPEC is 100% compliant with its output ceiling (including Indonesia) of 32.5 million barrels per day.

IEA

The IEA published the most favorable supply/demand from OPEC’s standpoint. It projects that demand will exceed supply by 700,000 b/d for the first half of 2017. But applying that for the full 6 months (180 days) yields a stock draw of 126 million barrels, not even half of the 273 million surplus over the 5-year average.

There are other problems. OPEC’s original numbers added to 32.7 million, not the 32.5 million barrel ceiling, so the cuts fall short 200,000 b/d if fully implemented.

Libya was assigned no production ceiling due to the disrupted state of its petroleum industry. But since the “reference month” of October, it has increased its production by 200,000 b/d and expects to add another 200,000 b/d over the next few months.

The Russian oil minister stated over the weekend that his country had cut 100,000 b/d of the 300,000 commitment. In addition, the Russian oil minister said that there were cuts of another 100,000 b/d that were committed but not yet made. It remains to be seen how long it will them to make additional cuts.

The U.S. Energy Department has made the first sales of the Strategic Petroleum Reserve (SPR) to commence in March. They project continuous sales of 70,000 b/d this year.

Conclusions

There are uncertainties in these estimations. OPEC and the EIA are forecasting inventory builds over the first half of 2017.

Using the IEA’s numbers, the most optimistic scenario is a draw of 126 million barrels. But if there is less than 100% compliance, and/or oil production increases in Libya, Nigeria, and/or the U.S., the size of IEA’s draw may be reduced or even erased.

I am quite certain, in any event, that the storage overhang will not be depleted in the first half of 2017. If there were some unexpected disruption to supplies of sufficient magnitude, the Strategic Petroleum Reserve would be drawn upon.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.