Options trading is a long game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions. To this end, an options-based portfolio requires discipline and time to materialize in order to reach its full benefits when benchmarked to a broader index. An options-based approach provides a margin of safety with a decreased risk profile while providing high-probability win rates. An options centric portfolio ebbs and flows just like any portfolio as various types of trades are executed, management of trades are carried out and the inevitability of assignment of occurs. Over the long-term, this approach provides smooth portfolio appreciation while generating consistent income. Since options are a bet on where stocks won’t go, not where they will go, this is accomplished without predicting which way the market will move. When adhering to options trading fundamentals, this approach can provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves. Following these option trading fundamentals, I’ve demonstrated an 85% (175/205) options win rate over the previous 9 months through both bull and bear markets while outperforming the S&P 500 over the same period by a wide margin producing a 4.51% return against a 0.95% for the S&P 500.

Results

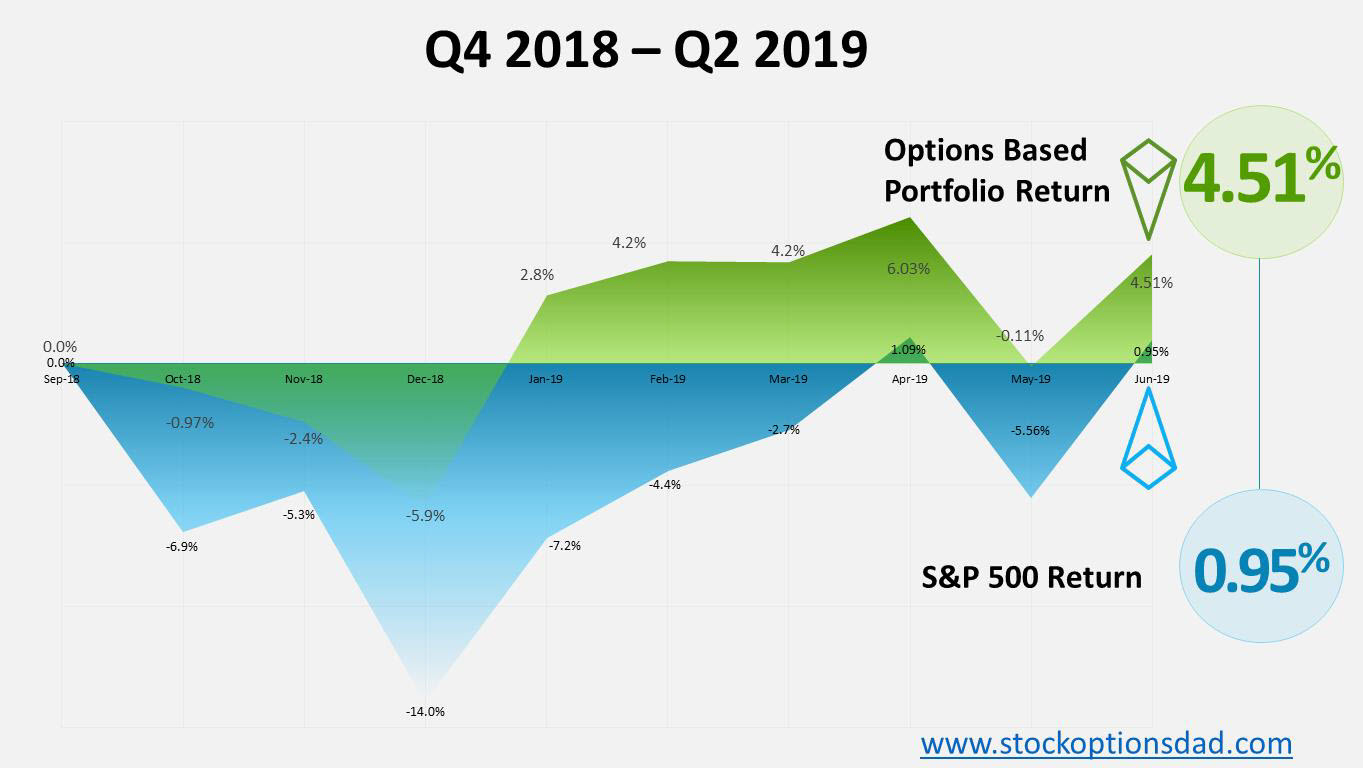

The broader market has been tumultuous over the past 9 months, to say the least. In Q4 2018, the S&P 500 posted one of its worst quarters and since the Great Depression with the index selling off 14% and erasing all of its gains for the year. 2019 started off on a high note for the S&P 500 with January posting a 7.9% gain, logging its best January in over 30 years. This was followed by continued strength in February, putting the index on its best footing since 1991 with a cumulative return of 11% through the first two months and rounding out Q1 2019 up just over a 13% return. May witnessed a market sell-off which saw a decline of -5.8%. June 2019 was the best June for the Dow since 1938 whereas the S&P 500 posted its best first half of a year since 1997, notching a 17.3% gain. Sticking to a set of disciplined fundamentals through this volatile market over the previous 9 months generated superior returns relative to the historic run by the S&P 500 (Figures 1-4).

Figure 1 – Options based portfolio return (4.51%) in comparison to the S&P 500 return (0.95%)

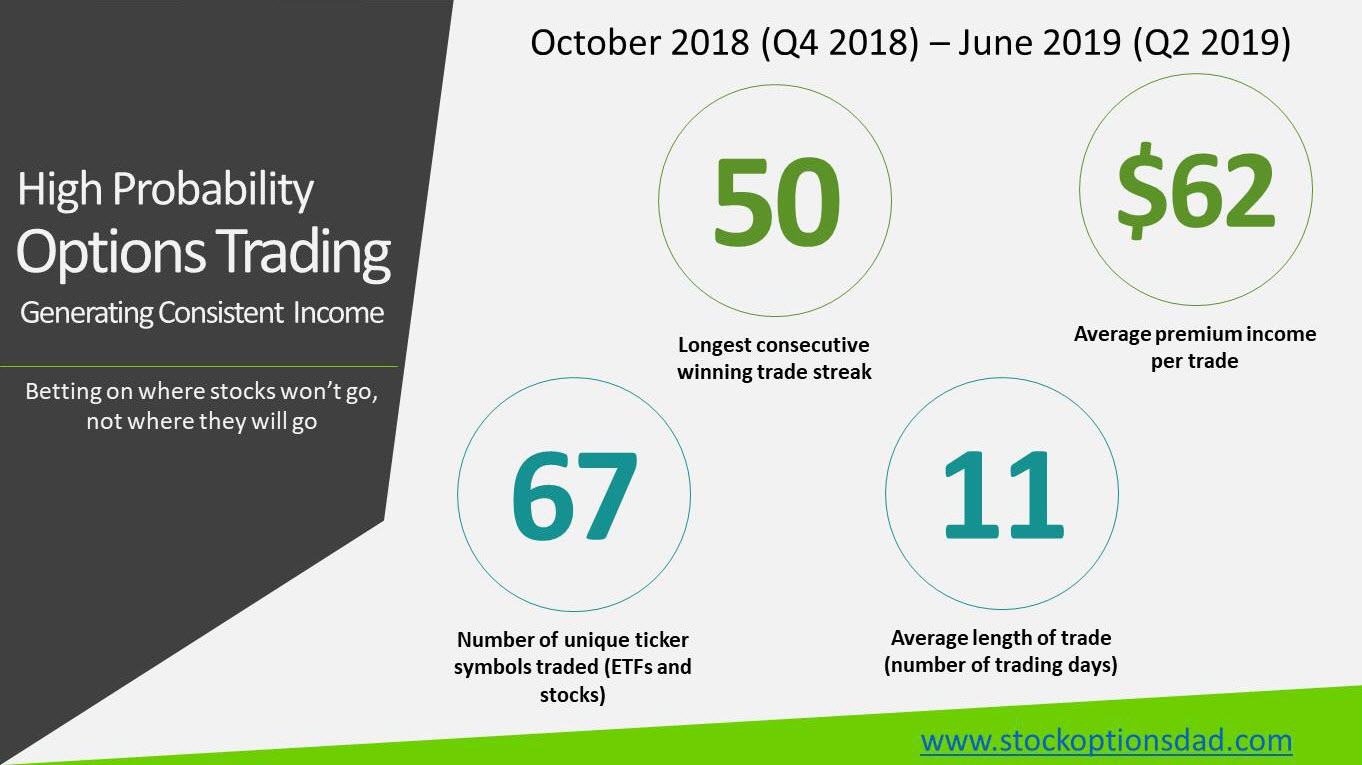

Figure 2 – Comprehensive options metrics over the previous 9 months

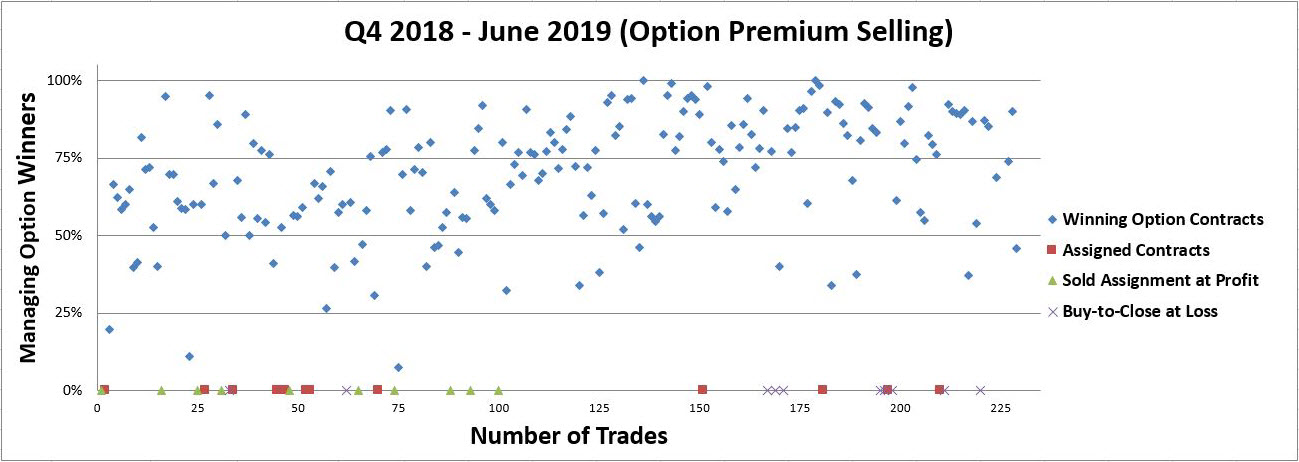

Figure 3 – Dot plot summarizing ~225 trades over the previous 9 month period

Figure 4 – Additional, comprehensive options metrics over the previous 9 months

Difficult Market Conditions Resulted In Mixed Results For Q2 2019

The options based portfolio did not perform as well as the broader index during Q2 2019 due to specific sector exposure weighing on performance.

- Oil and oil-related stocks sold-off (i.e., USO and SLB)

- Retail stocks tumbled double digits (i.e., GPS, URBN, LOW, KSS, and CPRI)

- Pharmaceutical supply chain stocks continued to be pressured (CVS and WBA)

- Financials couldn’t seem to get much traction (i.e., BAC and C)

- Steel stocks plummeted (i.e., X)

- Airlines were pushed lower (i.e., AAL)

A series of buy-to-close trades at a loss and a few assignments (KSS and X) largely negated premium income gains throughout the second quarter. Previously assigned positions from past quarters continued to weigh on performance (GE, SLB and USO) as well. Overall portfolio performance for Q2 2019 was anemic and slightly positive at 0.32%. Despite these mixed results, continuing to trade through all market conditions is essential to long-term options success.

Portfolio Approach

For the past 9 months, I’ve managed an options-based portfolio where I predominately leverage cash to sell options and collect premium income. The goal in options trading is to leverage cash and/or stock and sell options using the underlying cash and/or stock to collect premium income. This can be performed in a high-probability manner where a statistical edge goes to the option seller’s advantage.

The vast majority of my trades are cash covered puts. Thus I am not buying the underlying stock. However, I’m leveraging/earmarking cash and agreeing to buy shares at an agreed upon price by an agreed upon date. For example, if a stock sells for $50 per share now, I may elect to sell an option for $0.75 per share and agree to buy the shares for $45 one month into the future in exchange for $75 (since options trade in blocks of 100). When selling an option, one collects premium income ($75) in exchange for taking on the obligation/risk to buy the shares at the agreed upon price. I contractually agree to buy shares with a high probability that the shares will not trade lower than $45 before expiration. Thus, I’ll capture the premium income of $75 and re-purpose the cash that was earmarked upon expiration of the contract.

I like this type of trade when coupled with a high implied volatility rank (IV Rank) value because there’s a high probability that the shares will not be as volatile as the market is predicting as measured by IV Rank. Historically, predicted volatility is nearly always overestimated; hence, the stock will be less volatile than predicted. Meanwhile, a healthy margin of safety to the downside is built into the trade, and in this case, it’s a 10% cushion to the downside. Taken together, these types of trades are placed 1 standard deviation out-of-the-money to yield ~85% probability of winning the trade at expiration. These probabilities of success are based on past volatility moves over a given timeframe of the underlying security. Using past volatility moves, the market can use this to predict future stock volatility and probability of success. When IV Rank values are high, rich premiums are paid out at any given strike price since market participants are predicting a high level of volatility. If the shares break below the strike of $45, then your effective purchase price would be $44.25 per share since $0.75 per share was received upfront in the form of premium income. Best case scenario, premium is collected, and cash is re-purposed for future trades while worst case scenario is an assignment at $44.25 (which is 10% lower than the stock traded at the time of the initial trade).

The 7 Essentials for Effective Options Trading

Let’s review these 7 essentials that provide long-term options trading success for durable portfolio appreciation.

- 1. Be an overall options seller

- 2. Sell options in high IV Rank scenarios

- 3. Sell options that possess liquidity in the options market

- 4. Set an appropriate probability of success using Delta as a proxy

- 5. Manage winning trades

- 6. Maximize the number of trades

- 7. Limit position sizing/allocation

Mitigating Risk

This outperformance is due in part by proactively addressing losing trades to manage the overall risk profile. When engaging in options trading, losing trades are inevitable however managing these trades via risk-defined trades, position sizing, diverse sector allocation, buying-to-close for a gain or loss, allowing assignment to occur at expiration, selling covered calls on the assigned stock and rolling the trade out to a different strike level can mitigate risk and enhance long-term successful options trading. In the end, following a set of options, trading fundamentals will enable your portfolio to appreciate steadily month after month for consistent portfolio appreciation.

Managing Trades and Optimizing Outcomes

A variety of actions can be deployed in a losing trade situation to mitigate risk and optimize portfolio performance. A rule of thumb that I generally stand by is limiting myself to selling options on underlying dividend-paying stocks in the large-cap space thus an event I’m assigned, I’ll own shares of the underlying company at a significant discount (since I always sell options out-of-the-money in high IV Rank situations) and a dividend to reinforce the position. There are four actions that I usually employ to manage trades:

- 1. Take the assignment and sell covered calls against your long position

- 2. Buy-to-close at a loss to avoid assignment altogether prior to expiration

- 3. Buy-to-close at a loss and sell a new further out-of-the-money option to reset your positioning

- 4. Sell option spreads to define your risk (sell a put and buy a further out-of-the-money put)

Upon assignment, selling covered calls is a great way to extract additional value while waiting for the underlying assigned position to recover or appreciate beyond your assigned price. If an option is near expiration and has already broken through my strike price, then I often buy-to-close at a loss, especially if earnings are due prior to expiration. If this situation presents itself, buying-to-close and taking the loss may be the superior route since the odds are not in your favor moving into earnings/expiration. If the underlying stock has already broken through the strike, then upon earnings, the stock may sink lower and result in a huge loss upon assignment. After buying-to-close at a loss (if that was the best action to take) then selling a further out-of-the-money option will offset the loss and reset the odds of being in your favor.

In order to define your risk, you can sell an option spread, which is when an option is sold, and another option is purchased further out-of-the-money. In this situation, you receive premium income for selling the option, and you use part of that income to buy protection via buying a further out-of-the-money option. If you sell a put at a strike of $65 and receive $100 in premium income, you can buy a further out-of-the-money put strike at $60 for $40 in debt. The net premium income would be $60 ($100 - $40), and the max loss would be $500 ($65 strike - $60 strike) if the stock broke through the $60 level. If the stock breaks through $60, you have the right to sell shares at $60 since you bought the put option as well for protection. So, the ideal scenario is the income of $60 at expiration, and the worst case scenario is a max loss of $500. This can be modulated to define risk and optimize net premium income.

Lessons Learned

Everything that could’ve gone wrong in May 2019 went wrong. Airlines, banks, retail, oil, pharmaceutical supply chain, and trade war sensitive stocks all disproportionally impacted my portfolio. Despite the diversity of tickers across sectors, occasionally trades go horribly bad even in large-cap, dividend-paying stocks that are ostensibly lower risk equities. CVS Health (CVS), American Airlines (AAL), Bank of America (BAC), General Electric (GE), Kohl’s (KSS), Schlumberger (SLB), US Oil ETF (USO) and US Steel (X) were all assigned and have weighed heavily on my overall portfolio throughout the past 8 months. All of these assignments were down double digits (~-20%) from the assigned purchase price at one point. These stocks have been dead weight, especially the stocks in the oil space and the middle of the trade war crossfire such as US Steel, General Electric, and Kohl’s. Case in point, CVS fell from $70 to $53 per share, dropping 24% in one week and Kohl’s dropped from $72 to $51, dropping 29% in a single week. These drastic market moves are unpredictable; thus, managing risk is essential. These unrealized losses could have easily been avoided had I executed a buy-to-close at a loss prior to earnings being announced for both Kohl’s and CVS and/or sold an option spread to define my risk.

Conclusion

This comprehensive options strategy provides key fundamentals for long-term successful options trading. These fundamentals allow your portfolio to appreciate steadily since options are a bet on where stocks won’t go, not where they will go, without predicting which way the market will move. These fundamentals provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves. I’ve demonstrated an 85% options win rate over the previous 9 months through both bull and bear markets while outperforming the S&P 500 over the same period by a wide margin producing a 4.51% return against a 0.95% for the S&P 500 with a lower risk profile. However, unrealized losses can pile up and negate these performance metrics if proactive management isn’t utilized. This includes a variety of techniques that can be deployed to mitigate unrealized losses and/or assignment altogether. Taken together, options trading is a long game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions. When adhering to options trading fundamentals, this approach can provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves.

Good write up. I actually follow some of the same thoughts.