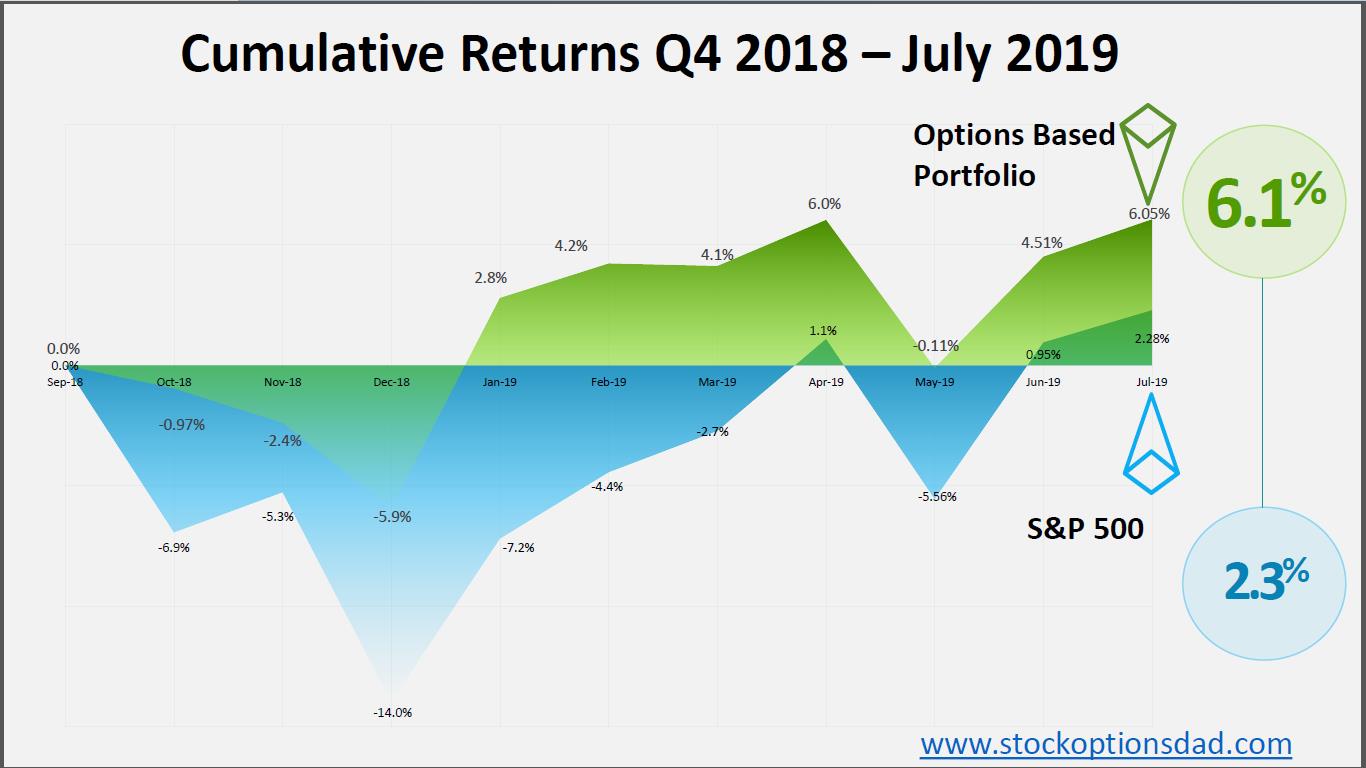

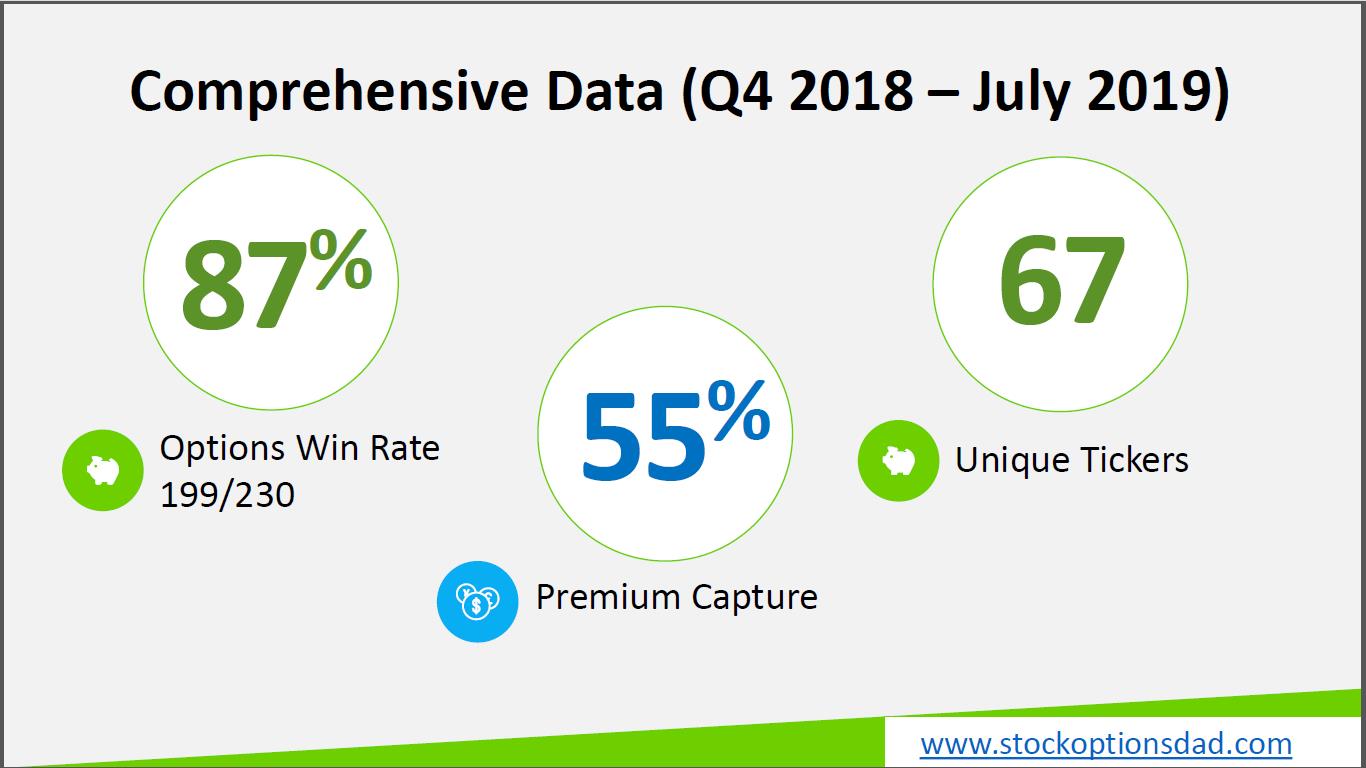

Generating smooth and consistent income month after month without predicting which way the stock market will move is the objective of options trading. Running an option-based portfolio offers a superior risk profile relative to a stock-based portfolio while providing a statistical edge to optimize favorable trade outcomes. Options trading is a long-term game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions. Put simply; an options-based approach provides a margin of safety with a decreased risk profile while providing high-probability win rates. Essentially, options are a bet on where stocks won’t go, not where they will go. Sticking to a set of fundamentals, this approach can provide long-term, high-probability win rates to generate consistent income while circumventing drastic market moves. In July, I posted a 96% (24/25) options win rate, and over the previous 10 months through both bull and bear markets that win rate percentage was 87% (199/230). Over the previous 10 months, the options-based portfolio outperformed the S&P 500 over the same period by a significant margin producing a 6.1% return against a 2.3% for the S&P 500.

What Does Life Insurance Have To Do With Options Trading?

Insurance companies sell policies based on actuaries and risk factors, then price these polices to their advantage. Insurance companies are betting on probabilities across insurance products and sell overpriced policies above their expected losses. The insurer agrees to pay out a specific amount of money for a specific loss (i.e., death). In return, the insurance company is paid monthly premiums, and based on this risk-based revenue model; it’s a very profitable business. Insurance companies sell policies with a premium cost level that maximizes a statistical edge to the insurance company’s benefit. The goal is to collect premiums over the course of the policy and never payout on the policies they sell to you. So, the probability of paying out on the policy is very low while the premiums received, over the policy lifespan will exceed your total benefit.

In terms of life insurance, it’s the probability that you won’t die before your predicted lifespan so the insurance won’t have to pay. The insurance company assumes you’ll die before the model predicts and will charge you more money via premiums upfront. In order to spread the potential payout risk, the insurance company will sell as many policies as possible to collect as much premium income as possible. In short, insurance companies have found a way to statistically place the probability of never paying out on these policies they sell to you in their favor.

Running Your Options Portfolio Like An Insurance Company

Options trading is much like the insurance example above. I receive premium payments (policy payments) in exchange for selling options (insurance). I sell these options with a statistical edge (underwriting) and a high-probability of winning the trade (insurance won’t have to pay). Occasionally, options move against you (death occurred) and you’re assigned stock (insurance is paid out) however in order to spread the risk of being assigned shares, options (insurance) are sold across a diversity of tickers that include both stocks and ETFs with varying expiration dates and optimal sector exposure. Additionally, risk is mitigated by appropriate capital allocation, position-sizing, and holding cash reserves in the portfolio.

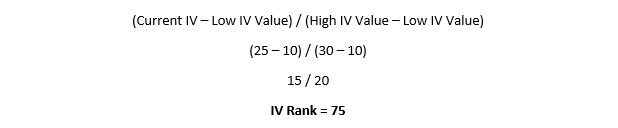

IV Rank – The Insurance Underwriter’s Edge

Implied Volatility (IV) rank is a measure of the current or predicted IV against its historic IV. When comparing these values, we can see how the current or predicted IV “ranks” in comparison to the past IV range. The predicted volatility is nearly always overestimated; hence, the stock will be less volatile than predicted. There’s a high probability that the shares will not be as volatile as the market is predicting when IV rank is high. Historic IV has a range, say the range of past volatility is 10-30 and the current IV value is 25, we arrive at an IV rank of 75.

This value of 75 is high relative to its historic range, and with this high value, options pricing is rich. Since the predicted volatility is high, traders are expecting a big move in the stock, which elevates options pricing. Since options pricing is largely determined by predicted volatility, as the stock fails to be as volatile as predicted, the IV rank value falls, and thus the option price falls as well. If an option is sold for $100 at an IV rank of 75 (knowing that stocks are less volatile than predicted), as the option lifecycle unfolds and the stock fails to become as volatile as predicted, the IV rank value may plummet to say a value of 30 (in conjunction with time premium decay), rendering the option value to ~$40. In this case, one can close the trade at $40 to net $60 in premium income. This is an iterative process where a premium is collected over and over again on these overpriced options due to a high IV rank value.

Options Results

The broader market has been tumultuous over the past 10 months, to say the least. In Q4 2018, the S&P 500 index sold off 14% and erased all of its gains for the year. 2019 saw its best January in over 30 years and rounding out Q1 2019 up just over a 13% return. May witnessed a market sell-off which saw a decline of -5.8%. June 2019 was the best June for the Dow since 1938 whereas the S&P 500 posted its best first half of a year since 1997, notching a 17.3% gain. July was a great month as well, and the S&P 500 has logged more than 20% return year-to-date. Sticking to a set of disciplined fundamentals through this volatile market over the previous 10 months generated superior returns relative to the historic run by the S&P 500 (Figures 1-4).

Figure 1 – Options based portfolio return (6.1%) in comparison to the S&P 500 return (2.3%)

Figure 2 – Comprehensive options metrics over the previous 10 months

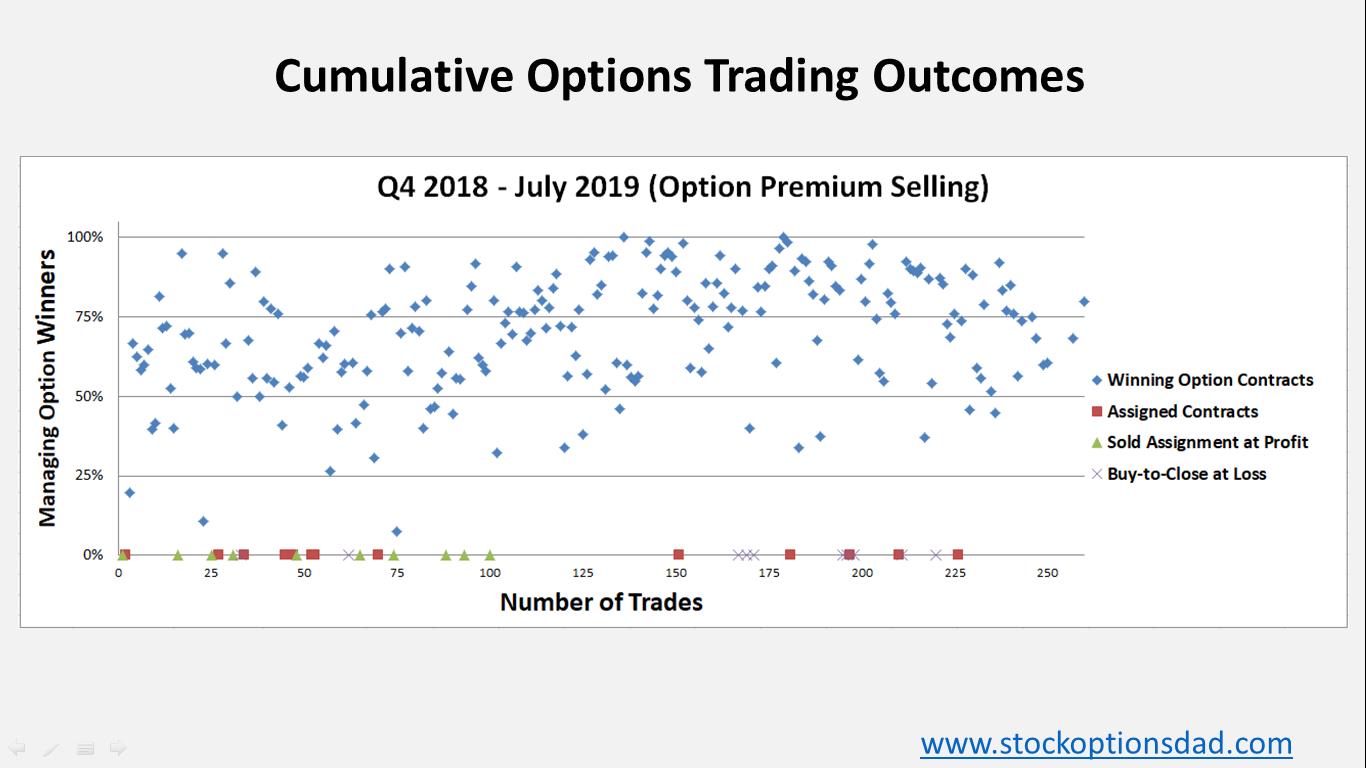

Figure 3 – Dot plot summarizing ~225 trades over the previous 10 month period

Figure 4 – Additional, comprehensive options metrics over the previous 10 months

Conclusion

An options-based portfolio has many similarities to an insurance company, selling option contracts in exchange for a premium. Selling options with a favorable risk profile and a high probability of success is essentially the bread and butter of insurance. Insurance companies sell policies with a premium cost level that maximizes a statistical edge to the insurance company’s benefit. The goal is to collect premiums over the course of the policy and never payout on the policies they sell to you. This options strategy provides key fundamentals for long-term successful options trading. These fundamentals allow your portfolio to appreciate steadily since options are a bet on where stocks won’t go, not where they will go, without predicting which way the market will move. These fundamentals provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves.

I’ve demonstrated an 87% options win rate over the previous 10 months through both bull and bear markets while outperforming the S&P 500 over the same period by a wide margin producing a 6.1% return against a 2.3% for the S&P 500 with a lower risk profile. Taken together, options trading is a long game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions. When adhering to options trading fundamentals, this approach can provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares in AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY and USO. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.