Previously, I wrote an article putting forth the efficient market hypothesis termed “There's No Edge In Stock Picking” and how less than 10% of fund managers outperform their benchmark over the long-term. These bleak performance metrics and the fact that there’s only a 36% chance that you pick a stock that outperforms the index is what makes options trading so effective.

Whether you want to win 70%, 80% or even 90% or your trades, you dictate your probability of success when it comes to options trading over the long-term. If you set your probability of success at ~85% and make trades at that probability level through all market conditions over the long-term on the scale of hundreds of trades, you’ll end up winning ~85% of your option trades. Options trading allows one to profit without predicting which way the stock will move. Options aren’t about whether or not the stock will move up or down; it’s about the probability of the stock not moving up or down more than a specified amount. Put simply; options are a bet on where stocks won’t go, not where they will go.

Options trading can generate consistent income and mitigate portfolio risk while producing high probability win rates. Options allow your portfolio to generate smooth and consistent income month after month without predicting which way the stock market will move. Running an option-based portfolio offers a superior risk profile relative to a stock-based portfolio while providing a statistical edge to optimize favorable trade outcomes. Options are a long-term game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions. An options-based approach provides a margin of safety with a decreased risk profile while providing high-probability win rates that are determined by the trader himself.

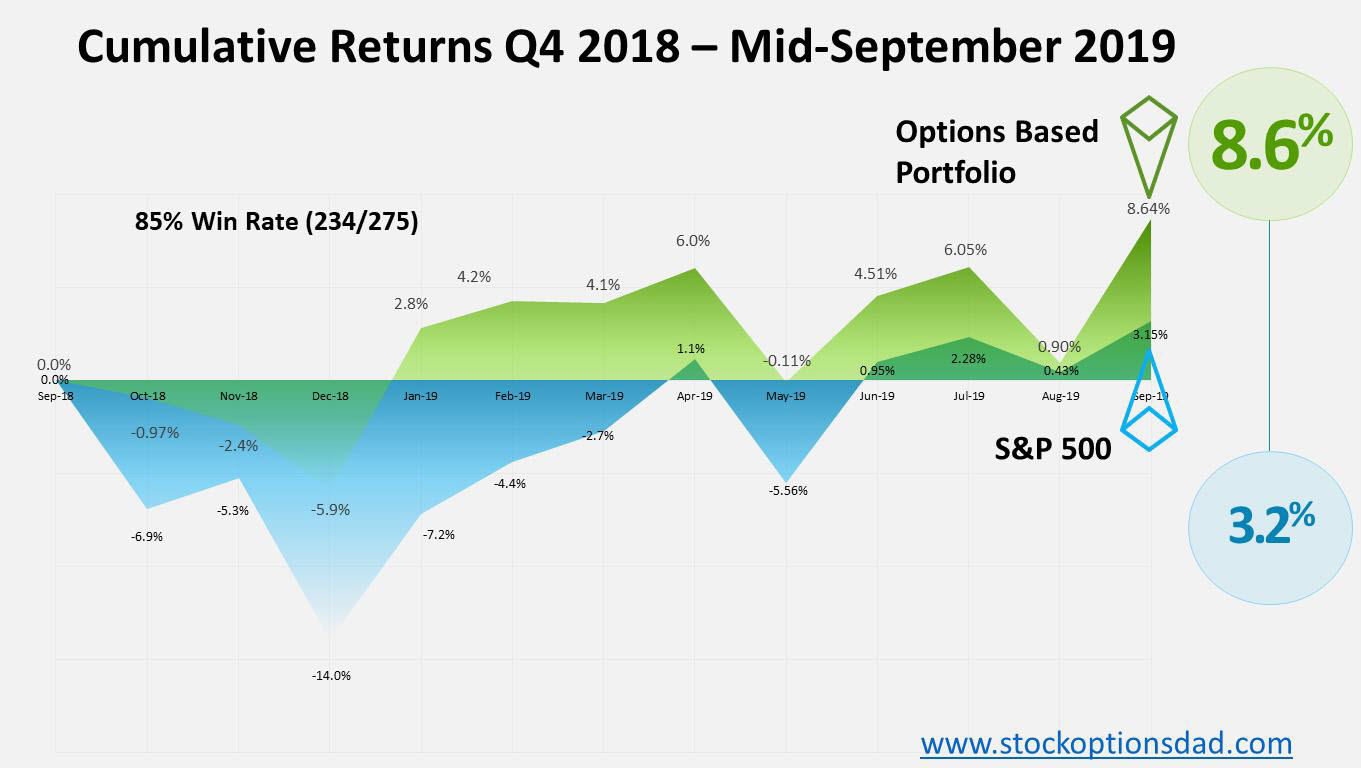

Empirically, over the previous 12 months, I’ve produced a return of 8.6% relative the S&P return of 3.2% while winning 85% of my trades via leveraging ~70 different ticker symbols.

Maximizing the Number of Trade Occurrences is Essential

A coin flip provides an equal probability of landing heads or tails hence 50:50 odds. However, the number of flips will influence the results and whether not they deviate from the expected probabilities.

- If you flip the coin 10 times, 7 heads and 3 tails may occur (70% heads / 30% tails)

- If you flip the coin 100 times, 60 heads and 40 tails may occur (60% heads / 30% tails)

- If you flip the coin 500 times, 275 heads and 225 tails may occur (55% heads / 45% tails)

- If you flip the coin 1,000 times, ~500 heads and ~500 tails may occur (~50% heads / ~50% tails)

Maximizing the number of occurrences is essential in options trading to smooth out any data skew that may result from trades that move outside of your probability target or as a result from a small sample size. There can be bad streaks and good streaks. In the market melt-downs of Q4 2018, May 2019, and August of 2019, I had a significant amount of assignments and positions that moved against me. My win rate for some months is 100% while other months may be as low as 70%. As I continue to maximize the number of trade occurrences across all market conditions, my win rate mirrors the probability of success I choose, which is typically the 85% level. I may have 3-4 assignments in a 10-trade block; conversely, I’ve won 50 consecutive trades. In order for the probabilities to play out, maximizing the number of trade occurrences is essential.

Fantasy Football and Options Trading

Fantasy football is a huge phenomenon for American Football fans. The idea is based on the performance of individual players at various positions that translates into points for his fantasy team. Based on past performance, the number of points for any given player is predicted prior to forming the fantasy football team. If a quarterback such as Tom Brady has historically passed for 300 yards on average per game then he’s predicted to score 12 fantasy points from passing (1 point for 25 yards passing) per game. He could throw for more or less than 300 yards, but he’s expected to throw around 300 yards per game. The probability of him throwing 150 yards is low while the probability of him throwing 450 yards is equally as low.

Future fantasy points are predicted based on past performance and other inputs such as the opponent’s defense and recent performance of the individual athlete. The likelihood of Tom Brady throwing between 250-350 yards for any given game is high. However, the likelihood of him throwing less than 200 yards or more than 400 yards is not as likely. Fantasy is a bet that Tom Brady won’t throw less than 200 yards or more than 400 yards per game. Betting on what the probabilities suggest provides durable and predicable points on a weekly basis. Could he have a huge game and throw for 500 yards, sure. Could he have a terrible game and throw for 175 yards, sure. But the likelihood of him performing at those extremes are statistically unfavorable hence the bet that those extremes won’t occur yet acknowledging that it’s a possibility. Over the course of the season, those extremes may occur here and there however the majority of games; the probabilities will fall into place.

How Probabilities are Determined in Options Trading

Stock options are no different, the probability of the stock trading between certain levels is determined by past moves (past performance) and future inputs such as earnings (opponent’s defense) and recent moves relative to the stock itself (Tom Brady vs. Tom Brady). Based on these data, future moves in the stock are predicted with a certain level of probability at various price levels.

Probability of success is determined by two factors:

- 1: Historic volatility – How much did the stock move in the past

- 2: Predicted (implied) volatility – How much will the stock move in the future

Options trading success is centered around the probability of the shares not moving up or down more than a specified amount. This is based on past moves and predicted future moves of a given stock over a given timeframe. Using “Delta” as a proxy for probability is a quick way to assess your probability of success on any given trade.

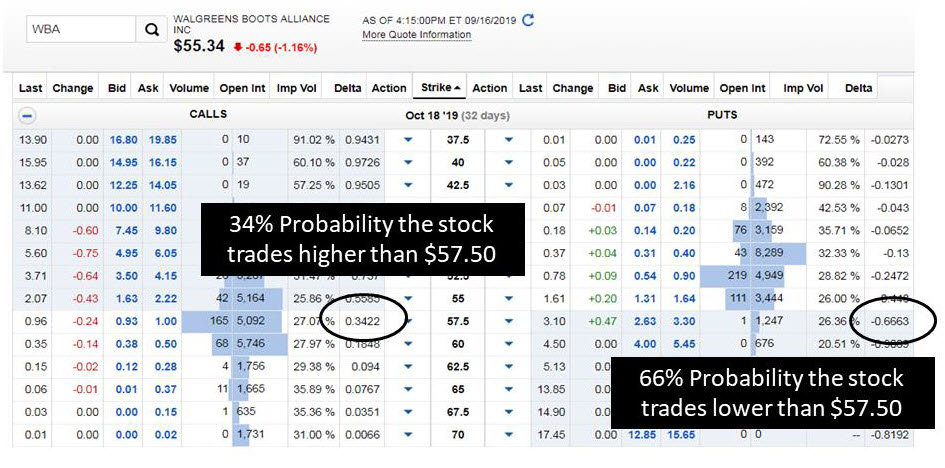

Walgreens (WBA) trades at ~$55 currently, and according to the Delta value, one month from now there’s a ~50:50 chance the stock trades higher or lower than $55. There’s a 55% (delta = 0.55) chance it trades higher (because it’s already a bit higher than $55) and a 45% (delta = 1-0.55) it trades lower (Figures 1 and 2).

On the call side: At the $57.50 level, there’s a 34% (delta = 0.34) chance it trades higher and a 66% (delta = 1-0.34) it trades lower.

On the put side: At the $57.50 level, there’s a 34% (delta = 1-0.66) chance it trades higher and a 66% (delta = 0.66) it trades lower.

Figure 1 – Options chain with Delta serving as a proxy for the probability of trade outcomes. On the call side, there’s a 34% (0.3422) chance that the shares trade higher than $57.50 and on the put side there’s a 66% (0.6663) chance the shares trade lower than $57.50.

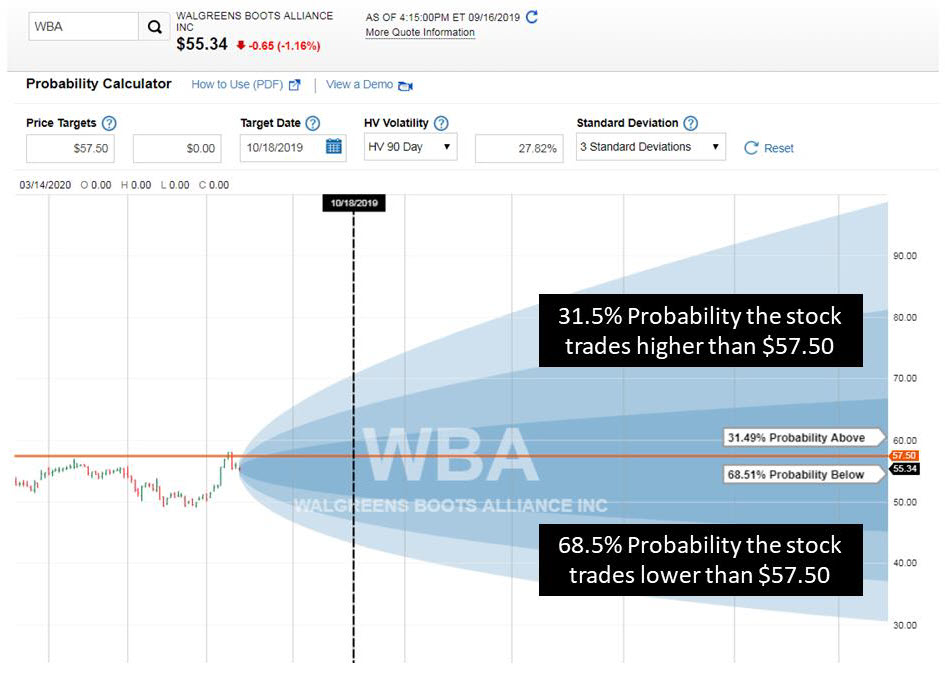

Figure 2 – A detailed look at the probability of the shares trading at $57.50 one month into the future. There’s a 31.5% chance the stock trades higher and a 68.5% the stock trades lower than $57.50 from current levels of $55.30.

Options are sold (covered calls or cash covered puts), and a premium is collected at the selected probability level of choice (70%, 80%, 90%, etc.). This is an iterative process where a premium is collected over and over again at your desired probability level to generate consistent income without predicting which way the stock will move, only betting that the stock won’t move beyond the probabilities you select. If you were to trade this trade hundreds of times, you can expect to win 66% of these trades at expiration. This level of success can be scaled out to the 85% level or 90% level however the premiums received will be lower since the odds will be lower.

Results

Here, comprehensive results of this options-based approach are highlighted where I usually sell options at the ~85% probability level. Sticking to a set of fundamentals, an options approach can provide long-term, high-probability win rates to generate consistent income while circumventing drastic market moves. Over the previous ~12 months through both bull and bear markets, my win rate percentage was 85% (234/275). The options-based portfolio outperformed the S&P 500 over the same period by producing an 8.64% return against 3.15% for the S&P 500 (Figures 4 and 5).

Figure 3 – Comprehensive options-based portfolio approach outperformance as of market close on August 17th, 2019

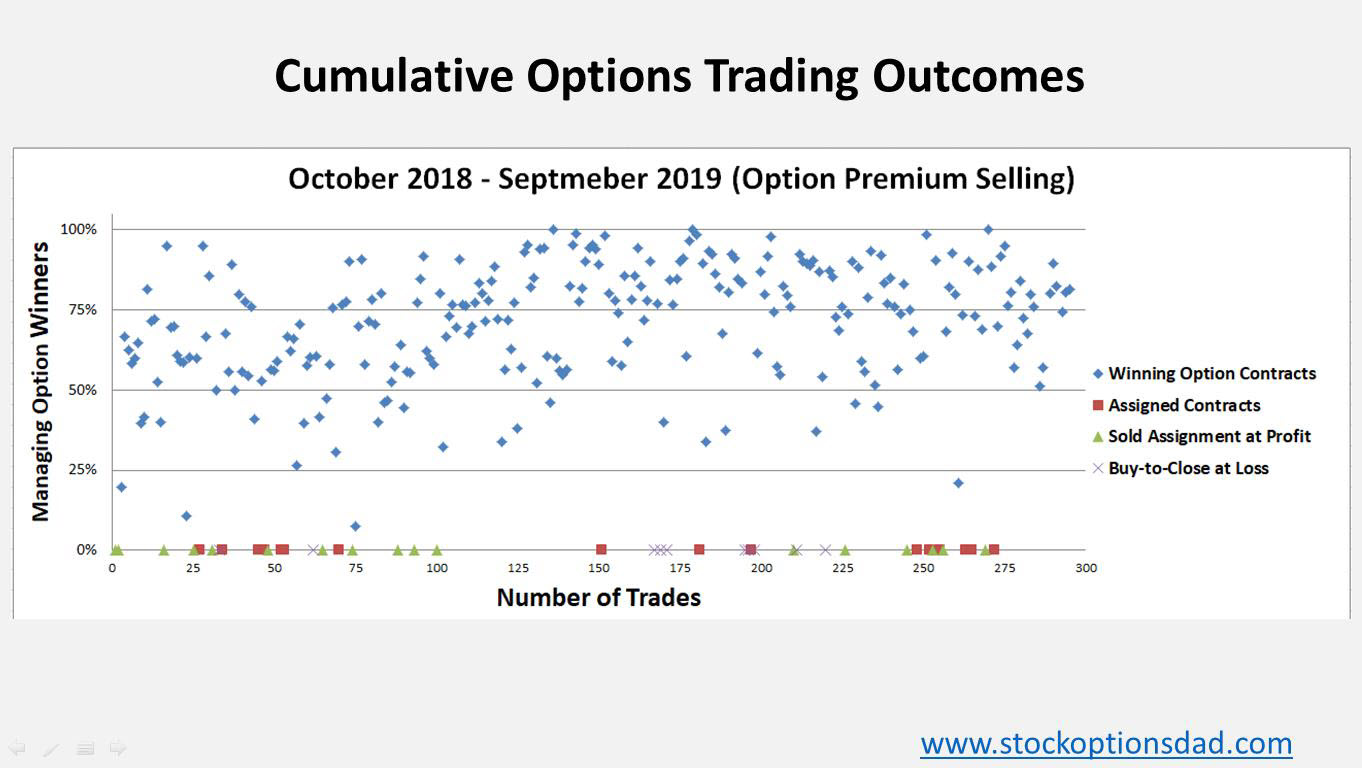

Figure 4 – Comprehensive dot-plot of all trades executed with outcomes (~300 trades) as of market close on August 17th, 2019

Conclusion

Whether you want to win 70%, 80% or even 90% or your trades, you determine your probability of success when it comes to options trading over the long-term. Often times, options traders lose the long-term perspective and discontinue the options-based approach prematurely. Maximizing the number of occurrences is essential in options trading to smooth out any data skew that may result from trades that move outside of your probability target and/or as a result from a small sample size.

Fantasy football and stock options aren’t much different where the probability of the stock trading at a certain level is determined by its past moves (past performance) and future inputs such as earnings (opponent’s defense) relative to the stock itself. Using “Delta” as a proxy for probability is a quick way to assess your probability of success on any given trade. Premium is collected over and over again at your desired probability level to generate consistent income without predicting which way the stock will move, only betting that the stock won’t move beyond the probability you select. If you were to select the 80% probability of success and traded at that level for hundreds of trades, you’d have a win rate of 80%.

An options-based portfolio has allowed me to generate true alpha, something less than 10% of actively managed funds are able to accomplish over the past ~12 months. Options fundamentals provide long-term durable high-probability win rates to generate consistent income while mitigating drastic market moves. I’ve demonstrated an 85% options win rate over the previous ~12 months through both bull and bear markets while outperforming the S&P 500 over the same period by a wide margin producing an 8.64% return against a 3.15% for the S&P 500 with a lower risk profile.

Taken together, options trading is a long game that requires discipline, patience, time, maximizing the number of trade occurrences and continuing to trade through all market conditions.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares in AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY and USO. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.