It’s been a rollercoaster ride of a year for the Gold Miners Index (GDX), with the ETF starting the year up more than 15% and massively outperforming the major market averages, only to suffer a 48% decline over the next five months.

Since then, the GDX has returned to outperforming, and some of the best names, like i-80 Gold (IAUX), are now up more than 50% from their lows.

This extreme volatility is why it can be difficult to trade the Gold Miners Index successfully. The reason is that one must be ultra-patient when establishing new positions to avoid large drawdowns during the down cycle, but being too complacent at the lows can be costly as the index can turn on a dime when it does bottom.

Fortunately, while several of the best names are already off to the races and out of low-risk buy zones, a couple of stocks are still in the proverbial stable and trading at attractive valuations. In this update, we’ll look at two names that offer large safety margins.

Sandstorm Gold (SAND)

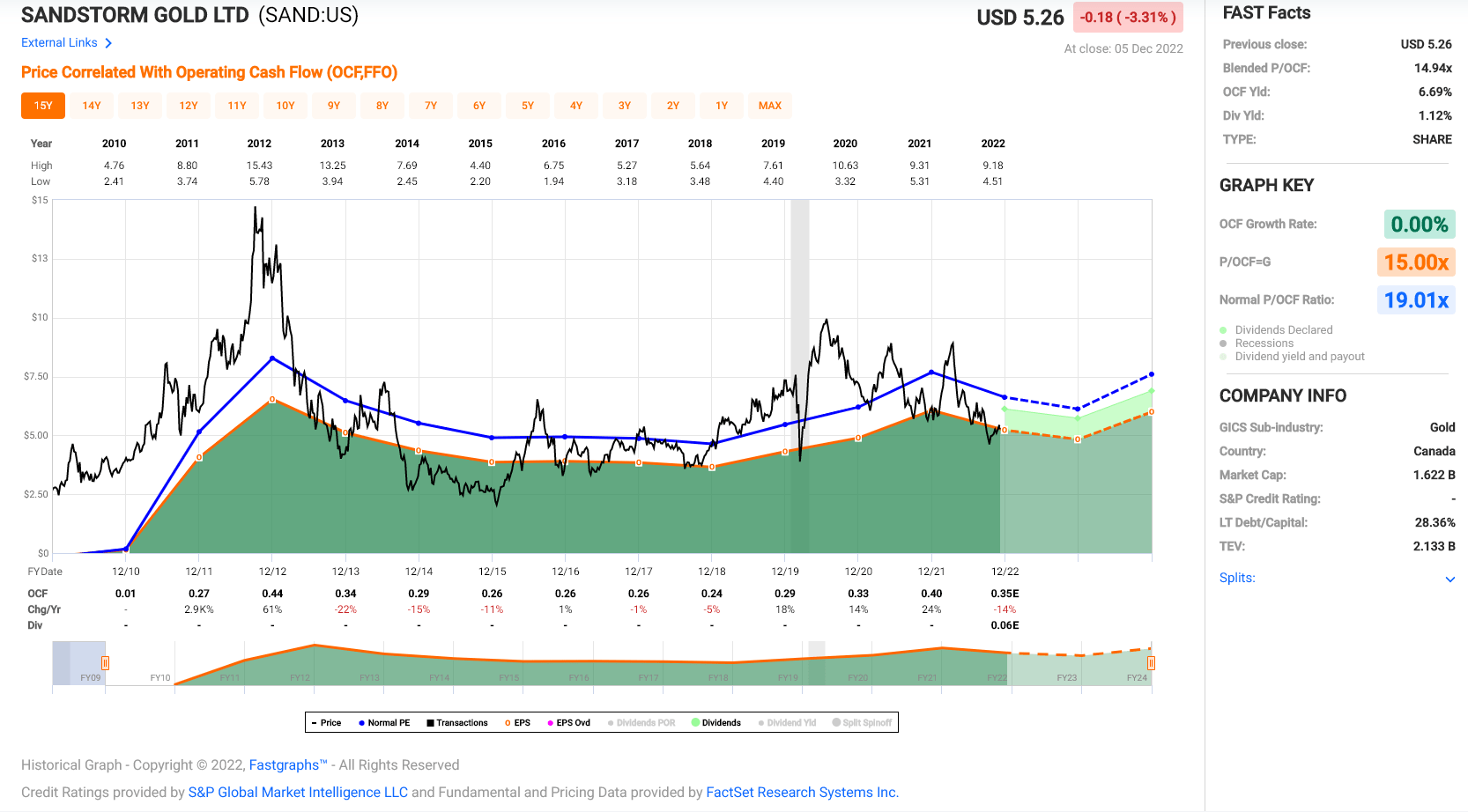

Sandstorm Gold (SAND) is a $ 1.6 billion precious metals royalty/streaming company.

It finances developers and producers in the gold and silver space, giving them capital upfront to build or expand their assets. In exchange, Sandstorm receives either a royalty on the asset over its mine life or a stream on the asset, meaning that Sandstorm has a right to buy a percentage of metal produced at a fixed cost well below the current spot price of gold/silver.

Since royalty/streaming companies typically have royalties/streams on over 20 assets, they are much more diversified than producers with 5-10 mines.

They also have much higher margins, given that they do not have to pay for labor, chemicals, fuel, explosives, and transportation but simply sit back and collect their metal deliveries from these assets.

Finally, the major benefit to owning royalty/streaming companies is that they are not required to spend annually on sustaining capital to maintain an operation, including mine development, drilling, and tailings expansions. In fact, any added resources are very beneficial, given that the royalty/stream is bought and paid for already. Hence, this is a proverbial cherry on top.

Unfortunately, while Sandstorm benefits from this superior model that carries very low risk, the company has had a tough year in 2022. This is because it went out and completed two major acquisitions ($1.1BB value), a smart move, and these deals transformed its portfolio from an average royalty/streamer to one with a phenomenal portfolio.

The issue was that Sandstorm ended up biting off a little more than it could chew with an increase in debt while gold, silver, and copper prices plunged in the fall, impacting its cash flow.

The result was that Sandstorm chose to do a $90MM capital raise to reduce its leverage ratio and pay down a portion of its debt, and this certainly wasn’t received well by the market, with these funds raised at a multi-year low for the stock.

However, while this certainly was painful for investors already in the stock, with SAND hitting new 52-week lows, this negative sentiment surrounding the deal has provided an excellent entry point into the stock for new patient investors looking for names trading at attractive valuations.

In fact, SAND is now the cheapest precious metals royalty/streaming stock in its peer group.

This deep discount to fair value is even though SAND’s portfolio has never looked better (increased diversification), and it has the best growth profile sector-wide, expecting to see annual gold-equivalent ounce [GEO] sales grow from ~80,000 in FY2022 to ~155,000 in FY2025.

If achieved, Sandstorm will generate over $200MM in cash flow in FY2025, making Sandstorm very attractively valued at just 8x FY2025 cash flow for a company with ~80% margins.

Based on what I believe to be a fair multiple of 19.0x cash flow (in line with its historical average) and FY2023 cash flow estimates of $0.41, I see a fair value for SAND of $7.80, translating to a 50% upside from current levels.

However, this assumes no upside in the gold price and doesn’t factor in the significant growth in attributable production in 2024 and 2025.

So, for patient investors, SAND’s cash flow per share should increase to $0.68 in FY2025, placing its fair value at $12.90, translating to a 148% upside to its 2-year target price.

Hence, I see the stock as a steal at current levels and plan to continue to accumulate below $5.20.

SSR Mining (SSRM)

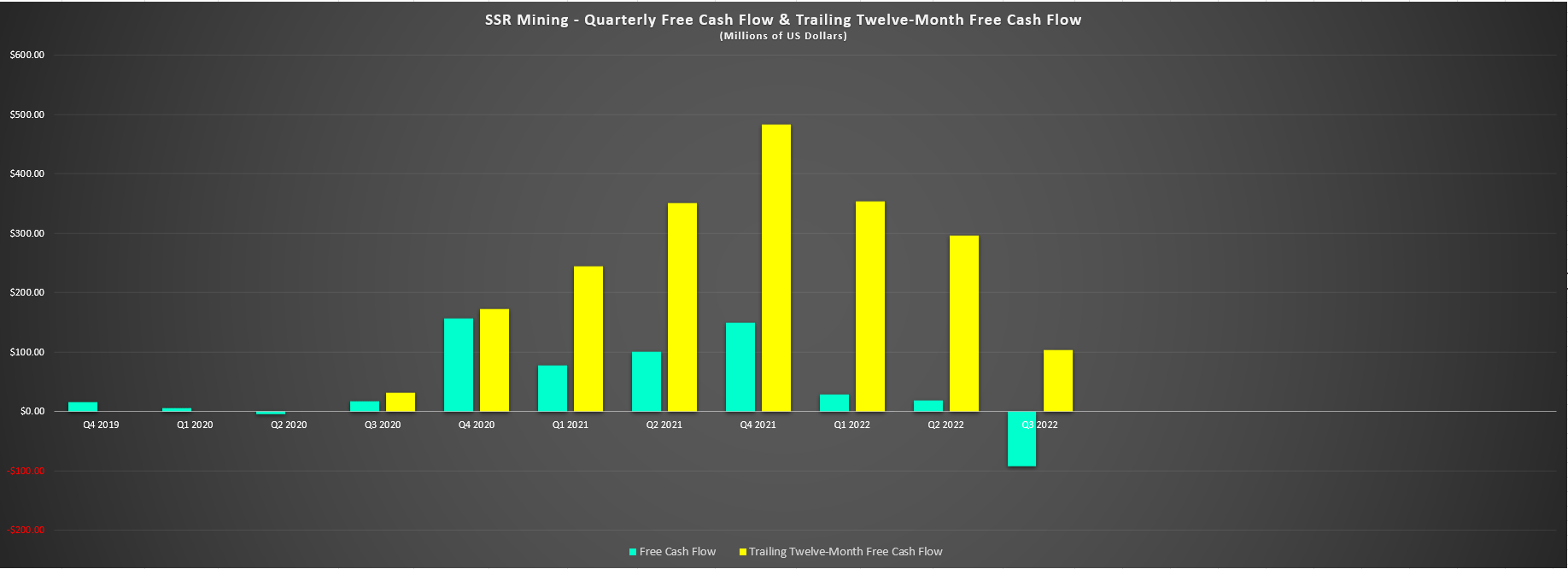

SSR Mining (SSRM) is an intermediate gold producer with four operating mines. These include the Copler Mine in Turkiye, the Marigold Mine in Nevada, the Puna Mine in Argentina, and the Seabee Mine in Canada.

This intermediate producer was one of the best-performing precious metals stocks in 2021, with an aggressive buyback program, the announcement of a dividend, and the subsequent increase in its dividend ($0.28 annualized vs. $0.20).

Meanwhile, the company finished 2021 on a high note, producing ~794,000 GEOs at all-in-sustaining costs of $955/oz, beating its output guidance and its cost guidance for the year.

Unfortunately, while 2021 was an exceptional year that helped the stock outperform most of its peers, 2022 has been nearly the exact opposite from an operational standpoint.

For starters, the company has seen slower leach times than planned which has impacted production at Marigold.

Secondly, the company had a leak of leach solution with diluted cyanide at its Copler Mine in Turkiye, forcing a suspension of operations and a major shortfall in expected output this year. Since Copler is the company’s largest mine with its lowest costs, this severely impacted the company’s Q3 results.

As it stands, SSR Mining has produced less than 500,000 GEOs this year, and all-in-sustaining costs are sitting well above $1,200/oz year-to-date, with margins plunging from $844/oz in Q3 2021 to [-] $105/oz. This was impacted by a lower gold price and much higher operating costs due to inflationary pressures, plus a limited contribution from Copler.

Not surprisingly, the stock has found itself more than 40% off its all-time highs, and it’s been one of the worst-performing gold producers in H2-2022, with free cash flow generation falling off a cliff.

The good news is that the Copler Mine has since restarted, and its Seabee Mine has a strong Q4 ahead. Plus, its Marigold Mine benefits from much higher grades, setting the company up for a much stronger quarter in Q4.

In addition, the company is now benefiting from a recovery in the gold price, and it has much easier comparisons ahead on a year-over-year basis after lapping what’s been a very difficult year.

Finally, the company continues to have exploration success across its properties, setting it up for organic growth later this decade.

So, while it was hard to justify owning the stock above $24.00, the setup is much more attractive with the stock below $15.50.

Based on a conservative cash flow multiple of 9.5 (reflecting its strong organic growth profile and track record of generous capital returns to shareholders), I see a fair value for the stock of $20.40 (FY2023 estimates: $2.15).

This points to a 32% upside from current levels, but investors can expect closer to a 37% total return when incorporating buybacks and dividends.

So, with SSRM set up for a better year and sentiment in the gutter, I would view further weakness below $14.90 as a buying opportunity.

While there are several names to choose from to play the recovery in the gold price, I see SAND and SSRM as two of the more undervalued names, with SAND being a clear example of a massive valuation disconnect.

In summary, I see SAND as a Buy below $5.20 per share and SSRM as a buy below $14.90 per share.

Disclosure: I am long SAND

Taylor Dart

INO.com Contributor

Disclaimer: This article is the opinion of the contributor themselves. Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

what is the weiss rating for these 2 gold stocks? are they on the monthly letters you send out?