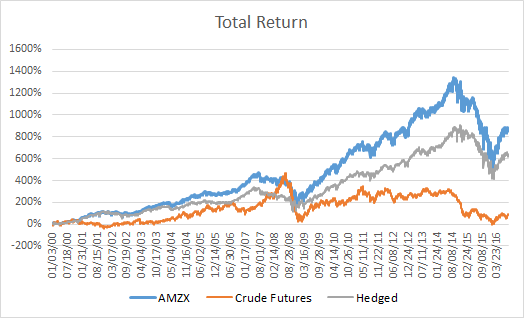

Energy-focused master limited partnerships (MLPs) have provided investors good returns over time, much better than owning crude oil futures. For example, from January 200 through July 2016, the Alerian Total Return Index (PACF:AMZX), a leading gauge of energy MLPs, provided a return of 867%, far exceeded the return from crude futures of about 63%.

However, there is reasonably strong correlation between AMZX and crude futures prices. As a result, AMZX has suffered some large drawdowns. It maximum drop from peak-to-valley (P2V) was 58% over the period mentioned above. I use P2V as my primary risk measurement because it shows how large a loss one may experience in a buy-and-hold strategy.

I tested hedging AMZX by maintaining a short position in crude futures. The risk-minimizing hedge ratio for crude futures was -17% but it only reduced the maximum P2V to 50% (see Hedged return in graph below).

I therefore applied the risk management process I developed to determine when to be invested in AMZX and when to go to cash. I provide the citations for the mathematical formulae and back-tested results for anyone interested in utilizing this process below. Continue reading "Energy-Focused Master Limited Partnerships (MLPs) Require Risk Management"